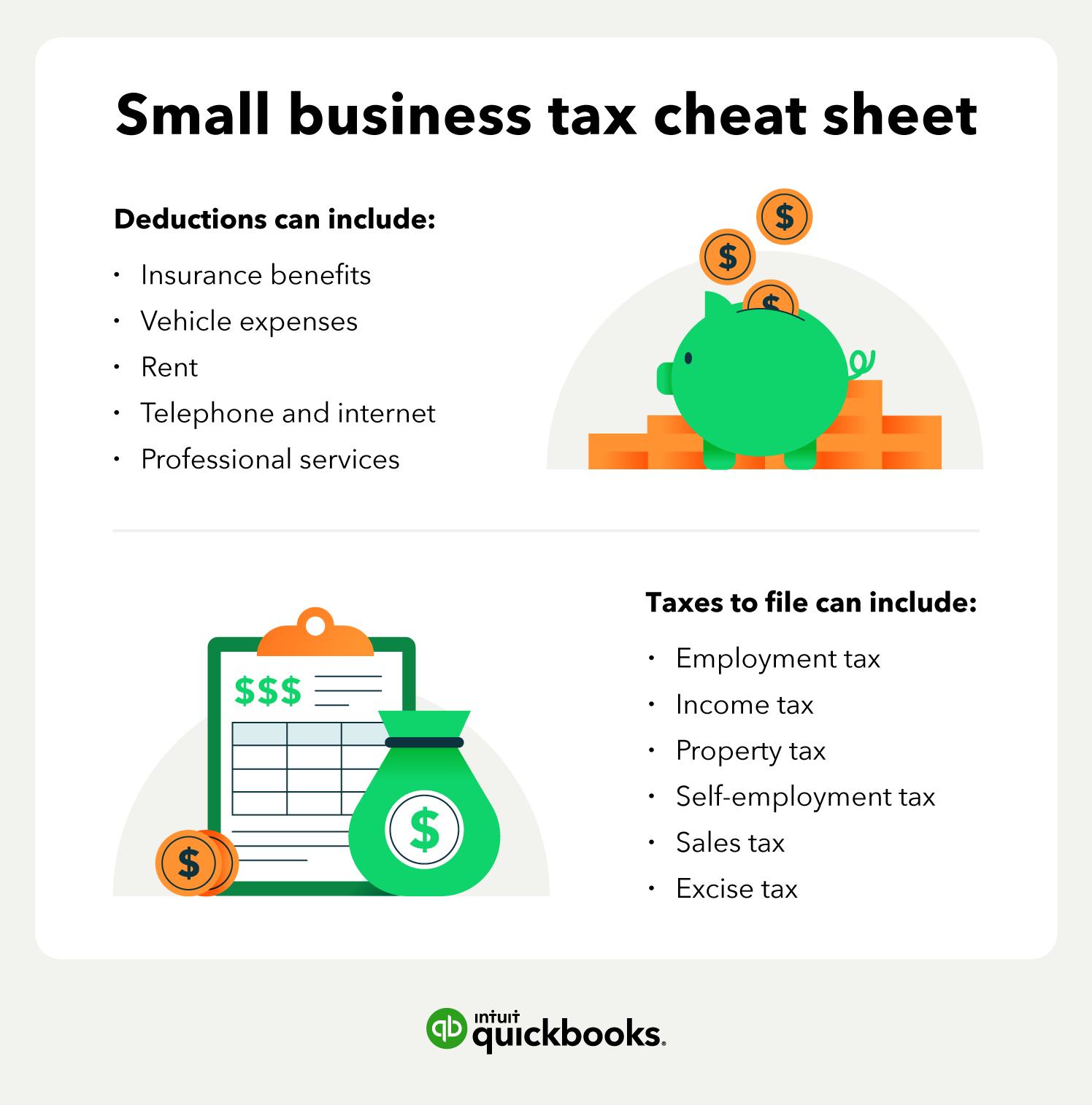

Types of business taxes in Maryland

As an employer in Maryland, you may be responsible for reporting and paying other business taxes in addition to withholding payroll taxes from your employees' paychecks. From federal to state and local levels, understanding the different tax programs and their impact on your business’s finances is important.

Business taxes in Maryland are imposed at the state and federal levels and will vary by corporation type. Businesses may be taxed at the C-corporation or S-corporation rate or avoid higher rates using pass-through filing. Owners of an LLC can elect for pass-through taxation using their personal income filing or pay the C-corporation rate.

