This guide will help you learn what credit means in everyday life, how it works for your business, and why it’s a key part of accounting. We’ll also show you how QuickBooks can help you stay on top of it all, whether you’re tracking your credit score or managing your invoices.

Credit definition

A credit is a key financial term with two meanings, depending on the context:

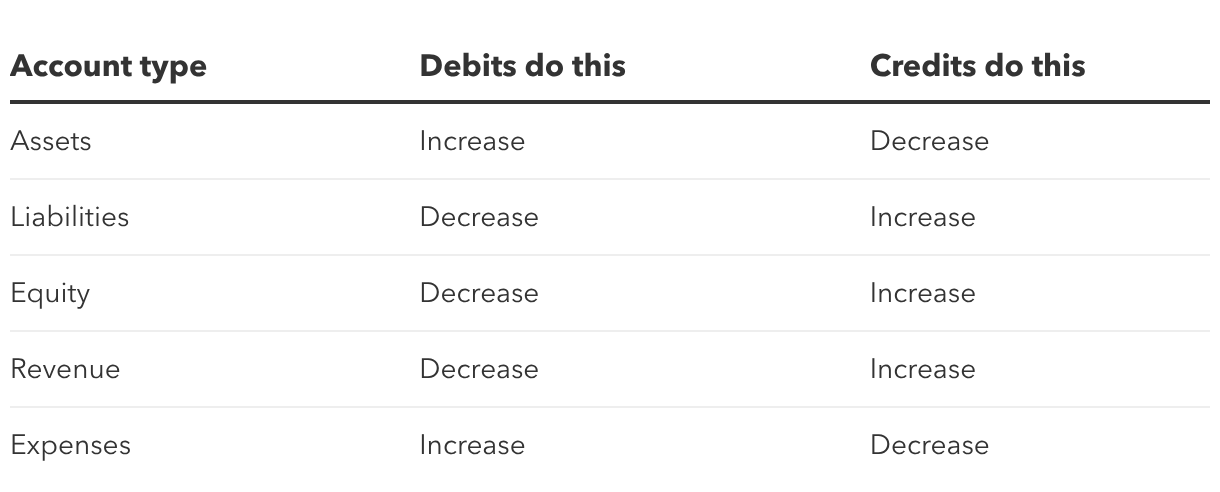

- In accounting: An accounting credit is an entry recorded on the right side of a ledger in the double-entry bookkeeping system.

- In finance: Credit refers to an agreement where a lender provides funds, goods, or services to a borrower, who agrees to repay in the future (typically with interest).

Why credit matters

In the financial context, credit matters because it can shape the opportunities you have in life and business. Good credit can open doors, while bad credit can close them.

When your personal credit is strong, you can:

- Get approved for loans like a mortgage, car loan, or personal loan, usually with better rates that save you money.

- Rent an apartment more easily since many landlords check your credit to see if you’re likely to pay on time.

- Set up utilities like electricity or internet, since utility companies often run credit checks before opening accounts.

- Save money because better credit scores can mean lower insurance premiums and interest costs over time.

- Get a job, as some employers may check your credit for roles where you handle money or sensitive information.

For businesses, good credit is just as important. A solid business credit profile can help you:

- Access financing like small business loans, lines of credit, or equipment leasing, typically with higher limits and lower interest rates.

- Negotiate better terms with suppliers since vendors may offer longer payment terms or larger orders when they trust your business’s creditworthiness.

- Manage cash flow during slow months, so you don’t have to dip into savings or miss payroll.

- Grow faster by leveraging financing to invest in inventory, hire employees, or expand operations.

Business vs. personal credit scores

If you run a business, it’s important to know how business credit scores differ from your personal credit history.

Personal credit scores are tied to you as an individual. They show how well you manage personal debts like credit cards, auto loans, or mortgages. These scores usually range from 300 to 850. The higher your score, the more likely lenders think you’ll pay your bills on time. Companies like Equifax, Experian, and TransUnion calculate these scores based on your payment history, how much you owe, how long you’ve had credit, new credit accounts, and the mix of credit you use

Business credit scores measure how well your business pays its bills and manages credit. These scores are completely separate from your personal scores. Agencies like Dun & Bradstreet (D&B) and Experian Business figure out your business credit score based on your company’s payment history with vendors, how much credit it uses, public records like liens or bankruptcies, and how long your business has been operating

Credit for businesses

Credit can be a powerful tool for businesses of all sizes. When you use it wisely, it helps you cover day-to-day costs, invest in new opportunities, and keep cash flowing when times are slow. Building strong business credit also shows lenders and suppliers you’re reliable, so you can get better rates and terms to help your business grow.

What is business credit?

Business credit is your company’s ability to borrow money or get goods and services now, with the promise to pay later. Unlike personal credit, it’s tied to your business, not you. A solid business credit score makes it easier to get working capital and term loans, lines of credit, or flexible payment terms with suppliers, all of which help your business move forward

Types of business credit

Businesses have a few options when it comes to credit:

- Bank loans: Borrow a set amount for big needs like equipment or renovations.

- Business lines of credit: Flexible funds you can draw from as needed, perfect for handling slow seasons or emergencies.

- Trade credit: Agreements with vendors that let you buy goods or services now and pay for them later, typically within 30, 60, or 90 days.

- Business credit cards: Pay for everyday expenses and earn rewards or cash back.

Building and monitoring your business credit profile

Follow these key steps to help you set up and maintain a good business credit score:

- Establish a separate legal entity: Form a limited liability company (LLC) or corporation so your business can build its own credit.

- Get an EIN and D-U-N-S number: Your employer identification number (EIN) and Dun & Bradstreet’s D-U-N-S number help credit agencies identify your business.

- Open a dedicated business bank account. Separate your personal and business finances to stay organized, simplify taxes, and protect your personal assets.

- Pay bills on time: Consistent, on-time payments build a positive credit history.

You may also want to consider using QuickBooks Online. It helps you build great business credit by tracking accounts payable and making sure you pay vendors on time. Many vendors report payments to business credit bureaus, so paying on time matters. QuickBooks also creates reports like profit and loss statements and balance sheets, which lenders usually ask for when you apply for loans or lines of credit.

When personal credit affects your business

Even if your business has its own credit, your personal credit can still play a role. Lenders and landlords can look at your personal credit if your business is new or doesn’t have a long credit history yet. A strong personal credit score can help you get startup loans, secure leases, or qualify for lines of credit that require a personal guarantee.

Credit for individuals

Credit is a key part of everyday life. It helps you buy items you can’t afford to pay for all at once, like a car or a home. It can also affect situations you might not expect, like renting an apartment or securing car insurance. Good credit makes life easier and can save you money over time. Bad credit can mean higher costs or fewer options. That’s why understanding and managing your personal credit is so important.

What is personal credit?

Personal credit is a lender’s trust that you’ll pay back the money you borrow. It’s based on your history of using and repaying credit, like credit cards, auto loans, or mortgages. It’s a way for banks, landlords, or even utility companies to decide if they can trust you to pay on time. When you apply for a new credit card or loan, lenders check your personal credit to decide if they’ll approve you, how much to lend, and what interest rate to charge.

Why your personal credit score matters

Your personal credit score is a three-digit number (usually between 300 and 850) that shows how likely you are to repay borrowed money. Lenders use scores like FICO and VantageScore to decide if they should give you credit and what interest rate to offer. A higher score makes it easier to get approved and can save you thousands in interest over time.

Your score can affect other areas beyond loans. Landlords can check it when you apply for an apartment. Insurance companies might use it to set your premiums. Some employers may even check credit as part of their hiring process for jobs involving money or sensitive information.

Here’s a look at what different credit score ranges mean: