You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

The IRS draws a simple line between a hobby and a business. A business is an activity you carry out to make a profit, while a hobby is something you do primarily for personal enjoyment, even if it earns money. Businesses and hobbies are taxed very differently.

In 2026, this distinction matters more than ever. The One Big Beautiful Bill Act permanently eliminated deductions on hobby expenses, so hobbyists can only subtract the cost of goods sold. Everything else, from home office costs to software subscriptions, is taxed in full.

According to a QuickBooks survey, 42% of SMB owners say they had limited or no financial literacy before starting out. If you're running payroll in a small or self-employed business, understanding the IRS hobby vs. business distinction can save you thousands at tax time.

The difference between hobby income and business income is how the IRS treats what you earn and what you can write off. Both hobby income and business income are taxable, but the IRS only lets you deduct expenses if you can show a profit motive and run your activity in a businesslike manner.

Here’s a breakdown of how taxes, deductions, and reporting work for hobbies vs. businesses:

Before 2018, hobbyists could deduct expenses up to the amount of their hobby income. The Tax Cuts and Jobs Act (2017) suspended that, and the OBBBA has now made the suspension permanent. Hobby expense deductions are not coming back without new legislation.

The trade-off sounds like a win for hobbyists because they skip paying self-employed tax. But they can't deduct expenses or offset losses against other income, except for the cost of goods sold (COGS). That means no deductions for marketing, home office costs, software subscriptions, mileage, or any other operating expenses.

If you're earning money from a side activity and haven't decided whether to register as a business, this is the math that should drive your decision.

A business owner who earns $30,000 and spends $25,000 pays tax on $5,000 of net profit. A hobbyist in the same position may reduce income by cost of goods sold, but cannot deduct other operating expenses. If their materials cost $10,000, they still owe income tax on $20,000, not the $5,000 a business owner would pay.

If you sell through a platform like Etsy, you may receive a 1099-K. Under the OBBBA, platforms only have to file one when your gross payments top $20,000 across more than 200 transactions. But a reporting threshold is not a tax threshold.

You owe tax on every dollar you earn, regardless of whether a platform sends you a form. And with hobby expense deductions permanently gone, a side hustler who earns $15,000 and spends $10,000 on supplies still owes income tax on the full $15,000, minus only the cost of goods sold.

Whether or not you receive a 1099-K, you must report all income from a hobby or business on your tax return.

The IES uses nine factors to determine whether what you do is a hobby or a business. IRS auditors don’t base their determination on a single factor. Instead, they weigh all nine against your individual circumstances.

To choose business deductions, you need to show the IRS that your activity is driven by profit.

Below, learn the nine factors they use in their decision, but first, here are five ways QuickBooks Solopreneur helps you build your case:

Running your activity in a businesslike manner means keeping the same records and systems that a profitable business would.

QuickBooks Solopreneur lets you categorize transactions as business or personal, creating the paper trail the IRS reviews as evidence you're in it to make money.

Example: One photographer keeps all her bookings on a calendar app, invoices via QuickBooks, and keeps receipts for equipment purchases. Another sells prints to his friends and deposits the cash in his personal account. To the IRS, the first is likely a business and the second is likely a hobby.

The IRS needs to see that you’re putting real hours into your activity to make it profitable. This doesn't mean you have to work on it full-time, but you do need to show that the time you invest goes beyond casual enjoyment.

Keep a time log of your productive hours. Spending 20 hours a week on sourcing, marketing, and fulfillment proves it's more than a weekend pastime.

Example: An aromatic candle maker spends 15 hours most weeks sourcing suppliers, experimenting with new scents, and maintaining her online store. Another who makes candles on rainy weekends and makes a few sales at local yard sales would find it hard to prove she’s running a part-time business.

You can take on staff for your part-time business. Hiring qualified people to help you is a sign that you want to make money, even if your own hours are limited.

If you rely on the income to pay bills, that strongly supports the IRS classifying your activity as a business.

This doesn't mean you have to depend on the activity entirely. But if you can show that the income plays a meaningful role in supporting your lifestyle, it works in your favor.

Example: A home baker whose sales cover a significant share of her monthly bills has a strong case. Someone with a six-figure salary who bakes on weekends and occasionally sells at farmers' markets has a weaker one.

Losses don't automatically make you a hobby. Every business loses money at some point, especially during startup or due to external factors like 2026's fluctuating material costs.

Keep records that show why you lost money, or the IRS may assume you never planned to make a profit.

Example: Lumber prices spiking and shipping costs doubling cause a custom furniture manufacturer to lose money for two years. Her invoices prove the costs, and a revised business plan shows she adjusted her prices. Another woodworker has lost money for five years but has no records explaining why. The first has evidence, while the second looks like a hobbyist.

The IRS looks for signs that you change course when plans don’t work out. If you dropped a slow-selling product or switched to a cheaper shipping vendor, that pivot proves you are chasing profit, not just pleasure.

Keep a simple decision log. Record what you changed, why you changed it, and the date. This demonstrates to the IRS that your approach is commercial, not recreational.

Example: A soap maker notices her gift sets sell well, but her individual bars barely break even. She scraps the individual bars and focuses on gift sets, negotiating with her packaging supplier to reduce costs so she can improve her profit margin. This type of decision, backed by documentation, is what the IRS looks for.

Your decision log doesn't need to show that every change worked. The IRS cares more about your intent, rather than how successful it was.

Consulting a CPA or industry expert shows the IRS you treat your venture as a commercial enterprise, not a personal interest. It demonstrates you take the activity seriously enough to pay for professional guidance.

You don’t need to take on a fractional CMO or CEO. A single consultation with an accountant about your tax obligations or a session with a small business tax service on pricing strategy can be compelling evidence.

Example: A personal trainer meets with a CPA each quarter to review his books and estimate his tax liability. This paper trail makes it hard for the IRS to dismiss his fitness business as a hobby.

A history of profitable ventures counts in your favor. It shows the IRS your track record of turning activities into profitable operations instead of abandoning them if they stop being fun or something else captures your attention.

You don’t need a string of high-profile exits to prove this. Modest profits from a previous side hustle or freelance business count.

Example: A jewelry maker who ran a profitable handmade greeting cards store on Etsy can highlight his experience to the IRS. Someone starting their first side-hustle doesn’t have this type of evidence, meaning the other eight factors are more important.

If you've made a profit in 3 of the last 5 years, the IRS presumes you're a business. But you still need records to defend that presumption.

This is sometimes called the "3-of-5 year rule". The IRS can still challenge your classification if other factors, like poor recordkeeping and no effort to reduce losses, indicate a hobby. The burden falls on you to back up those profitable years with documentation.

Example: A freelance graphic designer made a profit in 2022, 2023, and 2025 but posted losses in 2024 and 2026. The 3-of-5 rule is in her favor, but only if she can produce the Schedule C filings, bank statements, and expense records to prove those numbers are real.

You can enjoy your business, but the IRS needs to see that profit is the primary goal.

If the IRS believes personal satisfaction is the only thing driving the activity, with no real effort to turn a profit, they'll treat it as a hobby. The distinction comes down to what you actually do when the activity loses money, like raising prices or finding new customers.=

Example: Two people breed ferrets. One keeps track of every expense, markets each litter to find new owners, and adjusts pricing based on demand. The other only breeds her favorite variety, giving kits to her friends, and doesn’t track any transactions. Both enjoy what they do, but only the former shows the IRS that profit comes before pleasure.

Once you're classified as a business, you can deduct expenses that hobbyists cannot. But claiming deductions is only half the job, as you need to be ready to back up your classification if the IRS asks questions.

