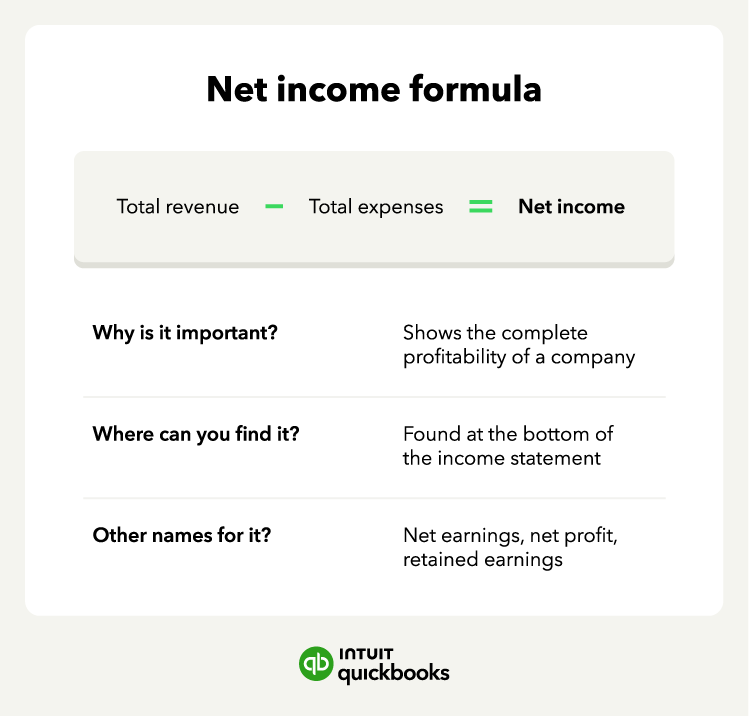

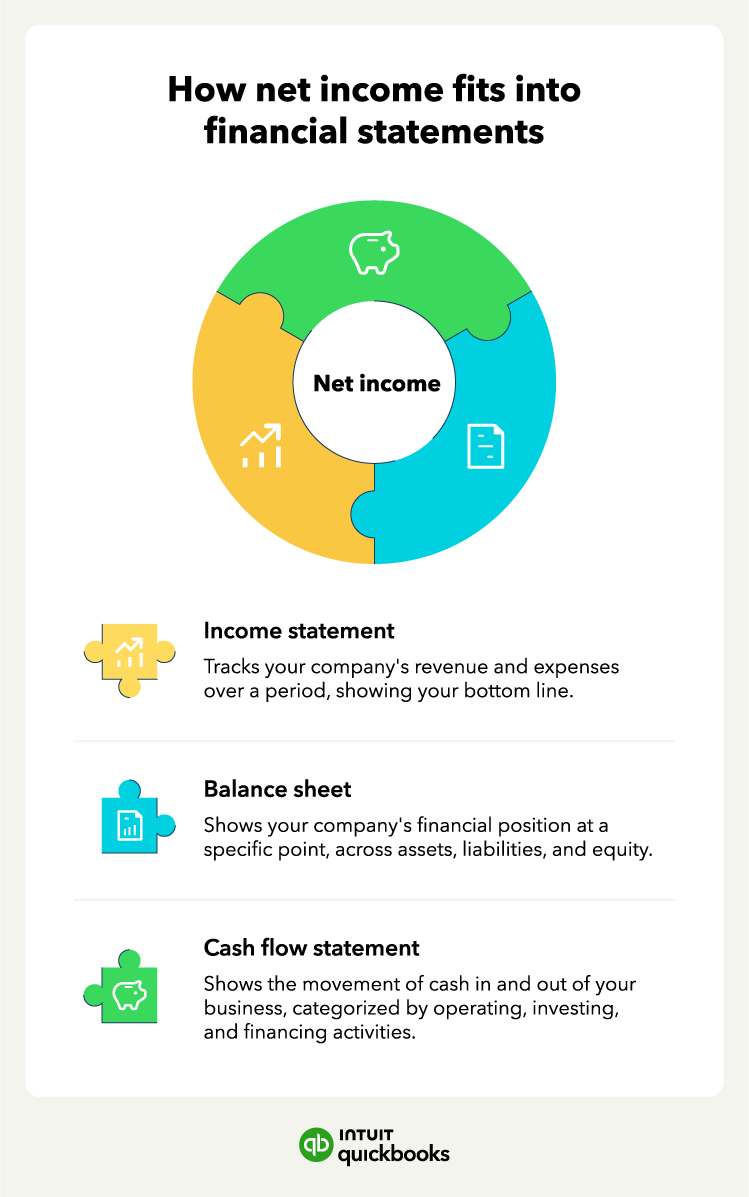

Net income formula tips

When using the net income formula, make sure you keep these tips in mind:

1. Know what counts as total revenue

Total revenue refers to the entire amount of income your business earns from its core operations. This includes sales of products or services, interest income, rental income, or any other business-related earnings.

It’s important not to confuse this term with gross profit, which is total revenue minus the cost of goods sold (COGS).

For example, if you bring in $500,000 in sales and it costs $200,000 to produce your goods (COGS), your gross income is $300,000, but your total revenue stays at $500,000.

