You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Running a business means managing the constant ebb and flow of cash. Even profitable companies sometimes face gaps between paying expenses and receiving customer payments. Enter working capital loans. These financing options are tools designed to keep your business operations running smoothly during these temporary shortfalls.

According to the 2025 Intuit QuickBooks Small Business Financing Report, operations using only business financing are more likely to report healthy cash flow compared to those relying on personal funds. This suggests that having the right funding strategy is not just about survival, but about setting the stage for stability.

This guide explores what working capital loans are, the different types available, and how to decide if this financing option is the right move for your business.

A working capital loan is a short-term financing solution that helps businesses cover everyday operational expenses. Unlike loans used to purchase equipment or real estate, working capital loans fund the routine costs that keep your doors open.

These loans are not designed to buy long-term assets or investments. Instead, they provide the liquidity needed to handle short-term financial obligations. Business owners can focus on growth and operations rather than worrying about whether there is enough cash in the bank to keep the lights on this week.

Working capital represents the difference between your current assets (cash, accounts receivable, inventory) and current liabilities (accounts payable, short-term debts). A working capital loan helps bridge gaps in this equation by providing funds for:

Businesses can choose from several working capital financing options, each suited to different situations.

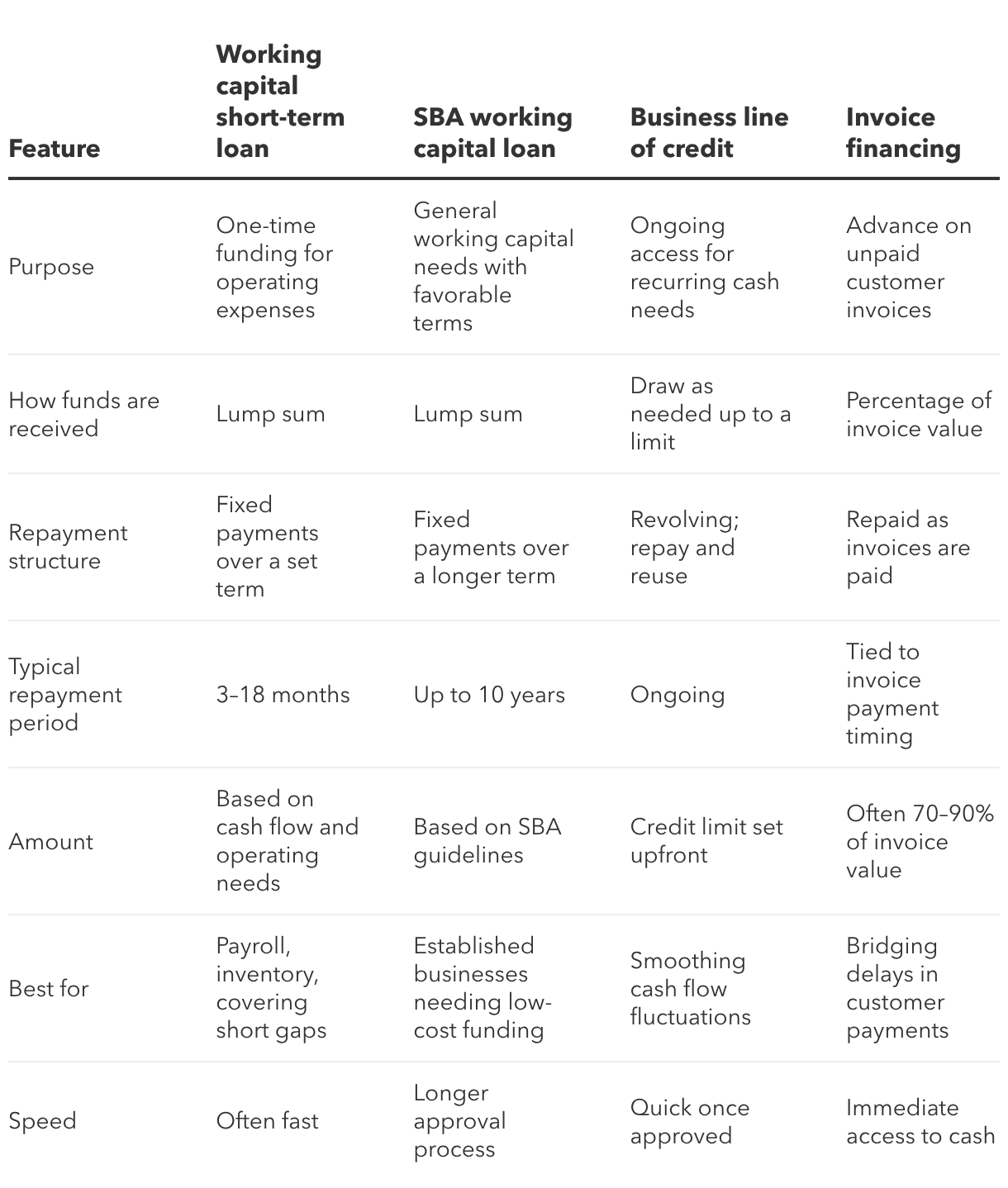

These traditional loans provide a lump sum with fixed repayment terms, typically ranging from three months to two years. They work well when you need a specific amount for a defined purpose. Because the term is short, the payments may be higher than a long-term loan, but you clear the debt from your books faster.

The Small Business Administration offers working capital programs with favorable terms, though they require more documentation and longer approval times. SBA loans are partially guaranteed by the government, which reduces risk for lenders and often results in lower interest rates for borrowers.

A line of credit gives you access to funds up to a predetermined limit. You only pay interest on what you borrow and can draw funds as needed. Once you repay the borrowed amount, that credit becomes available to use again.

Also called accounts receivable financing, invoice financing allows you to borrow against unpaid customer invoices. You receive immediate cash while waiting for customers to pay. Lenders typically advance a percentage of the invoice value (e.g., 85%) and release the remaining amount, minus fees, upon customer payment.