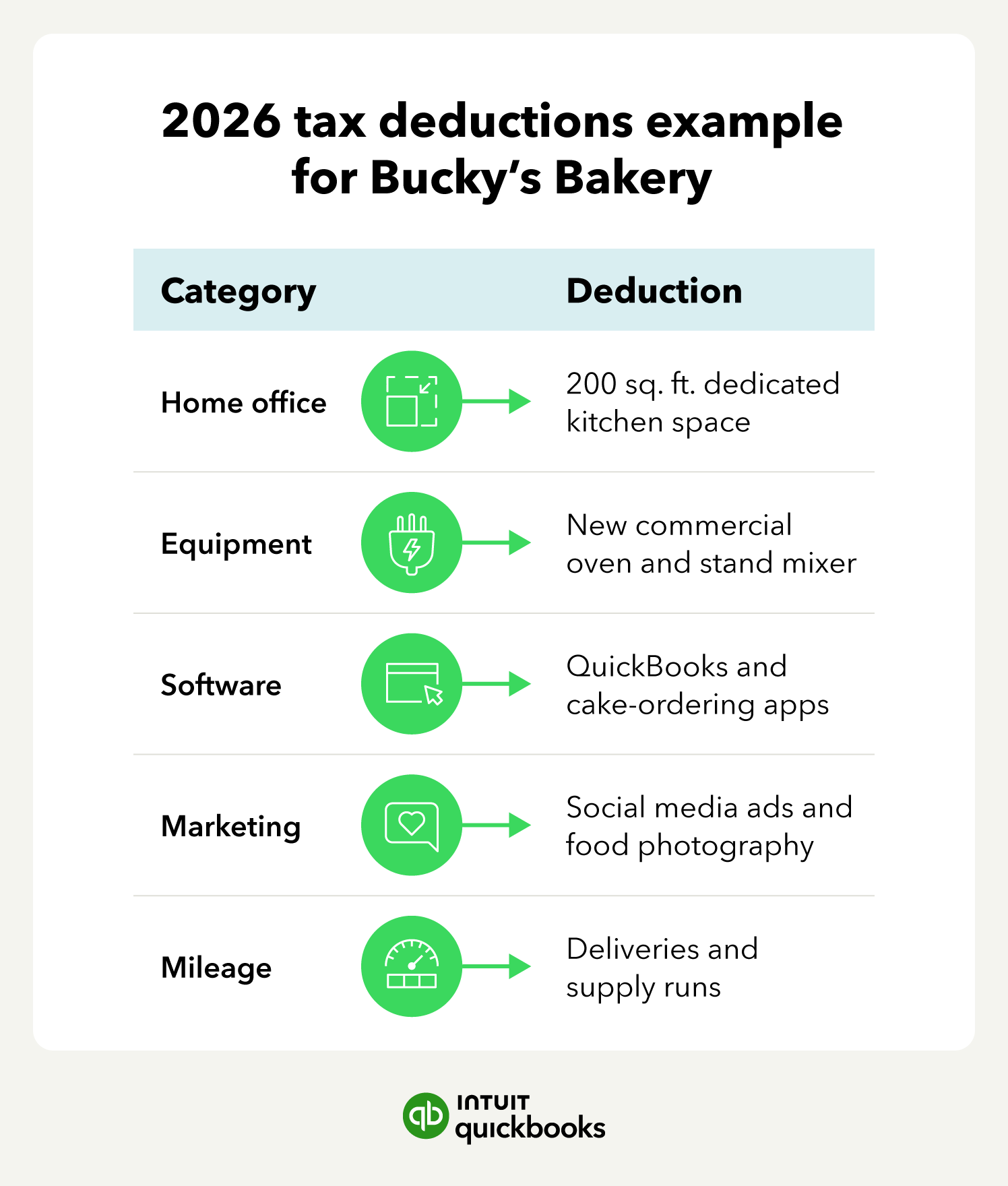

Once the IRS recognizes your activity as a business, you unlock deductions that hobbyists permanently lost under the OBBBA. Three categories matter most for solopreneurs filing in 2026:

If you sell physical products, you may also need to collect sales tax depending on your state.

The solopreneurs who survive IRS audits are the ones who kept clean records, not the ones who claimed the least. Every deductible expense should come from your business account, not your personal one. If you mix the two together, expect the IRS to question it.

QuickBooks Solopreneur lets you tag expenses as "business" or "personal" as they come in. This saves you from doing it later manually and creates a clean paper trail for your 2026 taxes.

Digital bookkeeping has changed what the IRS expects from business owners. While paper receipts fade and get lost, software timestamps, categorizes and backs up every transaction.

The solopreneurs most likely to struggle in an IRS audit are those who didn't keep evidence, not those who claimed too much.

The difference between a hobby and a business comes down to documentation. Log every expense, record every business decision, and separate your personal and business finances as they happen. Give the IRS the proof they need to classify you as a business and unlock the deductions that come with it.

QuickBooks Solopreneur is built for new businesses, freelancers, and side-hustlers. Start building the paper trail the IRS expects with our free QuickBooks Solopreneur option.

Call Sales: 1-800-285-4854