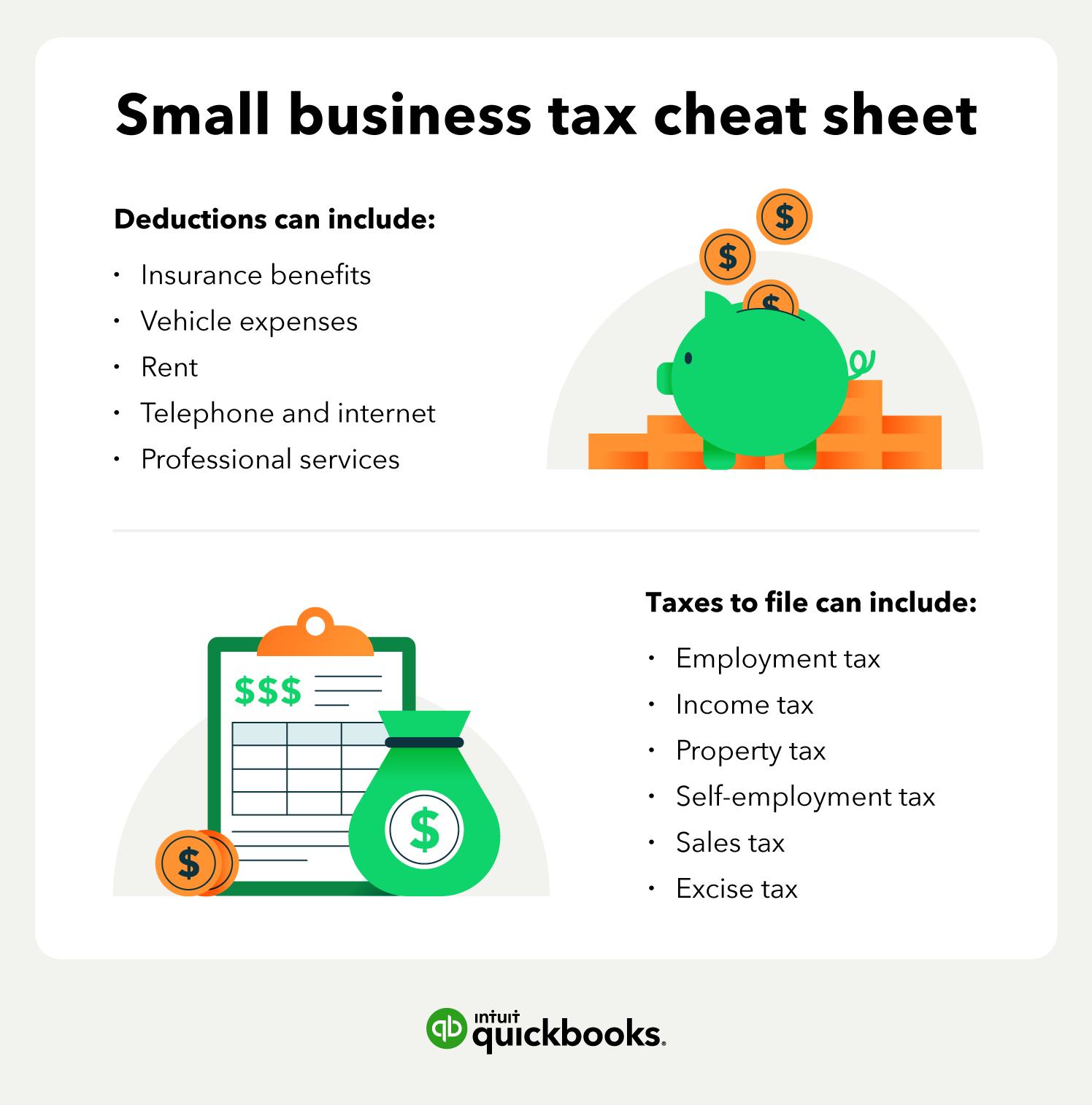

Types of business taxes in New York

As an employer in New York, you may be responsible for reporting and paying other business taxes in addition to withholding payroll taxes from your employees' paychecks. From federal to state and local levels, it’s important to understand the different tax programs and their impact on your finances. To maintain a fair workplace and meet compliance, your business must adhere to the pay equity laws in New York.

In addition, the onboarding process may seem overwhelming, but can actually be made more seamless by following this HR guide to hiring in New York. On the other hand, offboarding is also important, so be sure to adhere to these New York employee offboarding requirements to ensure compliance and make your professional relationships end on a positive note.

