According to recent QuickBooks research, the average US small business is chasing $17,500 in late payments. Without a clear balance sheet example, these "hidden" assets and the debts you owe can easily slip through the cracks.

A balance sheet is an important financial statement that summarizes your business's financial situation and helps you evaluate performance and your ability to meet financial obligations.

This guide will show you what a balance sheet is, how to use it, and how it can help you manage your business finances more effectively. We’ll also provide you with a balance sheet example and template you can use for your own business.

Jump to:

- What is a balance sheet?

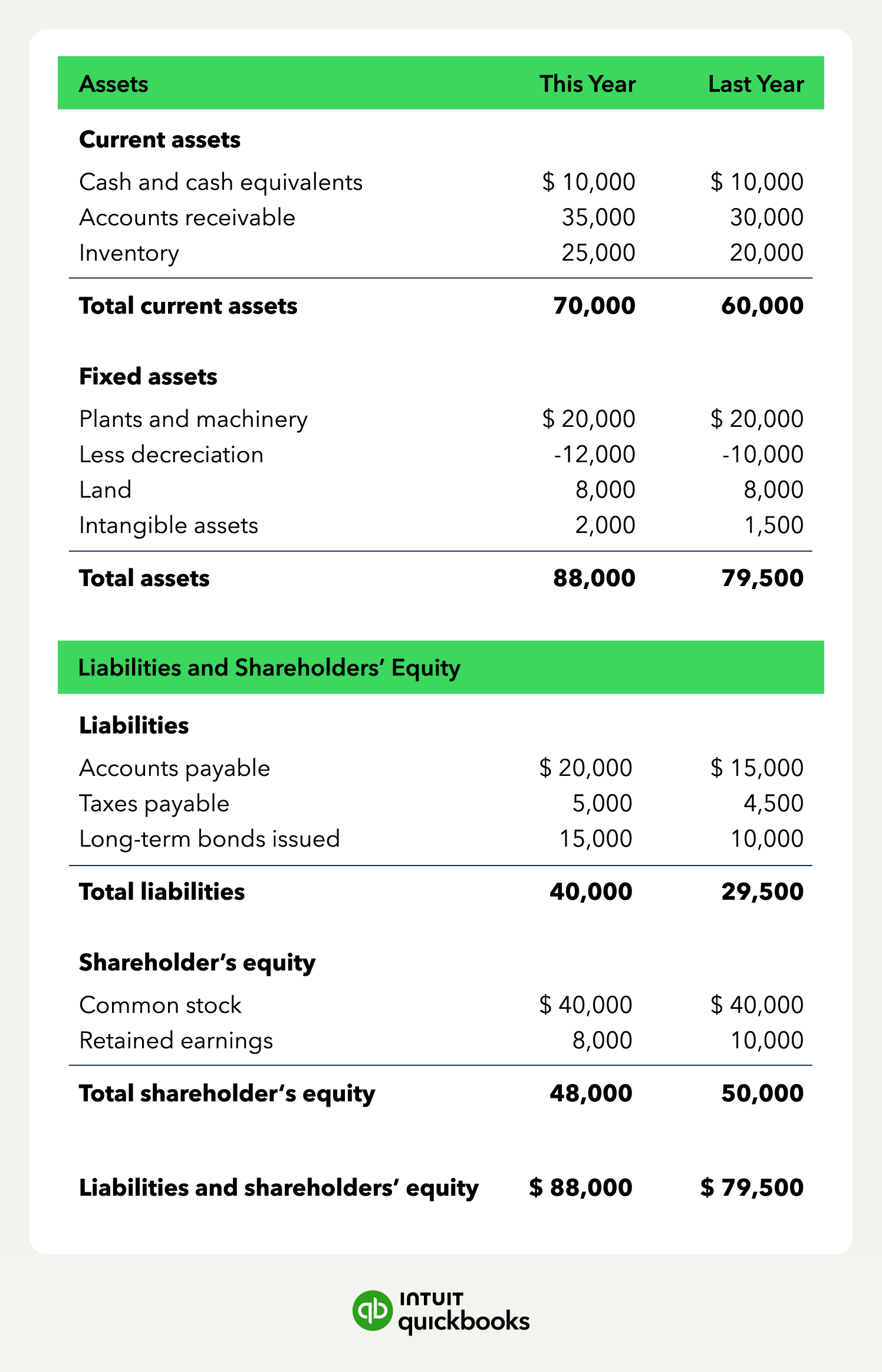

- Balance sheet example

