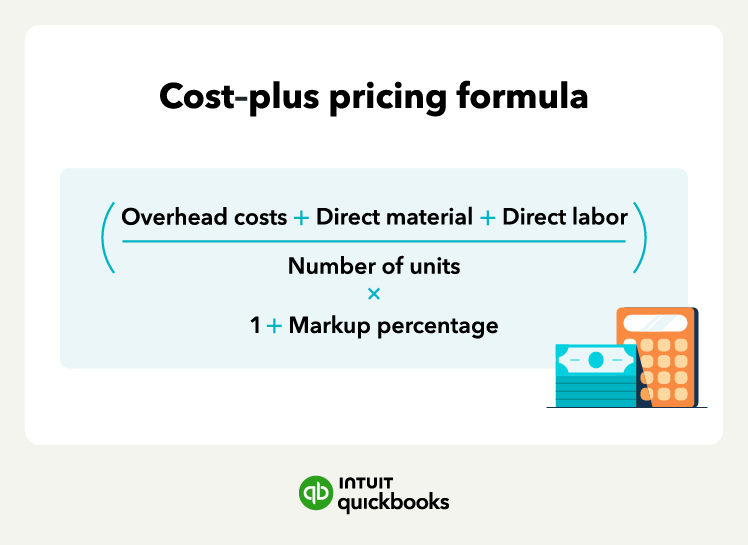

Cost-plus pricing (also known as markup pricing) is a straightforward method to ensure your business stays profitable from day one. Unlike competitive pricing or dynamic pricing, which rely on external market shifts, this approach focuses entirely on factors within your control.

This is especially important as a new wave of entrepreneurs enters the market. Recent QuickBooks data shows that 47% of aspiring small business owners cite cost as their biggest barrier to starting up.

The best part is that you can calculate your rates using the data already sitting in your accounting software. Here’s how to use cost-plus pricing to protect your margins and grow your business.

Jump to: