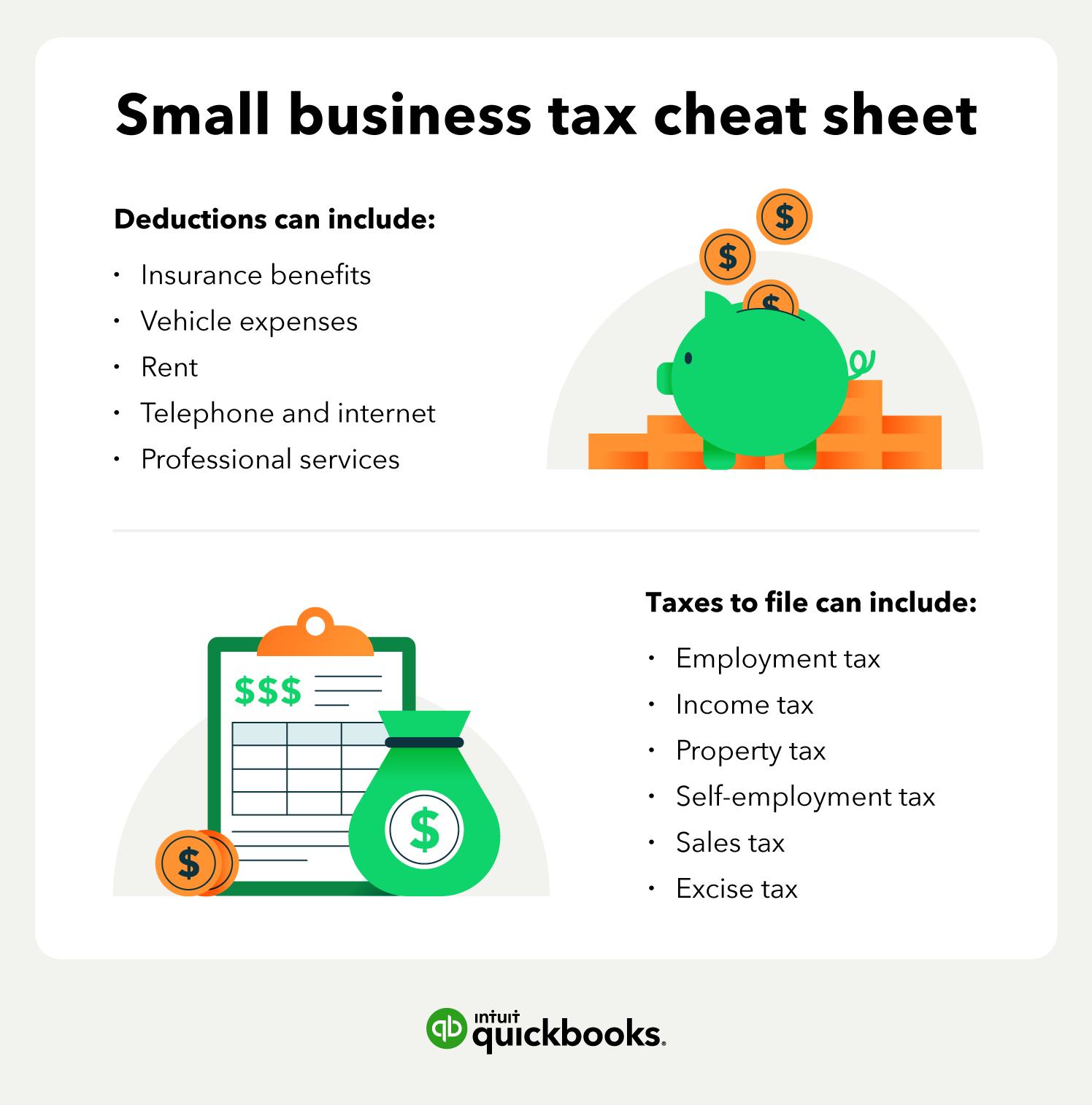

Types of business taxes in Arizona

As an Arizona employer, you may be responsible for reporting and paying other business taxes in addition to withholding payroll taxes from your employees' paychecks. From federal to state and local levels, understanding the different tax programs and their impact on your business’s finances is important.

Federal taxes

You'll be responsible for federal taxes in whatever state you open a business in. Unfortunately, there are dozens of federal tax forms with unique due dates and requirements. Using an accountant or small business accounting software can be helpful in avoiding mistakes that can lead to overpayment or penalties.

As a business owner, you have both personal and business tax filing obligations. Here’s what you need to know:

Personal tax filing

Federal income tax returns:

Every individual is required to file and pay federal personal income tax. This forms the foundation of your overall tax responsibility.

Business tax filing

Business owners have additional filing requirements, depending on the business structure:

- Sole proprietorship: Income and expenses are reported on your personal tax return using Schedule C (Form 1040).

- Partnership: A partnership must file an information return (Form 1065) to report income, deductions, and other relevant details, while each partner reports their share of income on their personal return.

- Corporation: A corporation files a corporate tax return (Form 1120), paying taxes on its profits.

- S Corporation: An S corporation files an informational return (Form 1120S). Its income, losses, and deductions pass through to shareholders, who report them on their personal returns.

- Limited Liability Companies (LLCs): LLCs are not classified separately for federal tax purposes and are taxed based on their ownership structure. Single-member LLCs default to sole proprietorship taxation or may elect corporate taxation, while multi-member LLCs default to partnership taxation or may elect corporate taxation.

Self-employment tax

If you work for yourself and earn more than $400 a year, you pay toward Social Security and Medicare programs through a self-employment tax. The Social Security system provides retirement benefits, disability benefits, survivor benefits, and hospital insurance (Medicare) benefits.

Employment taxes

As an employer, you are responsible for withholding and depositing federal income tax and the employee contribution to Social Security and Medicare taxes. You must also pay the employer portion of Medicare and Social Security and pay federal unemployment tax (FUTA).

State taxes

As a business owner, understanding your state tax obligations is an integral part of running your organization.

Corporate income tax

Paying corporate income tax is necessary for any C corporation in Arizona. The corporate income tax rate is currently 4.9% on net income generated.

How is the corporate income tax calculated?

In Arizona, corporate income tax is calculated starting with federal taxable income as reported on the corporation's federal tax return. This amount is then adjusted according to Arizona state tax laws to arrive at Arizona taxable income. Adjustments may include specific additions or subtractions required by the state, such as:

Additions:

- State and local income taxes deducted on the federal return

- Interest income from non-Arizona municipal bonds

Subtractions:

- Dividends received from another corporation if they were included in federal taxable income

- Interest income from U.S. government obligations like Treasury bonds.

These adjustments ensure the taxable income aligns with Arizona's regulations. For corporations operating in multiple states, the adjusted income is apportioned based on the proportion of sales, property, and payroll in Arizona. The state corporate income tax rate is then applied to determine the final tax liability.

Who may be liable for corporate income tax?

In Arizona, corporations are subject to corporate income tax if they generate income from business activities within the state. This includes both domestic corporations (incorporated in Arizona) and foreign corporations (incorporated elsewhere but conducting business in Arizona). Liability is determined based on the concept of nexus, which establishes a business's connection to the state.

Nexus refers to the level of presence or activity a business has in Arizona that justifies its obligation to pay state taxes. Nexus can be established through various means, such as:

- Owning or leasing real or personal property in Arizona

- Maintaining an office or place of business within the state

- Employing staff in Arizona to conduct business activities

- Delivering merchandise into Arizona using company-owned or leased vehicles

- Utilizing independent contractors or representatives to establish and maintain a market presence in the state

- Generating gross income exceeding $100,000 annually from Arizona customers as a remote seller or marketplace facilitator

Once nexus is established, the corporation must file Arizona corporate income tax returns and pay taxes on income apportioned to the state.

For detailed guidance on nexus and tax liability, businesses can refer to the Arizona Department of Revenue's Nexus Program for Corporate Income Tax.

Franchise taxes in Arizona

Franchise (or privilege) taxes are imposed on certain companies based on their privilege to operate within a specific state. Arizona does not have a franchise tax. However, it does have a Transaction Privilege Tax (TPT).

