What are small business expenses?

Small business expenses are IRS-qualified expenses that you can subtract from your taxable income, such as advertising and marketing expenses, business bad debt, and business casualty losses.

When you’re a small business owner, tax tasks can feel overwhelming, especially figuring out which of your expenses are tax-deductible. Taking time away from the day-to-day management of your business to investigate every possible tax tip isn’t realistic.

Instead, be ready when it comes time to file small business taxes by using the following list as a rundown of possible deductions you can take when filing your taxes:

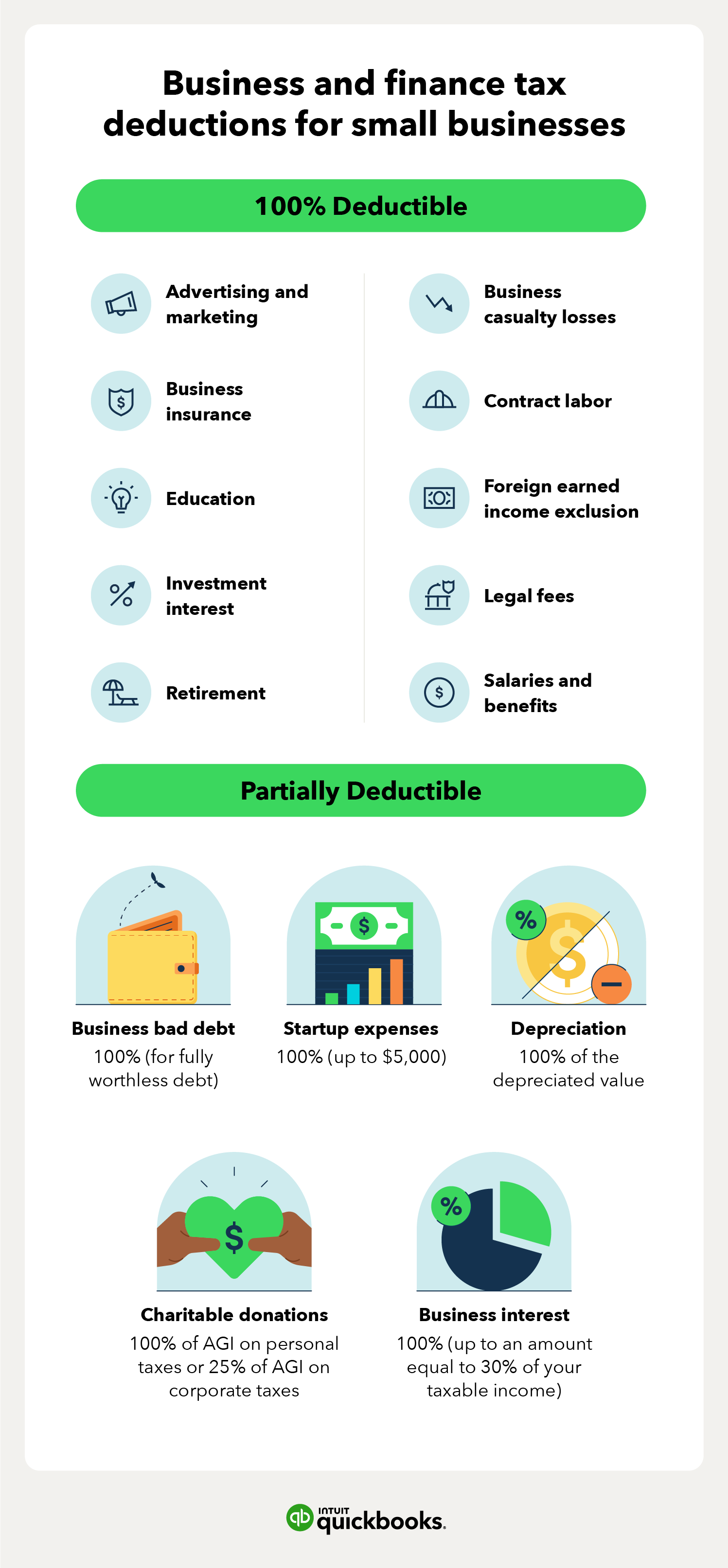

Advertising and marketing | Business bad debt | Business casualty losses | Business interest | Business meals | Business use of car | Charitable donations | Contract labor | Depreciation | Education | Foreign earned income exclusion | Gifts for employees and clients | Home office expenses | Legal fees | Moving expenses | Office supplies and expenses | Phone and internet expenses | Rent | Retirement | Salaries and benefits | Startup expenses | Travel expenses

1. Advertising and marketing

If you pay for advertising or marketing to promote your small business, those costs are fully tax deductible. They qualify as long as the expenses are considered ordinary, reasonable, and necessary.