Take a look at the chart below to see how these common working capital financing options compare.

Working capital loans work best in specific scenarios. Below are everyday business situations where this type of funding can be a practical option.

Many businesses experience predictable busy and slow seasons. A working capital loan helps you:

Retailers preparing for holiday shopping, landscaping companies gearing up for spring, or tourism businesses anticipating summer rushes often benefit from seasonal working capital financing.

Even with steady sales, timing mismatches between paying suppliers and receiving customer payments create cash crunches. Working capital loans help when:

Business rarely goes exactly as planned. Working capital financing provides a safety net for:

Sometimes opportunities arise that require immediate action. Working capital loans enable you to:

Growth requires investment before generating returns. Funding through a working capital loan can help support exciting business ventures, such as:

While working capital loans are a viable solution in various business scenarios, they're not always the right answer. Using short-term debt for the wrong purpose can strain your finances. Let’s break down some of the situations that are better handled with a different type of financing or a longer-term plan.

Avoid short-term working capital loans for purchasing real estate, buying expensive heavy equipment, major renovations, or long-term expansion projects. These investments need longer repayment terms that align with their useful life and return timeline.

Longer-term loans or equipment financing usually offer lower rates and extended amortization periods for these needs.

If your business consistently spends more than it earns, a working capital loan only delays inevitable problems. Before borrowing, address underlying issues, like pricing that doesn't cover costs, inefficient operations, declining market demand, or an unsustainable business model.

Taking on debt without a clear repayment plan creates financial stress. Avoid working capital loans if you have no realistic path to increased revenue or if current debt obligations already strain your cash flow.

If a working capital loan fits your needs, the next step is understanding how lenders decide who qualifies.

When reviewing working capital loan applications, most lenders will evaluate the following criteria:

As with any loan, you’ll need some basic documents to support your application. Whether you use accounting software or keep records another way, having everything organized ahead of time can make the process feel smoother.

Before applying, determine how much funding you actually need. Borrowing too much wastes money on unnecessary interest, while borrowing too little can fail to solve your problem.

