1. Limited visibility into inventory’s impact on cash flow

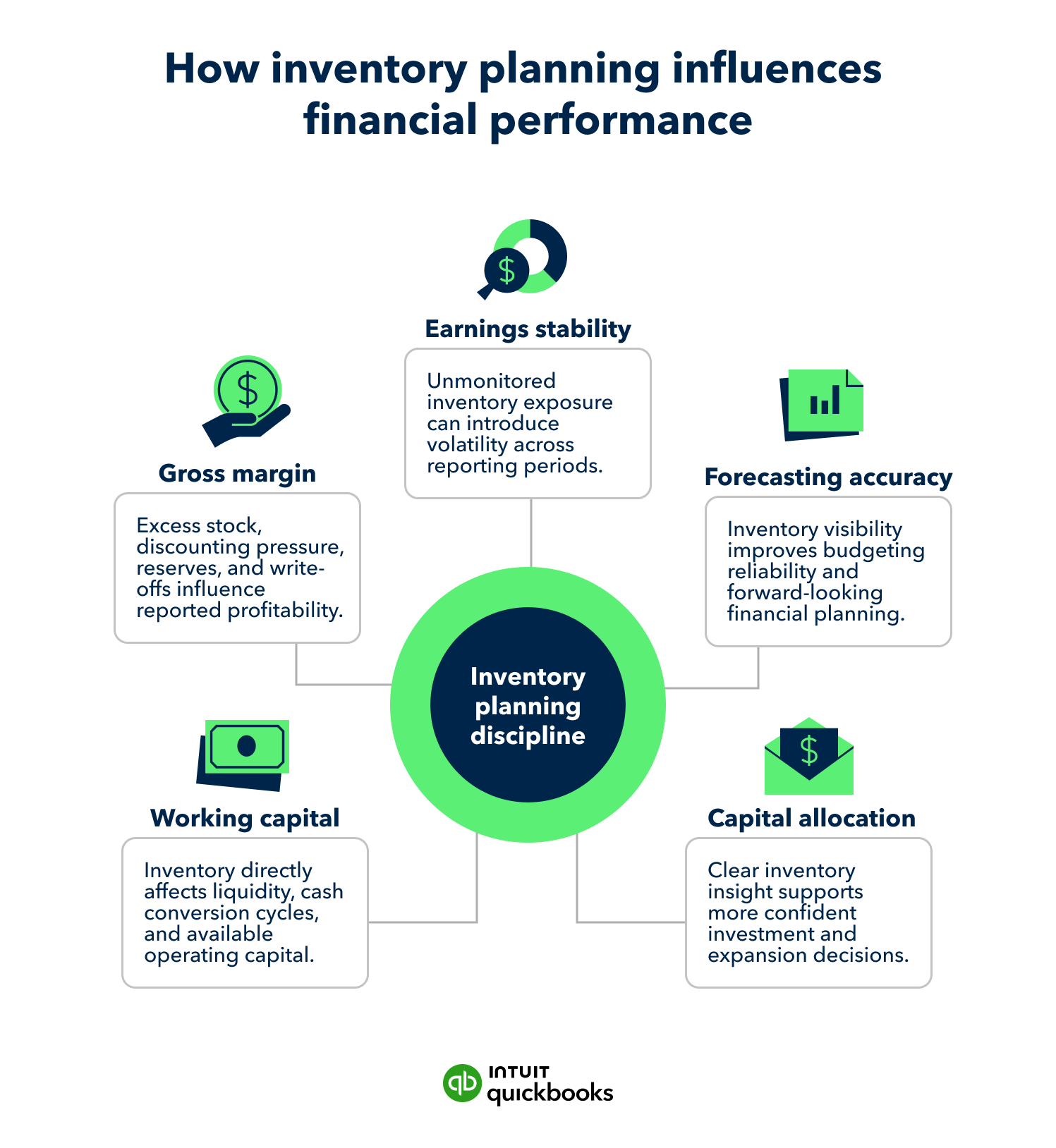

Inventory is typically one of the biggest demands on working capital for product-based businesses. And every dollar tied up in stock is a dollar you can’t put toward hiring, marketing, growth initiatives, or paying down debt.

When you don’t have clear, consistent financial visibility, inventory can quietly creep up over time, while available cash gets tighter. On paper, profitability may still look strong, but day-to-day liquidity starts to feel constrained. And because inventory is less liquid than receivables or cash, it can also weaken certain liquidity ratios if it grows out of proportion to sales. This expands balance sheet exposure and extends the cash conversion cycle.

That’s why finance teams need real-time insight into how inventory impacts the cash conversion cycle and, ultimately, how much flexibility the business has to allocate capital with confidence.

The financial risk

When inventory grows without corresponding revenue increases, several financial risks emerge:

- Lengthening cash conversion cycles: Excess stock extends the time between cash outflow and cash recovery

- Constrained working capital: Tied-up capital reduces flexibility for strategic investments

- Balance sheet strain: Elevated inventory levels increase asset concentration and reduce liquidity resilience

- Reactive liquidity management: Without early signals, finance teams respond to liquidity strain rather than preventing it

- Covenant and credit risk: Potential pressure on loan covenants and access to credit if cash generation slows while inventory builds

How finance teams address it

Finance leaders keep a close eye on inventory value alongside revenue and cash flow, because the relationship between the three tells an important story. Metrics like inventory turnover and inventory-to-revenue ratios can surface early warning signs, especially when stock levels start rising faster than demand. They also monitor days inventory outstanding as part of the broader cash conversion cycle, alongside days sales outstanding and days payable outstanding.

Timely financial reporting allows leadership to adjust purchasing, production, or pricing decisions before liquidity strain becomes material. Instead of reacting after cash tightens, teams can course-correct early and protect working capital.

Platforms like QuickBooks Online Advanced provide real-time visibility into inventory value and financial performance. That access to current data helps reduce margin surprises and supports steadier, more predictable cash flow.