Costs that the IRS considers primarily personal or lobbying are exempt from deduction, even if they have some promotional value.

- Percentage deductible: 100%

- Eligibility: Any marketing or advertising expenses spent on campaigns to keep or attract customers

- Business expense examples: Costs of producing physical marketing materials such as business cards or flyers, as well as advertising costs for TV, radio, print, and online

2. Business bad debt

When someone owes your business money, and you can’t collect it, this is a bad debt. Bad debt expenses can happen if you sell a good or service to a customer with the understanding that they’ll pay you later (in other words, on credit), and it becomes clear they aren't paying.

Business bad debts can be fully or partially worthless—meaning you’ve collected some but not all of the debt. Consult a tax professional to make sure you’re claiming the correct amount as a deductible.

- Percentage deductible: 100% (for fully worthless debt)

- Eligibility: The debt in question must be partially or fully worthless to be considered deductible. Worth is based on the understanding that the amount owed will be paid back

- Business expense examples: Loans to clients or suppliers, credit sales to customers, and business loan guarantees

3. Business casualty losses

This deduction applies if your business suffers theft or physical damage.

Long-term losses include things like erosion, wood decomposition, and termite damage are considered long-term losses. They don’t count as business casualty losses.

- Percentage deductible: 100%

- Eligibility: You must be the owner of the property, and the loss must be the result of a sudden, unpredictable event

- Business expense examples: Natural disasters, vandalism, or burglary

4. Business interest

If you take out a loan for business purposes—including a mortgage on business real estate—or obtain a line of credit for business purchases, the interest you pay is tax deductible. However, there is a limit to this. The interest expense deduction is currently 30% of your taxable income.

What does that mean? Say you take out a loan for your small business, and you pay interest on it. If your taxable income is $100,000 and you paid $60,000 in interest on your loan, you could claim a $30,000 deduction (30% of your taxable income) as a tax write-off.

- Percentage deductible: 100% (up to an amount equal to 30% of your taxable income)

- Eligibility: You are legally liable for the acquired debt, and you and the lender have a true debtor-creditor relationship

- Business expense examples: Interest on purchases made on credit for inventory stock and interest on credit card debt

5. Business meals

Business meals for employees, clients, and potential clients can be tax deductible, depending on the purpose of the meal.

Meal costs must be considered reasonable to be eligible, and they have to be purchased from a restaurant to be 100% deductible. Exorbitant prices for extravagant meals likely won’t qualify as a deductible business expense.

- Percentage deductible: 100% for company-wide parties or your own meals as part of doing business. 50% for office snacks and meals or business meals with clients

- Eligibility: The expense must be reasonable and not extravagant or excessive, and you or an employee must be present

- Business expense examples: Meal expenses while traveling on business or food and beverage expenses during social company activities, including holiday parties and happy hours

6. Business use of car

You can deduct the associated costs if you use your vehicle for business purposes. This means you’ll need to keep track of your mileage outside if your car is used for both business and personal use. For 2026, the standard mileage rate for operating a business vehicle is 70 cents per mile.

If you use the vehicle for both business and personal purposes, you must split the costs based on mileage. Vehicles used as equipment—such as dump trucks—and vehicles used for hire, like taxis and airport shuttle vans, do not qualify.

- Percentage deductible: 100%

- Eligibility: Vehicle use for business purposes

- Business expense examples: Registration fees and taxes, fuel, insurance, and maintenance and repairs

7. Charitable contributions

If you’re interested in giving back to your community through charitable donations, you can deduct the entire amount contributed.

If your business is set up as a sole proprietorship, LLC, or partnership, you can claim charitable donations on your personal taxes.

- Percentage deductible: 100% of adjusted gross income on personal taxes and 25% of adjusted gross income on corporate taxes.

- Eligibility: To qualify, you must give a cash donation to a qualifying organization

- List of business expenses examples: Donations to a church, synagogue, or other religious organization

8. Contract labor

If you paid a freelancer or independent contractor to work for your small business, you can deduct their fees as a business expense. Note that you’ll want to send freelancers and contractors a Form W-9 to collect their tax information before starting work.

If you pay a contractor $600 or more during the tax year, you’ll send them a Form 1099-NEC by January 31 of the following year. They’ll need this when they’re doing their taxes.

- Percentage deductible: 100%

- Eligibility: The freelancer or contractor is not an employee of your small business.

- Business expense examples: You pay an independent accountant to review your small business taxes.

9. Depreciation

Depreciation enables you to recover the costs of fixed and tangible assets over time. In other words, small business owners can regain costs associated with an asset’s age, wear, tear, and decay over its usable lifetime.

Bonus depreciation lets you claim a larger depreciation expense on assets purchased within the tax year. With bonus depreciation, you can deduct up to 100% of an asset’s cost.

- Percentage deductible: 100% of the depreciated value

- Eligibility: You use the asset as part of your income-generating operations, and the asset has an estimated life expectancy of more than one year

- List of business expenses examples: Computers, machinery, and office furniture

10. Education

If you provide yourself or your employees with qualifying educational benefits, you can deduct the costs. Tax-deductible education expenses include continuing education and courses for professional licenses.

You can’t deduct educational expenses that qualify you or an employee for a different trade. Courses necessary to meet the minimum education requirement for the job don’t count.

- Percentage deductible: 100%

- Eligibility: Deductible education costs must add value to the business and increase the workforce’s expertise and skills

- Business expense examples: Subscriptions to professional publications or industry-related seminars, webinars, and retreats

11. Foreign earned income exclusion

If you’re a US citizen and own a small business in another country, under certain circumstances, you can exclude your foreign income from your US business tax return. Essentially, the foreign-earned income exclusion prevents you from getting taxed twice.

The money you receive as a distribution of earnings and profits—rather than reasonable compensation—does not qualify.

- Percentage deductible: 100%

- Eligibility: You are a US citizen or resident alien, have a qualifying presence in a foreign country met by the Bonafide Resident Test, and have paid foreign taxes on foreign-earned income

- Business expense examples: Any foreign income earned and taxed in a foreign country

12. Gifts for employees and clients

If you give each employee a gift during the holidays or send a client a fruit basket to thank them for their patronage, you can deduct the costs of these gifts, with limitations. Make sure you keep records that prove the business purpose of the gift and show the amount spent.

When you’re calculating the $25-per-person limit, there’s no need to count gifts that cost you $4 or less that have your business name on them, like stickers or stress balls.

- Percentage deductible: 100% up to $25 per person

- Eligibility: It’s a tangible gift and not entertainment

- Business expense examples: An employee has a baby, and you send them a gift basket with baby items

13. Home office expenses

Many small-business owners—especially contractors and freelancers—work from a home office. If you use a home office, you might be able to deduct the costs of creating and maintaining your workspace.

There are two primary methods for taking home office deductions: simplified and regular. The simplified method is easier but could result in a smaller tax break, while the standard method requires a bit more math and precise recordkeeping but could get you a larger deduction.

- Percentage deductible: Based on what percentage of your home you use for business. You can divide the office square footage by the total square footage of your home to find the percentage

- Eligibility: Though it doesn’t need to be in a separate room, your office must be in a space solely designated to work and business operations

- Business expense examples: A portion of utility bills and homeowners insurance

14. Legal fees

Any legal fees that your small business pays can qualify as tax-deductible, including any fees in legal cases that you didn’t win.

Any legal or professional fees related to personal issues, including child custody and personal injury and property claims, are not deductible.

- Percentage deductible: 100%

- Eligibility: The expenses you incur must be considered ordinary and necessary to the business.

- List of business expenses examples: Fees for resolving tax issues.

15. Moving expenses

If you moved your business, you might be able to deduct any expenses associated with the move.

Moving expenses that don't directly correlate to the business move are no longer deductible. Personal moving expenses are exempt, although some exceptions exist for military members.

- Percentage deductible: 100%

- Eligibility: The costs of transporting business equipment, supplies, and inventory typically qualify as deductible

- Business expense examples: Transporting inventory stock or relocating machinery

16. Office supplies and expenses

Necessary supplies for running and maintaining a functional office are fully tax-deductible tax breaks.

If you bought a large number of office supplies on December 31, you can’t deduct that cost this year because it’s highly unlikely you used all of those supplies in the past year.

- Percentage deductible: 100%

- Eligibility: Deducting these items must not significantly skew your business’s income

- Business expense examples: Printers, ink cartridges, pens, and paper

17. Phone and internet expenses

If you use a phone and internet for your small business, those costs qualify as eligible deductions.

If you also use your work phone and Internet for personal use, you can only deduct the percentage of the cost you use for business purposes.

- Percentage deductible: 100%

- Eligibility: Phone and internet usage must be essential to your business operations

- Business expense examples: Internet and phone service

18. Rent

If you rent office space, a warehouse, or any other type of business property, you can qualify as a business expense on your taxes. A rent payment is any amount you pay to use the property for your small business that you don’t own.

If you have or will eventually receive equity in or title to the property in question, rent expenses are not eligible. If you use a home office, you might be eligible to write off a portion of the cost.

- Percentage deductible: 100%

- Eligibility: You must use the property for business purposes

- Business expense examples: Rent for a building or office space

19. Retirement

As a small business owner, you are responsible for funding your retirement plan, such as your 401(k). Fortunately, your contributions are tax-deductible.

If you have employees, your selected retirement plan must benefit all employees, not just you.

- Percentage deductible: 100%

- Eligibility: Retirement accounts must comply with IRS regulations and be deemed tax-qualified.

- Business expense examples: Contributions made to tax-qualified retirement plans, such as a Roth IRA, Simple IRA, or Solo 401(k).

20. Salaries and benefits

If you’re a small business owner with one or more employees, you can deduct the cost of the employee's salaries, benefits, and vacation pay. This includes regular wages, commissions, and bonuses.

Generally, the IRS does not challenge itemized salary and benefits deductions. However, there are some cases when the IRS will deem a deduction unreasonable—for example, if the employee is an investor or a personal acquaintance.

- Percentage deductible: 100%

- Eligibility: The employee must not be the sole proprietor, a partner, or an LLC member, and the salaries and benefits must be reasonable, ordinary, and necessary.

- List of business expenses examples: Employee salaries, paid time off, and commission or bonuses

21. Startup expenses

The IRS allows you to deduct up to $5,000 in startup costs so long as those expenses do not exceed $50,000. If your startup expenses exceed $50,000, your deduction will be reduced.

If you are buying tangible assets for your business that you will use for more than one year, the costs of these assets must be depreciated over their lifespans.

- Percentage deductible: 100% (up to $5,000)

- Eligibility: A startup cost is deductible if you incurred it before the day your business began, and it is a cost you would normally deduct when operating an existing business

- Business expense examples: Marketing, travel costs, and training costs.

22. Travel expenses

If you travel to meet a client, attend a conference, or for any other business-related reason, you can write off your travel expenses.

If most of your trip is spent doing business-related things, the IRS considers this a vacation, and your expenses aren’t deductible. Make sure to save documentation that proves your trip was for business.

- Percentage deductible: 100%

- Eligibility: For a trip to qualify as business travel, it must be considered ordinary, necessary, and to a destination away from the state you do business in

- Business expense examples: Plane, train, or bus tickets, and fares for taxis, Ubers, or other transportation

Best practices for managing small business expenses

Maintaining control over your expenses allows you to make informed financial decisions.

Small business owners can improve their expense tracking with a few easy steps:

- Create a budget: A detailed budget helps you outline your expected income and expenses and can serve as a roadmap for your financial planning.

- Track every expense: Record all your business expenses, no matter how small they are, which includes keeping your invoices and receipts.

- Properly categorize expenses: Organizing your expenses into categories like office supplies and utilities will give you a better understanding of how you're managing your money.

- Reconcile accounts often: Make sure your bank account and accounting records match to avoid discrepancies or errors.

- Use accounting software: Accounting software helps streamline

Streamline your accounting and save time

Running a business is rewarding but can come with many learning curves—like having to track your expenses and do your taxes. Luckily, small business accounting software like QuickBooks Online can help make the process less taxing by helping you track expenses throughout the year—either on your own or with the help of a virtual bookkeeper.

Small business expenses FAQ

Marshall Hargrave is a financial writer with nearly two decades of experience in finance, investing, and tax industries. He’s helped create and edit content for the likes of Investopedia, Robinhood, Fortune, and Yahoo! Finance. He’s also supported startups and small businesses with accounting, bookkeeping, and budgeting and worked with various finance organizations like the Consumer Bankers Association and the National Venture Capital Association. Marshall is a former Securities & Exchange Commission-registered investment adviser with a bachelor's degree in finance from Appalachian State University.

Call Sales: 1-877-866-5232