Maryland offers tax incentives that are designed to promote development in certain industries and areas of research. Businesses may be taxed using a modified tax schedule that adjusts for business conducted in and out of state.

Federal taxes

No matter where you start your business, federal taxes will be part of your responsibilities. There are dozens of federal tax forms with unique due dates and requirements, so having a good accountant or reliable small business accounting software can help you avoid mistakes that could lead to overpayment or penalties.

As a business owner, you have both personal and business tax filing obligations. Here’s what you need to know:

Personal tax filing

Federal income tax returns:

Every individual is required to file and pay federal personal income tax. This forms the foundation of your overall tax responsibility.

Business tax filing

Business owners have additional filing requirements, depending on the business structure:

- Sole proprietorship: Income and expenses are reported on your personal tax return using Schedule C (Form 1040).

- Partnership: A partnership must file an information return (Form 1065) to report income, deductions, and other relevant details, while each partner reports their share of income on their personal return.

- Corporation: A corporation files a corporate tax return (Form 1120), paying taxes on its profits.

- S Corporation: An S corporation files an informational return (Form 1120S). Its income, losses, and deductions pass through to shareholders, who report them on their personal returns.

- Limited Liability Companies (LLCs): LLCs are not classified separately for federal tax purposes and are taxed based on their ownership structure. Single-member LLCs default to sole proprietorship taxation or may elect corporate taxation, while multi-member LLCs default to partnership taxation or may elect corporate taxation.

Self-employment tax

If you work for yourself and earn more than $400 a year, you pay toward Social Security and Medicare programs through a self-employment tax. The Social Security system provides retirement benefits, disability benefits, survivor benefits, and hospital insurance (Medicare) benefits.

Employment taxes

As an employer, you are responsible for withholding and depositing federal income tax and the employee contribution to Social Security and Medicare taxes. You must also pay the employer portion of Medicare and Social Security and pay federal unemployment tax (FUTA).

State taxes

As a business owner, you must understand your state tax obligations.

Maryland franchise tax

A franchise tax is a fee that businesses pay for the privilege of operating within Maryland. Unlike income taxes, franchise taxes are not based on your business’s profits or net income but rather on the entity’s existence and right to conduct business in the state.

What is the franchise tax rate?

In Maryland, the franchise tax rate varies depending on the type of business:

- For electric companies, 2% of gross receipts from electricity delivered to customers in Maryland

- For gas companies, 2% of gross receipts from gas delivered for final use in the state.

- For telephone companies, 2% of gross receipts from telephone services within Maryland.

How is the franchise tax calculated?

The tax is based on the gross receipts (total revenue) your business earns in its specific industry. This means even if your business isn’t profitable, you could still owe the franchise tax if you provide services like electricity, gas, or telephone lines.

Who may be liable for the franchise tax?

The franchise tax mainly applies to utility companies, such as electricity, gas, or phone services.

Maryland offers the Job Creation Tax Credit, and the Employer-Provided Long-Term Care Insurance Tax Credit. These can be taken against the franchise tax along with the Community Investment Tax Credit by utility companies.

Most other businesses, including sole proprietorships, partnerships, and LLCs, are not liable for franchise taxes. However, if your business operates in a regulated field, it’s important to verify your obligations with the Comptroller of Maryland or a tax professional.

Excise taxes

Excise taxes are special taxes imposed on specific goods or services. In Maryland, these taxes apply to a wide range of products and activities, including:

Alcohol: Maryland imposes excise taxes on beer, wine, and distilled spirits. The current rates are:

- $1.50 per gallon for distilled spirits

- $0.40 per gallon for wine

- $0.09 per gallon for beer, cider, and mead

Motor fuel: The motor fuel tax rates in Maryland are:

- $0.4610 per gallon for gasoline

- $0.4685 per gallon for diesel

- $0.4610 per gallon for gasohol, propane, LNG, CNG, and ethanol

Cigarettes: The tax rate on cigarettes is $5.00 per pack of 20 cigarettes, and $0.25 per cigarette in the package for a pack of more than 20 cigarettes.

Other Tobacco Products (OTP): The tax rate for OTPs — excluding pipe tobacco and cigars — is 60% of the wholesale price of the tobacco product.

Cigars: Non-premium cigars are taxed at 70% of the wholesale price, while premium cigars are taxed at 15% of the wholesale price.

Pipe tobacco: Pipe tobacco is taxed at 30% of the wholesale price.

Electronic Smoking Device (ESD): ESDs and vaping liquid in a container of more than 5 ml are subject to a 20% sales and use tax rate. Vaping liquid in a container of 5 ml or less has a 60% tax rate.

Unemployment tax

As in all states, employers must pay federal unemployment insurance (UI) taxes. Maryland employers are also responsible for paying state unemployment insurance taxes. These taxes are calculated based on each employee's wages, up to a predetermined annual amount called the "taxable wage base" or "taxable wage limit."

State unemployment tax in Maryland begins with a wage base of $8,500 and has certain rates for new employers. The rate is between 0.3% and 7.5% for most businesses and 2.6 % for new employers.

Local taxes

In Maryland, all 23 counties and Baltimore City charge local income taxes, which are collected as part of your state income tax return. The rates vary depending on where you live, ranging from 2.25% to 3.20% of your taxable income. For instance, in Anne Arundel County, the rates for 2025 are tiered, starting at 2.70% and going up to 3.20%, depending on your income level and filing status.

Some jurisdictions levy additional local taxes, for example:

- Baltimore County charges an 8% tax on telephone and wireless service revenue.

- Baltimore City levies a 1.5% transfer tax on real estate transactions.

- Baltimore County has a 9.5% transient occupancy tax on room rates.

Sales and use tax

Sales and use tax is levied on tangible goods purchased in person, on the internet, or via phone and used in Maryland. The sales and use rate is 6% throughout the state and normally is paid each quarter. The Comptroller may adjust the frequency based on your amount due and will contact business owners regarding this.

Maryland does have sales tax and may require licenses for larger businesses as well as small enterprises. People selling at fairs or events often get a temporary license that covers 30 days of business. The rate for vendors is 6%.

The rate is 6% for sales under $1 and is assessed as follows:

- $.01 for sales of up to $.20

- $.02 for sales between $.21 and $.34

- $.03 for sales between $.34 and $.51

- $.04 for sales between $.51 and $.67

- $.05 for sales between $.67 and $.84

- $.06 for sales between $.84 and $1

The rate is exactly 6% for sales involving a taxable amount over $1 plus an additional:

- $.01 for amounts with an extra $.01 to $.17

- $.02 for amounts with an extra $.17 to $.34

- $.03 for amounts with an extra $.34 to $.51

- $.04 for amounts with an extra $.51 to $.67

- $.05 for amounts with an extra $.67 to $.84

- $.06 for amounts with an extra $.84 and less than $1

You can apply for a sales tax permit through the Maryland Department of Revenue and will not have a filing fee.

Sales and use tax is a combined tax in Maryland that is applied to natural gas, electricity, and other tangible goods. It also applies to the right to rent a room in a residential building or hotel.

Remote seller tax considerations

Remote sellers are businesses located outside of Maryland that sell to customers in the state through online platforms, mail, phone, or other remote methods. In 2018, the U.S. Supreme Court's decision in South Dakota v. Wayfair, Inc. allowed states to require remote sellers to collect and remit sales tax if they meet certain economic thresholds, even without a physical presence in the state.

In Maryland, remote sellers are required to report their sales and collect Maryland sales and use taxes if they meet one of these two criteria:

- Their total annual revenue from Maryland-based sales reaches or exceeds $100,000

- They process 200 or more transactions in the state within a year

Remote sellers must register with the Comptroller of Maryland to comply with these regulations and remit taxes on a regular basis.

Property tax

Property taxes are a key source of funding for local governments in Maryland, including all 23 counties, Baltimore City, and over 150 municipalities. These taxes apply to real property, such as land and buildings, and are assessed annually. Property tax bills are typically sent out in July or August for the fiscal year starting on July 1.

Property tax rates in Maryland vary depending on where your property is located. Rates are expressed as a dollar amount per $100 of your property’s assessed value. For example:

- Allegany County: $0.9750 per $100 of assessed value

- Baltimore City: $2.2480 per $100 of assessed value

- Montgomery County: $0.6700 per $100 of assessed value

Maryland also taxes personal property owned by businesses, such as equipment, furniture, and inventory. However, there are exemptions available. For example, farm equipment is fully exempt in all counties.

The Maryland Department of Assessments and Taxation (SDAT) determines the fair market value of properties for tax purposes. If you feel your property’s assessment is too high, you have the right to appeal the decision through SDAT’s appeal process.