Federal taxes

Regardless of which state you open a business in, you'll be responsible for federal taxes. There are dozens of federal tax forms with unique due dates and requirements, so using an accountant or small business accounting software can help you avoid mistakes that could lead to overpayment or penalties.

As a business owner, you have both personal and business tax filing obligations. Here’s what you need to know:

Personal tax filing

Federal income tax returns:

Every individual is required to file and pay federal personal income tax. This forms the foundation of your overall tax responsibility.

Business tax filing

Business owners have additional filing requirements, depending on the business structure:

- Sole proprietorship: Income and expenses are reported on your personal tax return using Schedule C (Form 1040).

- Partnership: A partnership must file an information return (Form 1065) to report income, deductions, and other relevant details, while each partner reports their share of income on their personal return.

- Corporation: A corporation files a corporate tax return (Form 1120), paying taxes on its profits.

- S Corporation: An S corporation files an informational return (Form 1120S). Its income, losses, and deductions pass through to shareholders, who report them on their personal returns.

- Limited Liability Companies (LLCs): LLCs are not classified separately for federal tax purposes and are taxed based on their ownership structure. Single-member LLCs default to sole proprietorship taxation or may elect corporate taxation, while multi-member LLCs default to partnership taxation or may elect corporate taxation.

Self-employment tax

If you work for yourself and earn more than $400 a year, you pay toward Social Security and Medicare programs through a self-employment tax. The Social Security system provides retirement benefits, disability benefits, survivor benefits, and hospital insurance (Medicare) benefits. As of 2025, the federal self-employment tax rate is 15.3%. 2.9% of this goes to Medicare, and 12.4% goes to Social Security. The Social Security portion applies to the first $176,100 of net earnings for 2025.

Employment taxes

As an employer, you are responsible for withholding and depositing federal income tax and the employee contribution to Social Security and Medicare taxes. You must also pay the employer portion of Medicare and Social Security and pay federal unemployment tax (FUTA).

State taxes

As a business owner, you must understand your state tax obligations.

New York franchise tax

Franchise taxes are required simply for doing business in New York for corporations registered in the state. In most instances, franchise taxes are required on corporations formed in New York but are not required for sole proprietorships or traditional LLCs.

In New York, the terms "corporate income tax" and "corporate franchise tax" are often used interchangeably. The corporate franchise tax encompasses the tax on business income, capital, and the fixed dollar minimum, serving as the primary tax on corporations operating within the state.

What is the franchise tax rate?

New York franchise tax rates depend on corporation type and income. General businesses pay 6.5% on incomes up to $5M and 7.25% above that, while manufacturers pay 0% and emerging tech companies pay 4.875%. A 0.1875% capital base tax (capped at $5M) and a minimum tax of $25-$200,000 (based on receipts) may also apply, with the highest amount due.

How is the franchise tax calculated?

The franchise tax rate in New York varies since it’s more complex than in other states. For tax years beginning on or after January 1, 2024, the calculations are as follows:

- Business income base tax:

- 6.5% for businesses with income of $5 million or less

- 7.25% for businesses with income over $5 million

- Capital base tax: 0.1875% (extended through tax year 2026)

- Fixed dollar minimum tax: Ranges from $25 to $200,000 based on New York State receipts

The tax due is the highest of these three calculations.

Who may be liable for the franchise tax?

In New York State, a company is subject to franchise tax if it has "nexus" with the state, which includes:

- Physical nexus: Domestic corporations incorporated in New York or foreign corporations doing business, employing capital, owning property, or maintaining an office in the state

- Economic nexus: Companies earning $1,283,000 or more in New York receipts

- Financial institutions: Credit card issuers with 1,000+ New York customers or merchant contracts

- Combined reporting: Members of a combined group with at least $12,000 in New York receipts if the group's total New York receipts exceed $1 million

Companies meeting any of these criteria should carefully evaluate their New York State franchise tax obligations. New York allows business owners to apply for franchise tax credits to encourage job growth, economic development, and investments in the state.

For more information on specific tax credits and eligibility requirements, visit the New York State Department of Taxation and Finance or Empire State Development websites. These official sources provide detailed explanations of available credits, application processes, and recent updates to tax incentive programs.

