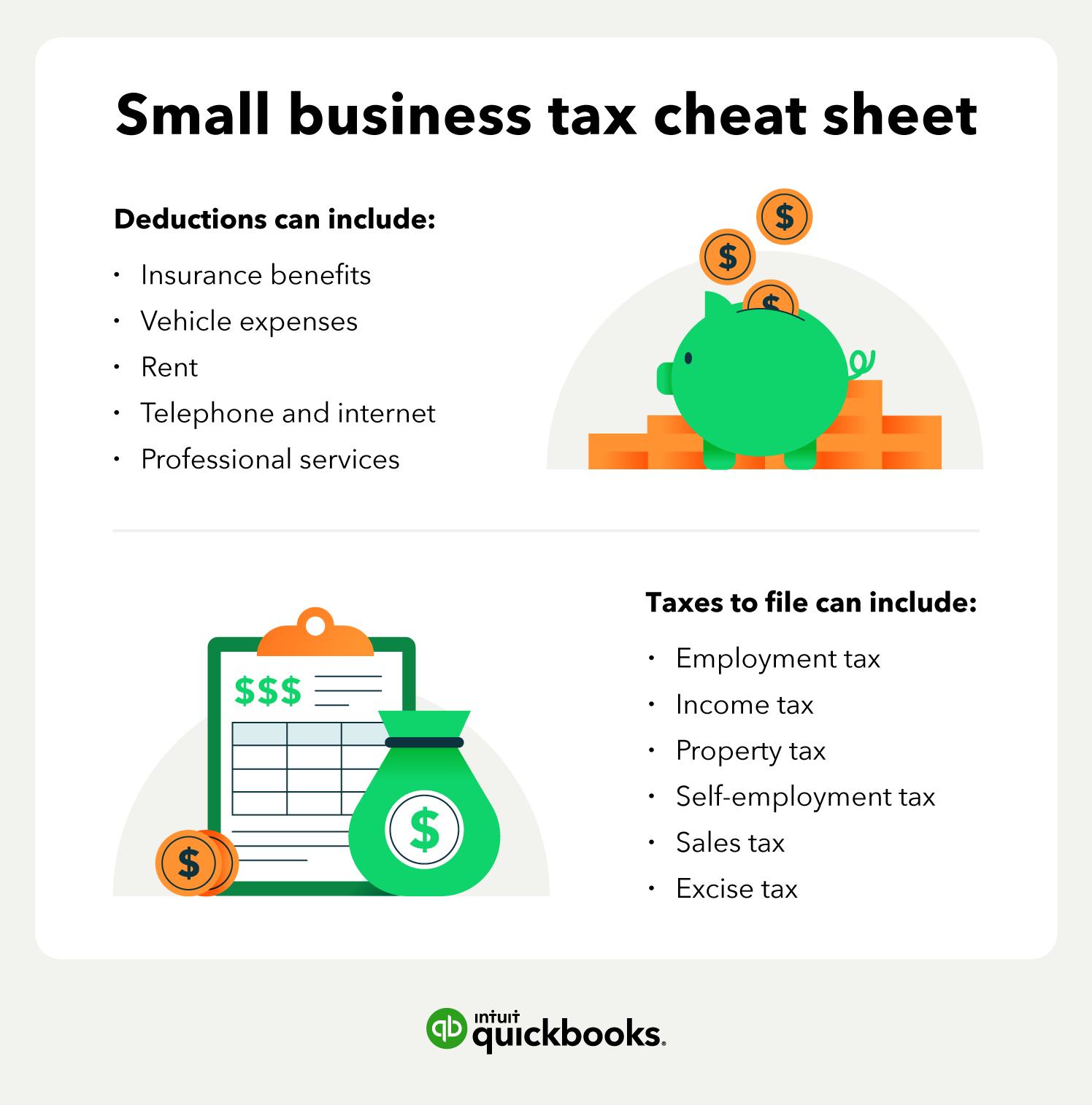

Types of business taxes in Illinois

As an employer in Illinois, you may be responsible for reporting and paying other business taxes in addition to withholding payroll taxes from your employees' paychecks. In order to have a fair workplace and stay in compliance, your business must adhere to the pay equity laws in Illinois. From federal to state and local levels, understanding the different tax programs and their impact on your business’s finances is important.

Federal taxes

You'll be responsible for federal taxes in whatever state you open a business in. Unfortunately, there are dozens of federal tax forms with unique due dates and requirements. Using an accountant or small business accounting software can be helpful in avoiding mistakes that can lead to overpayment or penalties.

As a business owner, you have both personal and business tax filing obligations. Here’s what you need to know:

Personal tax filing

Federal income tax returns:

Every individual is required to file and pay federal personal income tax. This forms the foundation of your overall tax responsibility.

Business tax filing

Business owners have additional filing requirements, depending on the business structure:

- Sole proprietorship: Income and expenses are reported on your personal tax return using Schedule C (Form 1040).

- Partnership: A partnership must file an information return (Form 1065) to report income, deductions, and other relevant details, while each partner reports their share of income on their personal return.

- Corporation: A corporation files a corporate tax return (Form 1120), paying taxes on its profits.

- S Corporation: An S corporation files an informational return (Form 1120S). Its income, losses, and deductions pass through to shareholders, who report them on their personal returns.

- Limited Liability Companies (LLCs): LLCs are not classified separately for federal tax purposes and are taxed based on their ownership structure. Single-member LLCs default to sole proprietorship taxation or may elect corporate taxation, while multi-member LLCs default to partnership taxation or may elect corporate taxation.

Self-employment tax

If you work for yourself and earn more than $400 a year, you pay toward Social Security and Medicare programs through a self-employment tax. The Social Security system provides retirement benefits, disability benefits, survivor benefits, and hospital insurance (Medicare) benefits.

Employment taxes

As an employer, you are responsible for withholding and depositing federal income tax and the employee contribution to Social Security and Medicare taxes. You must also pay the employer portion of Medicare and Social Security and pay federal unemployment tax (FUTA), and must also follow the SUTA tax requirements in Illinois.

State taxes

As a business owner, understanding your state tax obligations is an integral part of running your organization.

Illinois corporate tax rate

In Illinois, corporations pay a corporate income tax based on their net income.

What is the corporate tax rate?

Illinois has a 9.5 percent corporate income tax rate. This consists of a 7% business income tax rate and a 2.5% Personal Property Replacement Tax (PPRT) for corporations.

Personal Property Replacement Tax (PPRT)

The Personal Property Replacement Tax, also commonly known as just replacement tax, is designed to replace revenue that local governments lost when the state eliminated the personal property tax on businesses in 1979. This tax provides funding for local entities, including counties, municipalities, school districts, and special districts, ensuring they continue to receive financial support for public services.

The PPRT is levied on businesses, including corporations, partnerships, and trusts, and is calculated as a percentage of their net income. The rates vary depending on the type of business entity:

- Corporations: 2.5% of net income.

- Partnerships, S Corporations, and Trusts: 1.5% of net income.

How are the corporate tax rate and the PPRT calculated?

In Illinois, corporate taxes are calculated beginning with the corporation's federal taxable income. This amount is adjusted to determine the Illinois base income by adding back items like state and municipal interest income and subtracting others, such as interest income from U.S. Treasury obligations.

The corporate income tax rate of 7% is applied to this base income. The 2.5% Personal Property Replacement Tax (PPRT) is also calculated based on net income.

S corporations and partnerships are subject to a lower PPRT rate of 1.5% on net income and are exempt from the 7% corporate income tax.

Who may be liable for the corporate income tax?

Corporations are subject to Illinois corporate income tax if they have a nexus with the state. Nexus is established if:

- The corporation is qualified to do business in Illinois.

- The corporation is required to file a federal income tax return.

- The corporation has a physical presence in Illinois.

A corporation may be liable for Illinois corporate income tax if its activities in the state go beyond simply soliciting orders for tangible personal property. Out-of-state businesses are generally protected from state income tax if their only activity in Illinois is requesting orders that are approved and fulfilled outside the state. However, if a corporation conducts additional business activities within Illinois, it may lose this protection and become subject to the state's income tax.

Franchise taxes in Illinois

Franchise tax, also known as privilege tax, is a tax levied on businesses throughout the state that rewards them the privilege of conducting business operations within the state's borders.

What is the franchise tax rate?