2. Make sure you include all expenses

Your total expenses encompass every cost associated with running your business, including:

- COGS (materials, labor, production costs)

- Operating expenses (rent, utilities, salaries, marketing)

- Taxes (federal, state, local business taxes)

- Interest (on business loans or credit lines)

- Depreciation (the reduction in value of assets like equipment or vehicles over time)

- Other miscellaneous expenses (legal fees, office supplies, etc.)

Forgetting any of these can throw off your net income, which might leave you with an unrealistic view of your business’s profits and could impact your tax reporting.

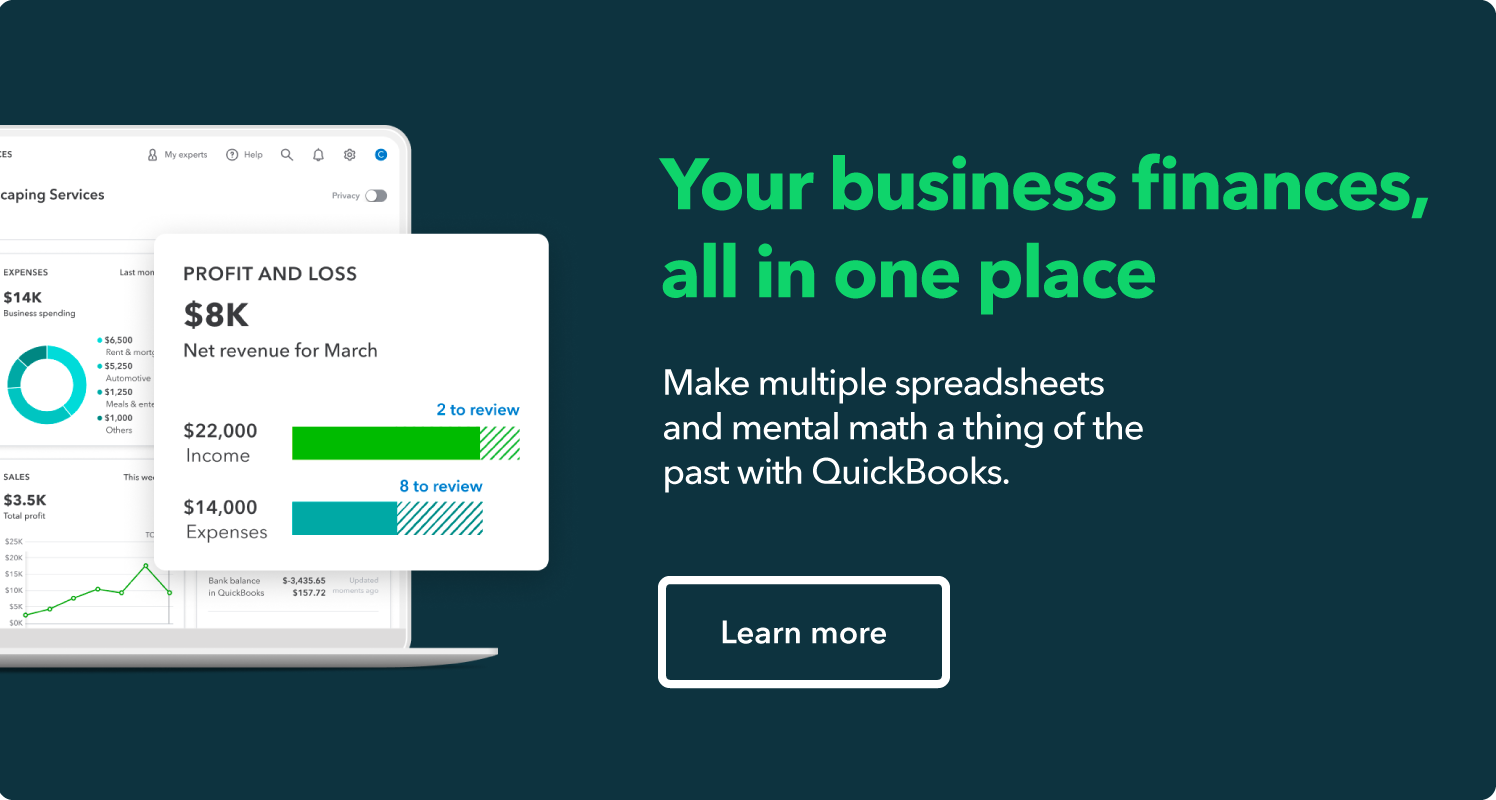

3. Don’t forget about net profit margin

Once you’ve got your net income, you can take it a step further and calculate your net profit margin. This shows what percentage of your revenue turns into profit, and you can do this by dividing your net income by revenue and multiplying it by 100 to get a percentage.

- Net profit margin = (Net income / Total revenue) X 100

For example, if your net income is $50,000 and your total revenue is $200,000, your net profit margin is 25%. That means for every dollar you earn, you’re keeping 25 cents as profit.

4. Make it a habit to check in on your numbers

Your business’s financial health isn’t something you figure out once and forget—it changes over time. That’s why it’s important to regularly review your income statements and see how your net income is trending.

Are profits growing? Are expenses creeping up?

Check in consistently so you can spot patterns, catch potential issues early, and adjust your strategy before small problems become big ones.