Excise taxes

Excise taxes are special taxes imposed on specific goods or services. In New York, these taxes apply to a wide range of products and activities, including:

Alcoholic beverages: Different types of alcoholic beverages are taxed at varying rates:

- Liquor and wine containing more than 24% alcohol by volume (ABV): $1.70 per liter

- Liquor and wine containing more than 2%, but not more than 24% ABV: $0.67 per liter

- Wine containing 24% ABV or less: $0.30 per gallon

- Beer: $0.14 per gallon

- Cider: $0.0379 per gallon

Tobacco: Cigarettes and other tobacco products are subject to excise taxes. For 2024, the state excise tax on cigarettes in New York is $5.35 per pack.

Motor fuel: New York imposes a motor fuel tax. For liquefied petroleum gas, the excise tax through 2024 is 17.3 cents per gallon.

Unemployment tax

In New York, employers are responsible for funding state unemployment insurance (UI) taxes. These taxes are applied to each employee's wages up to a specified annual limit, known as the "taxable wage base" or "taxable wage limit."

For 2025, the taxable wage base for New York State UI tax is $12,800. Employers' UI tax rates vary based on their experience rating, which in 2024 ranged from 2.1% to 9.9%. This experience rating reflects an employer's history with unemployment claims and determines the specific rate within the given range.

It's important to note that these rates and the taxable wage base are subject to change, and employers should consult the New York State Department of Labor for the most current information. And, as stated above, employers must also pay federal unemployment insurance taxes, which are separate from state UI taxes.

Metropolitan Commuter Transportation Mobility Tax (MCTMT)

You’re subject to the tax if you are required to withhold New York state income tax from wages and your payroll expenses for covered employees in the Metropolitan Commuter Transportation District (MCTD) exceed $312,500 in any calendar quarter. For more information, visit the MCTD website.

These taxes are on top of your regular state and federal taxes. New York City's tax system can be pretty complex, so it's often a good idea to get help from a tax professional to make sure you're doing everything right and taking advantage of any potential tax breaks.

New York Pass-Through Entity Tax (PTET)

The New York Pass-Through Entity Tax (PTET) is an optional tax that partnerships and S corporations can choose to pay on their New York income. It's designed to potentially reduce your overall tax burden, especially if you have significant income subject to New York State taxes. The tax rates range from 6.85% to 10.9% based on income brackets.

One of the main benefits of the PTET is that it can reduce your federal taxable income and may also provide a credit on your state income tax return. However, the PTET is a complex tax, so it's important to carefully evaluate your specific situation and consult with a tax professional to determine if it's the right choice for your business.

Local taxes

In addition to federal and state taxes, many cities, counties, and other jurisdictions in New York levy other kinds of local taxes to fund essential services and infrastructure such as schools, roads, police, and fire protection.

For example, New York City has the Business Corporation Tax (BCT). This tax applies to C corporations and certain S corporations, with taxes calculated based on a combination of income, capital, and a fixed dollar minimum, depending on the size and type of business.

Unincorporated businesses such as partnerships, sole proprietorships, and certain LLCs may also be subject to New York City’s Unincorporated Business Tax (UBT). The UBT applies to sole proprietorships, partnerships, and LLCs operating within the city that haven't elected to be treated as corporations for tax purposes. It's calculated at a rate of 4% of your taxable income. If your estimated tax for the year is likely to exceed $3,400, you'll need to file an annual UBT return and make quarterly estimated tax payments.

Sales and use taxes

New York has a sales tax, which is typically levied on just about all tangible products and many services. In New York, the base sales tax rate is 4%. However, it's important to remember that many counties and municipalities in New York also enforce their own additional local sales tax rates. Some local tax rates can reach a combined 8.875% in total, depending on where you are located in New York and where you intend to conduct business. Tax rates and jurisdictions can be reviewed and compared easily online.

Remote seller tax considerations

Remote sellers must register, collect, and remit New York sales tax if they meet economic nexus thresholds:

- Over $500,000 in gross receipts from tangible personal property delivered into New York in the prior four sales tax quarters

- More than 100 sales of tangible personal property delivered into the state

Sellers meeting these criteria must register as New York vendors, collect sales tax on all taxable sales, and file periodic sales tax returns. These rules apply to all tangible personal property sales, whether taxable or exempt.

Marketplace providers facilitating third-party sales must also register and collect tax if they meet the same thresholds for transactions into New York.

Property taxes

New York State imposes property taxes at the local level, with each jurisdiction using these taxes to fund local services. If you own property in New York, you will receive a tax bill based on the assessed value of your property and the local tax rate, which can vary significantly across taxing jurisdictions.