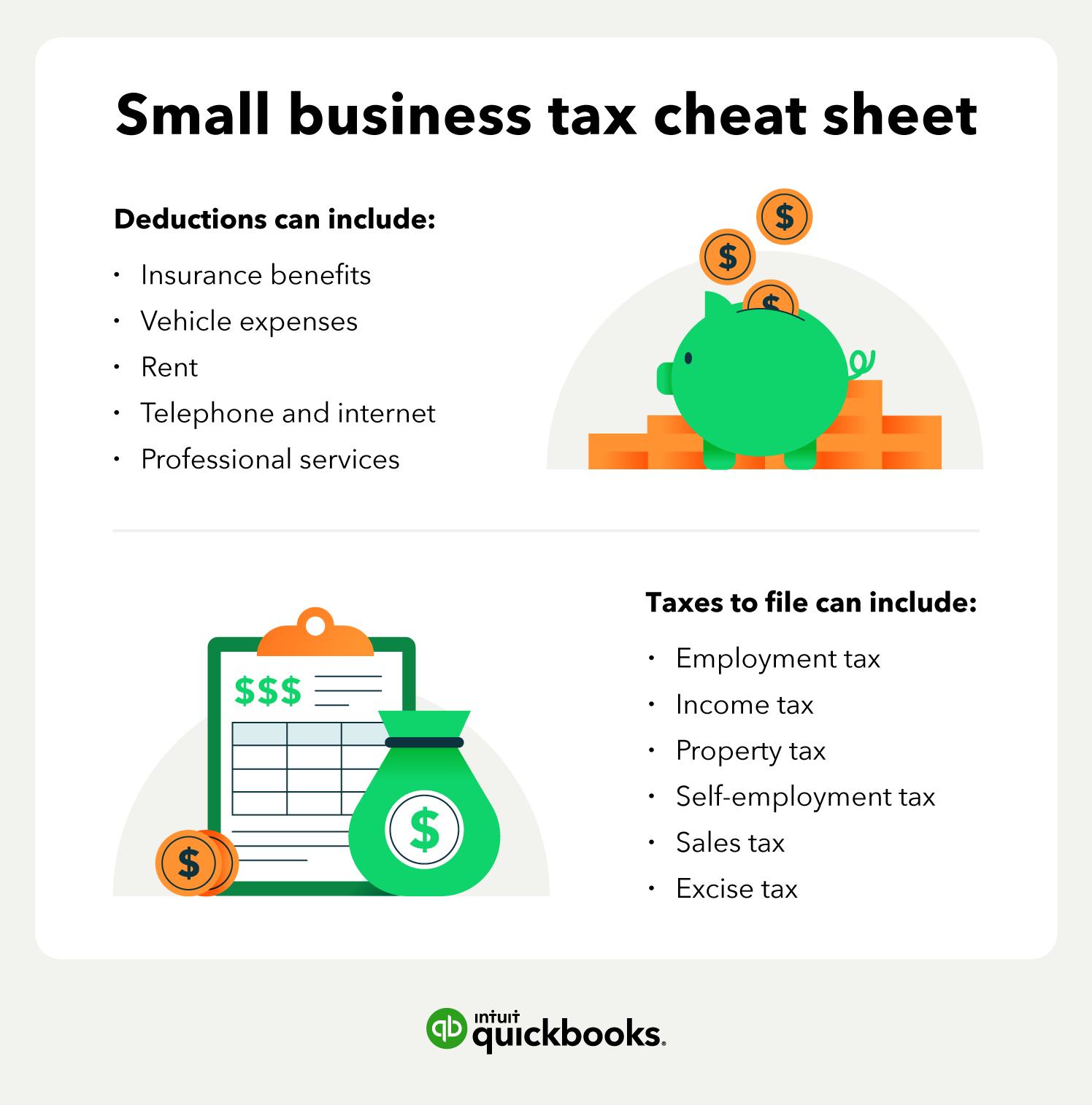

Types of business taxes in Oregon

As an employer in Oregon, you may be responsible for reporting and paying other business taxes in addition to withholding payroll taxes from your employees' paychecks. The Oregon paycheck calculator makes it easy to estimate withholdings and net pay. From federal to state and local levels, it’s important to understand the different tax programs and their impact on your finances.

