You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

What will the economy look like this year? No one can say for sure. Things could go well, or the country could face a recession. Towards the end of 2025, job growth had slowed, and unemployment had risen to 4.4%. While this doesn’t mean we’re headed for a downturn, it's still a valid reason to look into recession planning for your business.

In this article, you’ll find detailed steps on how to recession-proof your business as well as insights into factors that might make you vulnerable to a recession.

If a recession hits, there are both upsides and downsides to running a small business. On one hand, your small size may make it easier to pivot your business model quickly. But you might also have less access to credit and capital.

As a small business owner, this lack of resources means you may want to focus on cash flow management to recession-proof your business. You’ll also need to consider your local economy. If you’re in an area with a relatively stable economy, you likely won’t be hit as hard as a larger enterprise with dozens of locations across the country or the globe.

Industry can also be a factor, so consider how recession-proof your field of work is. A pharmacy, for instance, may fare better than a convenience store during a recession, as people will still need their prescription medications.

To determine how prepared you are for a sudden economic downturn, you need to take a hard look at your accounting, sales, and other stats. Here are a few red flags that indicate you might be vulnerable:

It’s important to look at all your business numbers, not just your bank balance. A low bank balance doesn’t necessarily mean your business is in danger. Instead, use accrual-based accounting to determine your true risk. And know that when we’re not currently in a recession, you have time to take the steps needed to prepare and protect your business.

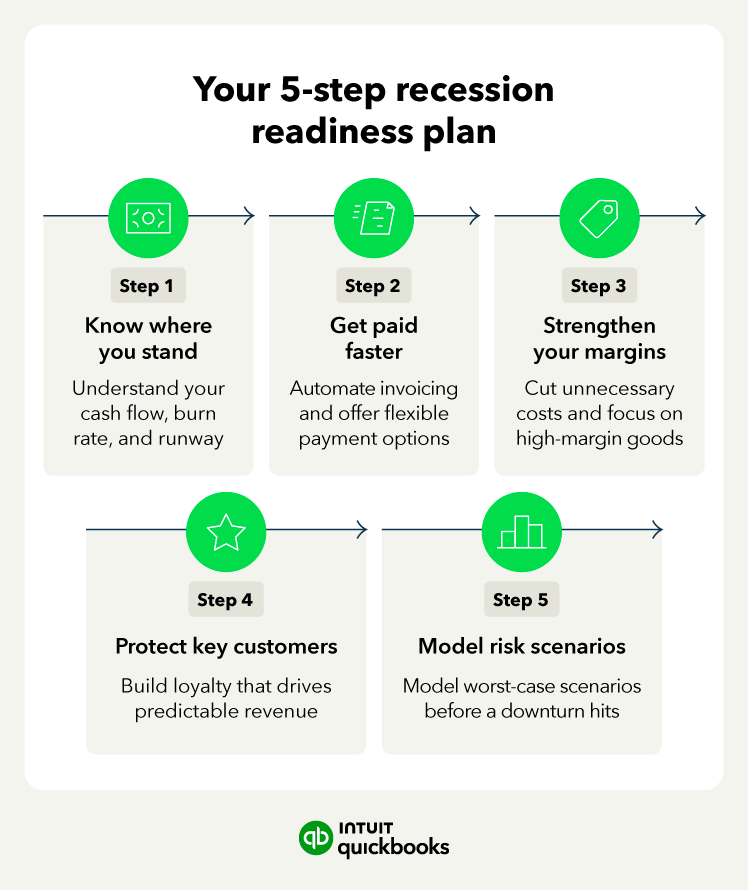

Before you can begin protecting your business from the potential for a recession, you first need a real-time view of your finances.

The first step in understanding your current finances is to generate a profit and loss report. This involves gathering data on your revenue, sales, and expenses, which you should be able to pull quickly from your accounting software.

You can then use these numbers to calculate the cost of goods sold (COGS), operating profit (Earnings Before Interest, Taxes, Depreciation, and Amortization, or EBITDA), and your net income. Now do the same for the prior year so you can compare the last 12 months to the previous year in a year-over-year (YOY) analysis. You’ll want to look for dips or downward trends that aren’t part of normal seasonal slowdowns.