- The 3 key components of a balance sheet

- Balance sheet calculation explanation

- Reading and understanding a balance sheet

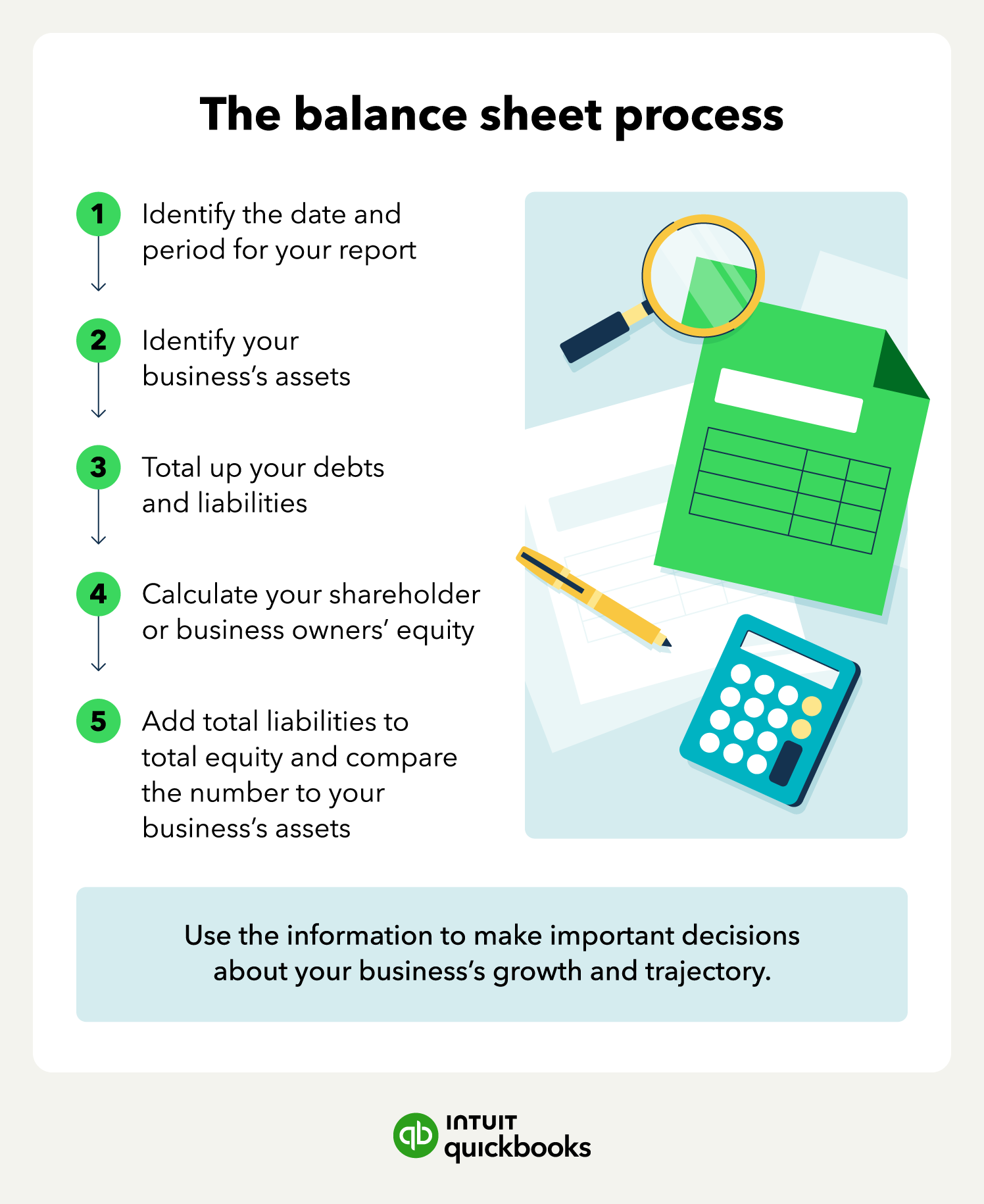

- How to create a balance sheet in 6 steps

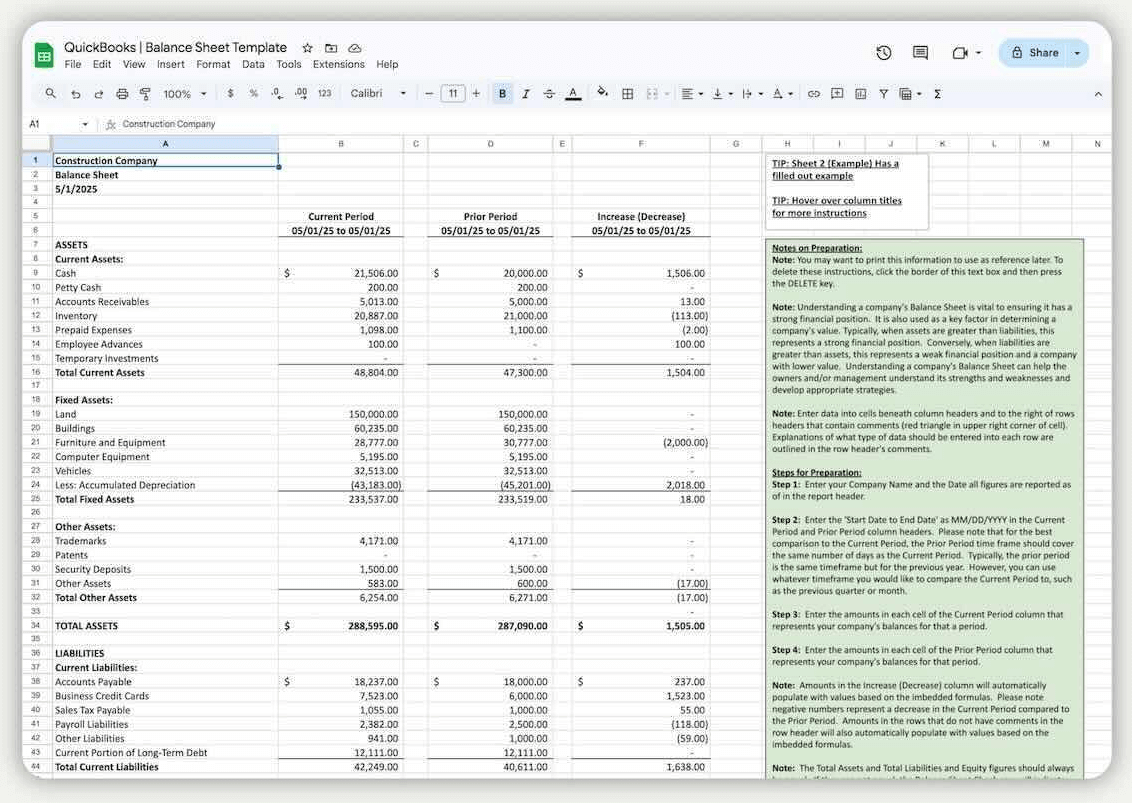

- Balance sheet template

- Balance sheet uses for small businesses

- Spend more time growing your business