Working Capital = Current Assets - Current Liabilities

This formula shows how much short-term financial breathing room your business has. It compares what you can quickly access—like cash, receivables, and inventory—to what you owe in the near term, such as vendor bills, payroll, and short-term debt.

A positive number generally means you can cover upcoming obligations. A negative number can signal tight cash flow and the need for additional support.

Once you understand your current position, use these steps to figure out how much funding makes sense for your requirements.

List the exact expenses you need to pay and when you’ll need the money. This keeps your loan amount tied to real, near-term needs.

Many businesses add 10–20% to cover timing gaps or unexpected costs, so the loan doesn’t feel tight from day one.

Review projected revenue to confirm monthly payments fit comfortably within your cash flow.

Factor in interest, fees, and total repayment—not just the loan amount—to understand the full impact on your business.

Say your business needs to cover a few short-term costs:

That puts your working capital need at $50,000.

If you secure a 12-month working capital loan at 12% annual interest, your estimated monthly payment would be about $4,440, with a total repayment of roughly $53,280 over the year. This figure helps you see how the loan fits into both your immediate needs and your ongoing cash flow.

Working capital loans vary significantly in cost and structure. It is vital to read the fine print.

Interest rates and fees directly impact the overall cost of your loan or credit. Knowing what to expect can help you compare your choices, budget effectively, avoid surprises, and make informed financial decisions.

Working capital loans offer various repayment schedules to fit different business cash flow cycles.

Always calculate the total repayment amount, not just the interest rate. A loan with a lower rate but higher fees might cost more overall than one with a higher rate and minimal fees.

Before committing to a loan, consider these alternatives. Getting funding for a business can take many forms.

For smaller, short-term needs, business credit cards can help cover expenses quickly. Certain cards also offer rewards, useful perks, or a limited interest-free time period.

Equity financing means raising capital by selling an ownership stake in your business—often to angel investors, venture capital firms, or other investors—rather than taking on debt. In return for this capital, you give up partial ownership and may share some control over major decisions.

Research industry-specific grants, government programs, and business competitions that provide non-repayable funds. While competitive, this is essentially "free money" that doesn't add to your liabilities.

Sometimes the answer isn't more money, but better management of the money you have. You might negotiate better payment terms with suppliers, offer discounts for early customer payments to accelerate cash inflow, tighten credit policies, or reduce unnecessary expenses.

Not all lenders are the same, and not all loans fit every business. Finding the right lending partner is just as important as finding the perfect loan for your needs.

Traditional banks are well-established financial institutions and a common source for business loans. They offer stability but often come with stringent requirements.

Online lenders operate digitally, providing quick, accessible financing solutions that can be ideal for immediate needs.

Credit unions are member-owned, non-profit financial cooperatives. They often prioritize community and can provide a more personal lending experience.

Alternative lenders are non-bank institutions that offer financing outside of traditional banking channels. They often provide specialized and flexible funding options.

Once approved for working capital funding, use these tips to maximize benefits.

Stick to your planned use of funds. Prioritize expenses that generate revenue or solve immediate problems. Track spending carefully and avoid using loan funds for non-essential expenses or personal purchases.

Set up automatic payments to avoid late fees. Pay more than the minimum when possible to reduce interest costs. Monitor cash flow to ensure you always have payment capacity. If problems arise, communicate with lenders immediately rather than missing a payment.

Use the loan period to strengthen your operations. Address underlying cash flow issues to reduce your reliance on debt in the future. Simultaneously, work on building business credit by making every loan payment on time.

Working capital loans are an excellent tool for managing short-term financial needs, helping you navigate challenges and seize opportunities. By using them strategically, you empower your business to operate smoothly and grow with confidence.

Ready to take the next step? QuickBooks Term Loans and Lines of Credit can keep your business on track. Even better? You can manage your money right where you already manage your finances. See how QuickBooks working capital financing could benefit your business.

QuickBooks Term Loan and QuickBooks Line of Credit loans are issued by WebBank.

Call Sales: 1-800-285-4854