In addition to looking for dips, you may also want to identify the percentage of your revenue currently consumed by COGs and EBITDA, as this will help you with the next step.

Now that you have your baseline number, you can use it to calculate how many months you can survive without revenue during a recession. First, total all your bank balances, average the last three months of expenses, and then divide the first number by the second number.

For instance, $10,000 in cash divided by $5,000 in monthly expenses means you would last only two months if revenue ceased. Use only cash in hand for your calculations, not accounts receivable. If a recession hits, funds tied up in AR are not guaranteed cash.

Having 3-6 months of recession runway is generally considered safe or ideal; however, this can vary by industry. For instance, if you are in a recession-resistant field like healthcare or education, then you might not need as much runway. However, other types of businesses, such as startups or manufacturers, may need additional runway.

The cash runway above assumes the worst-case scenario: A recession that halts your sales. For an accurate picture of your current spending versus cash reserves, you may want to monitor your burn rate. This indicates how many months you can continue operating without depleting your cash reserves.

Accounting software, like QuickBooks, can help you track your monthly outflows to help you determine your burn rate, which is your current cash balance divided by the difference between your revenue and expenses.

For instance, let’s say you're trying to expand your business, and your expenses are $6,000, but your revenue is only $5,000. This gives you a burn rate of $1,000. If you have $10,000 in the bank and your revenue remains steady, then your runway is 10 months.

If a recession hits, you’ll want to decrease your expenses quickly, as a drop in revenue will balloon your burn rate. Appropriately labeling your expenses can help you quickly identify what to cut (e.g., variable costs are usually the first to go).

Now that you have a good idea of what your current finances look like, it's time to recession-proof your business by taking steps to improve your cash flow and savings. From automation to requesting longer net terms, here are some key ways to build your bank balances quickly.

Accounts receivable is the process of collecting money for the goods and services you sold. Without it, you don’t get paid. But as a small business owner, the AR process can be complicated and time-consuming. By automating accounts receivable, you can get paid faster with less hassle.

One way this works is through invoice reminders. Using automation, you can set up reminders so that payment requests are sent in sequence:

These sequence reminders can help prevent late payers from slipping through the cracks.

Another way to ensure you get paid and build your bank balance is to offer your customers flexible payment options. The more payment methods you offer, like ACH, credit cards, and digital wallets, the better. Even though some of these options carry higher processing fees, they're still better than receiving late payments or no payments at all.

Making it easier for customers to access your payment portal can also help. For PDF invoices, you can embed a direct link to your payment portal. Compared with paper checks, adding a Pay Now button can get you paid much faster.

Once again, automation can help you manage your payments more efficiently. For example, QuickBooks Payments automatically reconciles your payments and invoices, saving you the time of manually matching them up.

The other half of the cash flow equation is to reduce expenses. One way of doing this is to negotiate extended payment terms (e.g., moving from Net-15 to Net-30). Having a longer period to pay your bills gives you additional time to collect payment, allows you to prioritize debt repayment, and can even earn you a little extra interest on your balance.

Vendors that extend your payment terms may also offer you early payment discounts. While this can save you money, you’ll want to look at the interest rate on your debt. If the discount is less than the interest on your debt, you’ll want to keep the cash.

To help manage your payments, the Accounts Payable Aging Report in QuickBooks shows who you owe and the latest date you can pay a vendor without incurring a penalty.

To negotiate better net terms, start discussions well ahead of contract renewals. Pull data and history to support your request, and ask for longer terms than you need to reach a favorable compromise.

Another way to protect your business during downturns is to improve your margins through efficiency, expense management, and identifying your highest-margin products. As a business owner, the goal is to ensure every dollar spent produces a return.

Start your margin research by conducting an internal audit. Review every overhead cost, including commonly overlooked expenses such as recurring subscriptions and office cleaning supplies. As you look through your costs, highlight expenses that don’t directly contribute to your revenue or essential operations. These are the costs you can cut.

For QuickBooks users, the Expenses by Category report can help you quickly spot leakage in areas like unmanaged travel, redundant software seats, or office supplies.

Which of your products are performing well? Using the Sales by Product/Service report, you can quickly identify which of your best sellers have the highest profit margins. The report will also help highlight the products with low margins and poor sales. These products and services may be worth sunsetting.