Transaction Privilege Tax (TPT)

Arizona's Transaction Privilege Tax (TPT) is a tax on the privilege of conducting business within the state, levied on vendors rather than consumers. Businesses engaged in taxable activities are responsible for obtaining a TPT license and remitting the tax to the Arizona Department of Revenue.

What is the Transaction Privilege Tax rate?

The state imposes a base TPT rate of 5.6% on most business classifications. In addition to the state rate, counties and cities may levy their own TPT rates, which vary by location and type of business activity.

Excise taxes

In Arizona, excise taxes are imposed on specific goods and services in addition to the general Transaction Privilege Tax (TPT). Notable excise taxes include:

- Liquor Luxury Tax: Spirituous liquor is taxed at $3.00 per gallon, vinous liquor (wine) at $0.84 per gallon, and malt liquor (beer) at $0.16 per gallon.

- Gasoline and diesel: Both are taxed at a flat rate of $0.18 per gallon.

- Tobacco Luxury Tax: A $2.00 excise tax is applied per pack of 20 cigarettes.

- Adult use (recreational) marijuana: Subject to a 16% excise tax, in addition to the standard state and local TPT rates.

It’s important to review which special taxes may apply to your Arizona business.

Unemployment tax

As in all states, employers in Arizona are required to pay federal unemployment insurance (UI) taxes. Arizona employers also fully fund state unemployment insurance. State UI tax is applied to each employee's wages up to a maximum annual amount, referred to as the "taxable wage base" or "taxable wage limit."

For 2025, the taxable wage limit for Arizona UI tax is $8,000. Rates for established employers range from 0.04% to 9.72%, depending on the business’s ratio rating. New employers are assigned a standard tax rate of 2%.

Employers are notified of their specific tax rates annually via a "Determination of Unemployment Tax Rate" notice provided by the Arizona Department of Economic Security.

Local taxes

In addition to federal and state taxes, many cities, counties, and other jurisdictions in Arizona levy other kinds of local taxes to fund essential services and infrastructure such as schools, roads, police, and fire protection. These taxes often include local sales taxes, property taxes, and specific use taxes.

Sales and use taxes

Unlike some states that combine their sales and use taxes into a single payment, Arizona separates them into distinct categories.

TPT

Arizona's Transaction Privilege Tax (TPT), as mentioned above, is functionally the same as sales tax. Even though it is imposed on the sellers, they, in turn, will generally pass this tax to customers—hence, a sales tax.

The state's base TPT rate is 5.6%. However, local jurisdictions and counties can impose additional taxes, resulting in combined rates that can exceed 11.2%, depending on the location.

Use tax

In addition to the TPT, Arizona also imposes a use tax. This tax applies when tangible personal property is purchased but the seller doesn’t collect the required tax. Businesses are responsible for use tax if:

- They buy goods from an out-of-state retailer or utility business for use, storage, or consumption in Arizona.

- They use a resale certificate for purchases, but the goods are later used or consumed in Arizona in a way that doesn’t match the certificate's intended purpose.

- They purchase goods from another state where the sales tax or excise tax rate is lower than Arizona’s use tax rate.

Visit the Arizona Department of Revenue website for details.

Remote seller tax considerations

Remote sellers—businesses without a physical presence in Arizona—must collect and remit Transaction Privilege Tax (TPT) if their gross sales into the state exceed $100,000 in the current or previous calendar year. Once this threshold is met, they must register for a TPT license via the Arizona Department of Revenue website and collect tax on future sales.

These requirements apply only to remote sellers and out-of-state marketplace facilitators; businesses with a physical presence in Arizona must comply with TPT regardless of sales volume. Remote sellers should review their Arizona sales annually to ensure compliance.

For detailed information and guidance on remote seller taxes, refer to the Arizona Department of Revenue website and consult with a tax professional to ensure compliance with all tax obligations.

Property taxes

All property taxes in Arizona are calculated at a county level. You can learn more about specific county property tax rates on the Arizona Department of Revenue's property tax website.