The franchise tax rate, also known as a capital stock tax, is 0.10% of a business's total paid-in capital for corporations. Paid-in capital is the total money a business receives from its shareholders for their stocks. If your corporation doesn't have any paid-in capital, it still must pay a minimum franchise fee of $25.00 annually. The cap for annual franchise tax is $1 million. When submitting your franchise tax alongside your corporation annual report, you'll need to pay a $75.00 filing fee. There are plans to phase out this tax, but as of now it remains in effect.

Illinois franchise tax credits

For tax years ending on or after January 1, 2024, and before January 1, 2025, the first $5,000 in liability is exempt from the franchise tax payable by domestic corporations. On and after January 1, 2025, the first $10,000 in liability is exempt from the franchise tax payable by domestic corporations.

Pass-through entity (PTE) tax

The PTE tax is an elective tax that applies to partnerships and S corporations. This tax rate is 4.95% of the taxpayer's net income. It's important to note that LLCs may elect to be taxed as partnerships or S corporations, making them eligible for the PTE tax election.

Partners or shareholders of an electing pass-through entity can claim a credit against their individual tax liability equal to 4.95% of their distributive share of the entity's net income.

Excise tax

An excise tax is charged on specific goods, activities, and services designated by the state. The rate for each service, activity, or good varies and can be found in the Illinois Revenue's Excise Tax Rates and Fees table. Some examples of excise taxes in Illinois include:

- Alcoholic beverages: Different types of alcoholic beverages are taxed at varying rates. For instance, beer and cider (0.5% - 7% alcohol) are taxed at $0.231 per gallon and alcoholic liquor (with alcohol content of less than 20%) is taxed at $1.39 per gallon.

- Tobacco products: The excise tax for distributors and individuals is $2.98 per package of 20 cigarettes.

- Gas use tax: Purchasers are charged 5 percent of the purchase price or $0.024 per therm, whichever is less. Delivering suppliers are charged $0.024 per therm.

- Cannabis: There is a 10% tax on adult-use cannabis with THC levels of 35% or less; 25% tax on adult-use cannabis with THC levels above 35%.

Unemployment tax

In Illinois, employers are required to pay state unemployment insurance (UI) taxes, which fund temporary benefits for eligible unemployed workers.

For the year 2025, the taxable wage base is set at $13,916, meaning employers pay UI taxes on each employee's wages up to this amount. The tax rate for each employer ranges from 0.2% to 6.4% and is based on the employer’s history with unemployment claims and a fixed fund building rate of 0.55% applied to all employers to maintain the solvency of the Unemployment Insurance Trust Fund. Combining these components, the total UI tax rate for employers in 2025 ranges from 0.75% to 7.85%.

Local taxes

In addition to state taxes, Illinois allows local jurisdictions to impose their own taxes, which can affect businesses operating within those areas.

Sales and use taxes

In Illinois, the state sales tax rate for general merchandise is 6.25%, while most groceries, medical appliances, and prescription drugs are taxed at a reduced rate of 1%. Local and county tax rates vary significantly, with a combined maximum sales tax rate of 11.5% across the state. In Chicago, the total combined rate is 10.25%.

As of January 1, 2025, some localities have updated their sales tax rates for general merchandise. Businesses can check the current combined state and local tax rates for specific areas using the MyTax Illinois Tax Rate Finder.

Illinois sales tax is a combination of use taxes and Retailers' Occupation Tax (ROT) applied to the total gross receipts of retailers from the sale of tangible personal property intended for consumption or use.

Remote seller tax considerations

In Illinois, remote sellers—businesses without a physical presence in the state—are required to collect and remit Illinois Retailers' Occupation Tax (ROT) if they have an economic nexus in the state. Effective January 1, 2025, a remote seller must register for an Illinois Tax ID Number and begin collecting ROT if:

- The remote seller's cumulative gross receipts from sales of tangible personal property to purchasers in Illinois are $100,000 or more; or

- The remote seller enters into 200 or more separate transactions for sales of tangible personal property to purchasers in Illinois.

Remote sellers meeting these thresholds should register and start collecting Illinois ROT beginning January 1 of the following year. For detailed information, refer to the Illinois Department of Revenue's website.

Property taxes

In Illinois, property taxes are managed primarily at the local level and are a key source of funding for services such as education, public safety, and local infrastructure. Tax rates differ by county and municipality, based on the budgetary requirements of each area. Property assessments are typically conducted every four years, with annual updates made between general assessment periods.