One of the biggest risks businesses take is providing goods and services without payment. While businesses often do things this way, that doesn’t mean there isn’t another option. Instead, you could choose to require advance payments for your goods and services, or just for certain projects.

Advance payments are a way to reduce your risk and ensure you have the capital you need to do your work. This could be invaluable if you're one of the 46% of small business owners in our Small Business Insights Survey experiencing cash flow problems. However, if you are going to accept advance payments, you’ll need to account for these deposits or full payments correctly.

If you’re interested in trying this billing method, but don’t know where to start, we have you covered. In this guide, we’ll cover what advance billing is, the benefits of this billing method, and how to process advance payments.

Jump to:

- What is an advance payment?

- How do advance payments work?

- Advance billing vs. billing in arrears

- How to account for advance payments

- How to accept advance payments

- Tax implications of advance payments

- Pros and cons of advance payments

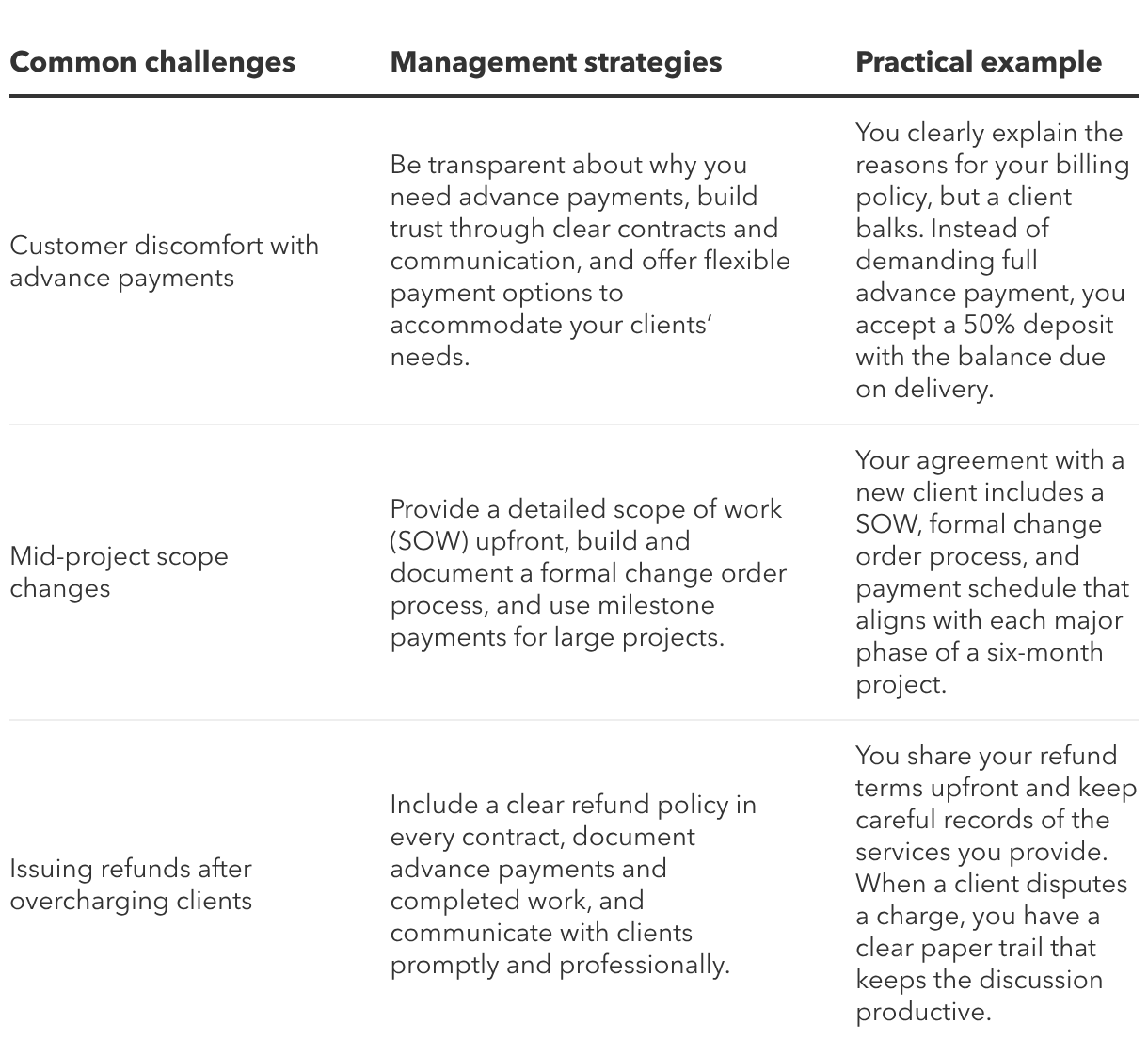

- Common challenges with advance payments

- How to accept advance client payments with QuickBooks Online