It’s important to consider both sales and profit margins when evaluating your products/services. After all, a low-margin item with high sales is still better than a high-margin item with no sales.

Another way to reduce costs and run lean is to shift from fixed to variable expenses. While some fixed costs can be converted, others, like labor, technology, and logistics, can be moved from fixed to variable.

For instance, if your employees can work from home, eliminating the large permanent office in favor of remote work arrangements and co-working spaces could result in significant savings.

When it comes to labor costs, the Project Tracking feature in QuickBooks can show you exactly how much external labor is costing you per job compared to internal fixed salaries. This can help you decide whether switching from employees to project-based contractors is a good move.

During a recession, loyal customers will help keep you afloat. Keeping a customer is much cheaper than finding a new one, so it's best to identify strategies now that can help you lock in your best customers.

To begin, you need to pinpoint your VIP clients. These are the 20% of your customers who provide 80% of your revenue. Using your accounting data, look for customers with frequent purchases, high average order values (AOV), and high total orders over time. You can use this info to calculate the customer’s lifetime value (CLV) and find the best customers.

Once you’ve identified your VIP clients, review their purchase history, trends, feedback, and more. Then craft a retention plan tailored to them.

One key way to improve customer retention is to reward brand loyalty. You want your customers to keep coming back to you, not looking at the competition.

Some incentives you can offer include:

For example, if you’re selling a subscription service, you can offer a discount for a 12-month commitment versus a month-to-month plan. The goal with retention is to lock in predictable revenue.

Another option for attracting and keeping your customers is to diversify your income streams. Offering all the products and services a customer needs will help ensure they stay with you and build a steady, predictable revenue stream. However, you don’t just want to add products/services at random.

When diversifying, try looking for “sticky” revenue models. These are products or services that make it difficult or costly for your customers to switch. For instance, subscription services, maintenance plans, interconnected products, or proprietary items. The dependable income these new products/services bring in will help you ride out the sales dip of a recession.

Another way to implement “sticky” revenue is to pair a low-cost item with proprietary consumables. For example, an espresso machine brand offers a low cost for the actual machine and then locks customers in with its proprietary coffee capsules.

Being proactive is your best defense against recession-inspired business woes. While simple financial forecasting can help you prepare for a recession, going on the offensive during a downturn can afford you some unique opportunities.

To prepare for the worst, you have to know what the worst-case scenario looks like. What exactly this looks like depends on your business model, size, and industry. For example, if you only have a handful of clients, model what things look like if you were to lose your biggest client. Other worst-case scenarios to consider include recession, disaster, supply chain failures, and data breaches.

Try to anticipate how different scenarios might affect your business. Will you lose revenue, experience a credit crunch, or have delayed customer payments? How do these what-if scenarios affect your cash flow? One way you can calculate this is to use the QuickBooks Cash Flow Planner. By playing with your future income/expense numbers, you could simulate a scenario like a 25% revenue drop.

Once you know what the worst-case scenario looks like and how it will affect your business, you can then craft emergency action plans that include actions like hiring freezes, securing the funding you need early, and reducing nonessential spending. This proactive plan can help you avoid panicking and making poor decisions when the worst happens.

While a recession is generally bad for business, it also presents opportunities. If your cash flow is healthy, then an economic downturn might be the best time to hire top talent, secure cheap advertising, and purchase discounted property or equipment.

While competitors pull back and lay off staff, your investment in your business during the recession can help secure your long-term success.

A business slowdown often leaves you with more time on your hands. Instead of spending this time worrying, you can use it to modernize your processes and streamline your workflows. Automating your bookkeeping tasks, purchasing inventory management software, and digitizing your paper-based documents can all improve your efficiency.

When the economy rebounds, the changes you made will have set you up to take advantage of the boom in business.

While it's important to recession-proof your small business, you should also prepare for a positive future. Perhaps plans for growth and expansion, or for new products and partnerships, are on the horizon.

Real-time cash flow viewing and management are essential for planning for now, the worst, and the future. With QuickBooks Money, you’ll get all the tools you need to stay on top of cash inflows and outflows.

Call Sales: 1-800-285-4854