Federal taxes

Regardless of which state you open a business in, you'll be responsible for federal taxes. There are dozens of federal tax forms with unique due dates and requirements, so using an accountant or small business accounting software can help you avoid mistakes that could lead to overpayment or penalties.

As a business owner, you have both personal and business tax filing obligations. Here’s what you need to know:

Personal tax filing

Federal income tax returns:

Every individual is required to file and pay federal personal income tax. This forms the foundation of your overall tax responsibility.

Business tax filing

Business owners have additional filing requirements, depending on the business structure:

- Sole proprietorship: Income and expenses are reported on your personal tax return using Schedule C (Form 1040).

- Partnership: A partnership must file an information return (Form 1065) to report income, deductions, and other relevant details, while each partner reports their share of income on their personal return.

- Corporation: A corporation files a corporate tax return (Form 1120), paying taxes on its profits.

- S Corporation: An S corporation files an informational return (Form 1120S). Its income, losses, and deductions pass through to shareholders, who report them on their personal returns.

- Limited Liability Companies (LLCs): LLCs are not classified separately for federal tax purposes and are taxed based on their ownership structure. Single-member LLCs default to sole proprietorship taxation or may elect corporate taxation, while multi-member LLCs default to partnership taxation or may elect corporate taxation.

Self-employment tax

If you work for yourself and earn more than $400 a year, you pay toward Social Security and Medicare programs through a self-employment tax. The Social Security system provides retirement benefits, disability benefits, survivor benefits, and hospital insurance (Medicare) benefits. As of 2024, the federal self-employment tax rate is 15.3%. 2.9% of this goes to Medicare, and 12.4% goes to Social Security. The Social Security portion applies to the first $168,600 of net earnings for 2024.

Employment taxes

As an employer, you are responsible for withholding and depositing federal income tax and the employee contribution to Social Security and Medicare taxes. You must also pay the employer portion of Medicare and Social Security and pay federal unemployment tax (FUTA).

State taxes

As a business owner, you must understand your state tax obligations.

Oregon franchise tax

Oregon doesn't actually have franchise taxes, but the state does impose a privilege tax on companies that sell certain products. This tax differs from those in other states because it is not charged to every business.

What is the franchise tax rate?

Again, Oregon has a privilege tax, not a franchise tax. This rate is $2.60 per barrel for companies that sell wine, malt beverages, and cider. There is also a tax of $25 imposed per ton of grapes sold to make wine. And vehicle sellers must pay .005 % of the retail price.

How is the franchise tax calculated?

In Oregon, the state doesn’t impose a traditional franchise tax but uses privilege taxes in its place. Here’s how these taxes are calculated:

Alcoholic Beverage Privilege Tax

- For malt beverages (beer): $2.60 per barrel (31 gallons).

- For wine and cider:

- $0.67 per gallon for wine with alcohol content below 14%.

- $0.77 per gallon for wine with alcohol content between 14% and 21%.

- $0.08 per gallon for cider with alcohol content below 7%.

The tax is calculated based on the volume of beverages manufactured or imported into Oregon. Businesses must file monthly reports and pay the tax for beverages removed from bonds or imported. See the Oregon Liquor and Cannabis Commission for more information.

Vehicle Privilege Tax

The tax is 0.5% (0.005) of the retail sales price of new vehicles sold in Oregon. For example, if a new vehicle is sold for $40,000, the privilege tax would be $200. Dealers are responsible for collecting and remitting this tax. Visit the Oregon Department of Revenue for more information.

Who may be liable for the franchise tax?

Liability for Oregon's privilege taxes depends on the specific tax:

- Alcoholic beverages: Manufacturers in Oregon and importing distributors are responsible for filing privilege tax reports and remitting the tax.

- Vehicles: Oregon vehicle dealers are responsible for paying the Vehicle Privilege Tax but may collect the amount from the buyer.

There are certain instances when an Oregon business does not have to pay their privilege tax. For example, vehicle sellers are exempt if the seller receives a resale certificate from the buyer, and the buyer typically sells vehicles.

Excise taxes

Excise taxes are special taxes imposed on specific goods or services. In Oregon, these taxes apply to a wide range of products and activities, including:

Alcoholic beverages: Oregon imposes a privilege tax on the manufacturing and importing of alcoholic beverages (see previous section for rates).

Tobacco products: Oregon levies taxes on the distribution of cigarettes and other tobacco products.

- Cigarettes: $3.33 per pack of 20 cigarettes

- Cigars: 65% of the wholesale sales price, with a maximum tax of $1 per cigar

- Moist snuff: $1.80 per ounce, with a minimum tax of $2.17 per retail container

- All other tobacco products: 65% of the wholesale sales price

Marijuana products: Oregon imposes a tax on the retail sale of marijuana items. Retail sales tax is 17% of the retail sales price. Cities and counties may levy an additional local tax of up to 3%

Motor vehicle fuel: The state imposes a tax on motor vehicle fuels:

- Gasoline and diesel: $0.40 per gallon

- Aviation gasoline: $0.11 per gallon.

- Liquefied petroleum gas (Propane): $0.40 per 1.353 gallons

Corporate excise tax: Corporations doing business in Oregon are subject to a corporate excise tax, which is a tax for the privilege of doing business in the state. The tax rate is 6.6% on Oregon taxable income of $1 million or less and 7.6% on Oregon taxable income above $1 million. The minimum excise tax ranges from $150 to $100,000 based on Oregon sales.

Unemployment taxes

In Oregon, employers are responsible for funding state unemployment insurance (UI) taxes. These taxes are applied to each employee's wages up to a specified annual limit, known as the "taxable wage base" or "taxable wage limit."

For 2024, the taxable wage base is $52,800 per employee. Rates range from 0.9% to 5.4%. The new employer rate is 2.4%. There’s also a special payroll tax offset of 0.109% for all quarters.

Local taxes

Depending on where you live in Oregon, certain local jurisdictions impose taxes that your business should be aware of:

Prepared food and beverage taxes

The city of Ashland levies a 5% tax on the sale of prepared food and beverages. This tax applies to items sold by restaurants, caterers, and similar establishments.

Arts education and access income tax

Portland assesses a flat tax of $35 on residents aged 18 and over who have an income of $1,000 or more annually and reside in households above the federal poverty level. The revenue supports arts education and nonprofit organizations within the city.

Local marijuana taxes

In addition to the state's 17% tax on recreational marijuana sales, many Oregon cities and counties impose an additional local tax of up to 3%. The Oregon Department of Revenue collects these local taxes on behalf of participating jurisdictions.

Transient lodging taxes

Oregon imposes a 1.5% statewide lodging tax on short-term accommodations. Additionally, many local governments levy their own lodging taxes, which can vary by location.

Sales and use taxes

Oregon does not impose a sales tax that businesses must collect. The one exception is if you sell automobiles. The tax rate is 0.5% of the retail price. Also, if you sell items online to another state, you may have to collect and pay sales tax.

Remote seller tax considerations

Oregon doesn’t impose a general sales tax, so remote sellers are not required to collect Oregon sales tax on sales to Oregon residents.

However, remote sellers may be subject to Oregon's Corporate Activity Tax (CAT) if they meet certain thresholds:

- Businesses with Oregon commercial activity of $750,000 or more must register for the CAT

- The tax is applied to taxable Oregon commercial activity exceeding $1 million

- The tax is computed as $250 plus 0.57% of taxable Oregon commercial activity over $1 million

For CAT purposes, you have nexus — the connection between a business and a state or local government that requires the business to collect and pay sales tax — with Oregon if:

- Owns or uses capital in Oregon

- Has a certificate from the Secretary of State authorizing it to do business in Oregon

- Has $50,000 of property or payroll in Oregon (including employees and contractors acting on behalf of the business)

- Has $750,000 of Commercial Activity in Oregon

- Has 25% of its property, payroll, or Commercial Activity in Oregon

- Has Oregon domicile

Property taxes

Unless you have a business that's otherwise exempt, you'll be responsible for paying property taxes on any building you own. Your property taxes will be valued at 100% of the real market value, regardless of what you paid for the building. The exact rate you pay will vary by what county your business is in. Visit the Oregon Department of Revenue for more information.

Taxable property typically includes:

- Privately owned real property (land, buildings, and fixed machinery and equipment)

- Manufactured homes

- Personal property used in business