You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Are paper checks slowing down your small business payments? eChecks, or electronic checks, are a secure digital alternative to paper checks for fast and cost-effective fund transfers.

These payment methods offer enhanced security and significantly lower fees, making them ideal for recurring payments and high-cost items. For a small business, that time (and money) matters.

According to QuickBooks' 2025 Small Business Late Payments Report, over half (56%) of the surveyed small businesses reported being owed money from unpaid invoices, averaging $17.5K per business. Late payments can significantly impact cash flow and overall business health.

Today, we'll cover how eChecks work, why they matter, and how you can use them to speed up payments in your small business.

`

If you're looking to streamline your small business payments, you need to understand the basics of the eCheck. This payment solution provides a secure, cost-effective, *and* efficient alternative to traditional, paper-based transactions.

Let's break down the essential concepts so you can put this tool to work for your bottom line.

An ACH Payment is a broad term for any electronic transaction processed through the Automated Clearing House (ACH), a US-based electronic fund transfer system. In simple terms, this system is a centralized method that banks use to transfer money without relying on paper checks or card networks.

For your small business, understanding this means realizing that when you accept an eCheck, you're using a highly regulated and reliable system for funds transfer.

eChecks are incredibly versatile, but they really shine when it comes to guaranteeing a predictable income stream. They're commonly used for online purchases, bill payments, and recurring payments, as they are reliable and convenient.

Example: If you run a gym, you can use eChecks to set up automatic, monthly membership fee deductions directly from your customers' checking accounts, reducing late payments and saving you time on collections.

eCheck payments are a safe alternative to paper checks, which can be vulnerable to fraud. eChecks reduce the risk by using data encryption and eliminating the need to handle sensitive bank information physically.

Example: When a customer pays an invoice for your consulting services via a secure online form with an eCheck, their bank details are encrypted. This is much safer for you than accepting a paper check with their routing and account numbers sitting in your office for anyone to see.

It's important to know that eChecks cannot be processed on weekends. The transaction must be processed through the ACH network during regular business hours (typically 3-6 days), so a payment can take a few days to clear.

Example: If a customer pays you for catering services on a Friday, the funds won't start moving until Monday and won't be fully available until later that week. You need to account for this in your cash flow projections and payment terms.

In 2026, the gap between eChecks and wire transfers is closing. While a standard eCheck processes in batches over 3-6 days, many processors now offer same-day ACH or integration with FedNow and RTP (Real-Time Payments).

Why it matters: You can now choose between standard (lowest cost) and instant (higher fee, immediate settlement), depending on your specific cash flow needs for that day.

An eCheck can be declined for various reasons, such as insufficient funds or incorrect account information. Once the recipient's bank has processed a payment, it generally cannot be canceled.

Example: If a new client for your landscaping service provides incorrect bank details, their eCheck will be declined. You’ll then have to follow up and obtain the correct information, as the initial transaction isn’t easy to reverse or correct once submitted.

Most people with a bank account can use eChecks. However, it's always a good idea to check with your bank or payment processor for any specific requirements or restrictions before initiating a transaction. By accepting eChecks, you expand the pool of customers who can pay you easily and conveniently.

Example: Offering eChecks as an option alongside credit cards and digital wallets ensures that customers who prefer or only use direct bank debits—like many corporate clients—can still pay you without friction.

eChecks offer a convenient way for merchants and customers, employers and employees, and small businesses to exchange money electronically. How this works:

eCheck transactions rely on the Automated Clearing House (ACH) system, which facilitates batches of electronic funds transfers (EFTs). ACH allows banks to exchange transaction details, communicating what to debit, what to credit, and to whom—all electronically.

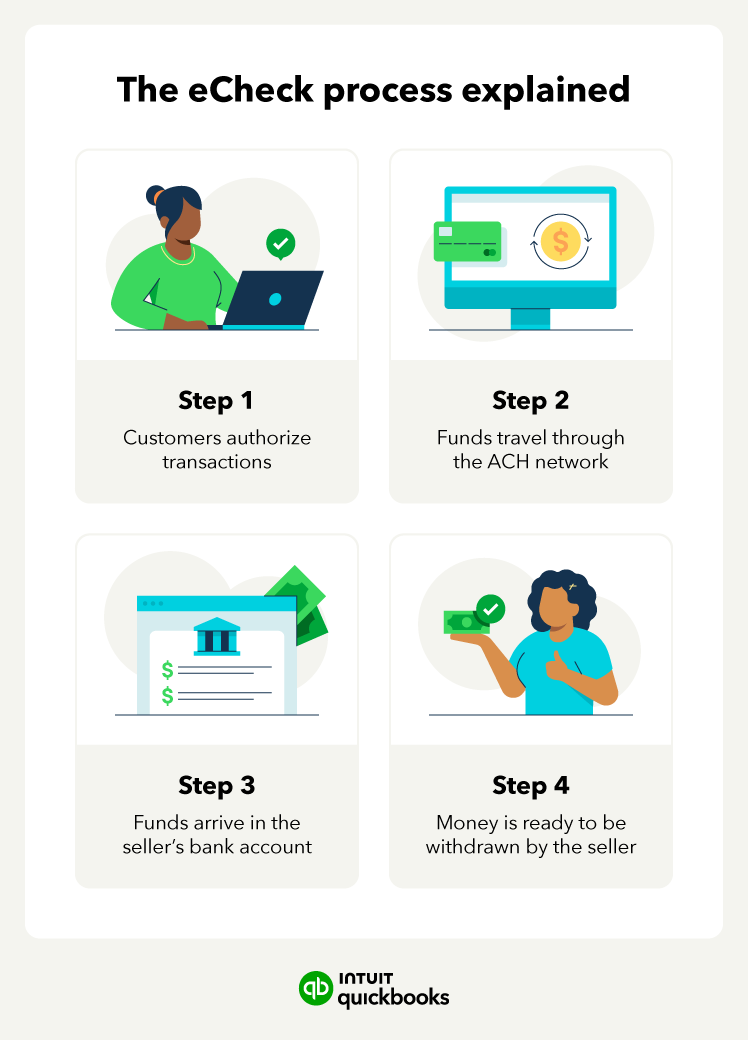

Let’s take a closer look at how eCheck processing works step by step.

The customer authorizes a predetermined amount to be withdrawn from their account. You can’t receive funds until the customer approves the transaction. Ensure your banking details are correct to avoid delays in processing.

The funds are transferred electronically via the ACH network. Keep in mind that an ACH transfer is slower than a wire transfer. ACH transfers are processed in batches rather than one by one, so it can take a few days to see the money move.

The amount is transferred from the payer’s financial institution to the seller’s financial institution. Processing times may vary, but eChecks typically take 24 to 48 hours to verify and 3 to 6 business days for funds to be deposited into the respective business checking account.

The money is withdrawn from the payer’s bank account and deposited into the payee’s bank account. Your small business bank account should now reflect the funds, and you can withdraw them.

On average, an eCheck takes three to six business days to process through the ACH network. However, several factors can impact processing times.

For example, some banks may have longer internal review times for eCheck transactions, which can extend the processing window. Also, if you’re sending an eCheck payment to your business account for the first time, processing may take longer due to additional security checks or account verifications.

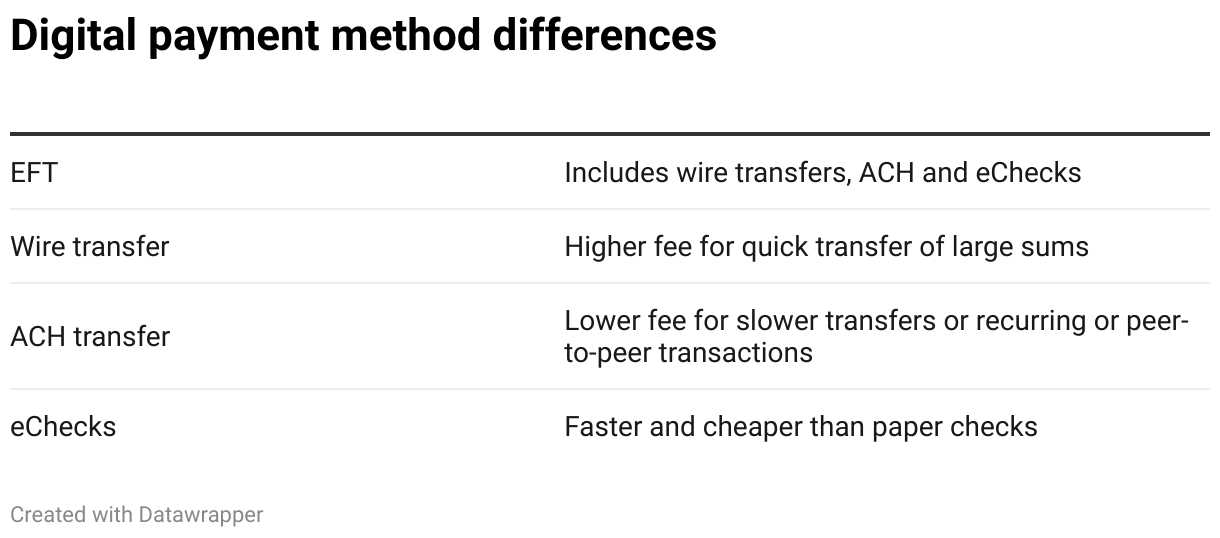

Electronic Funds Transfer (EFT) is a broad term that covers any type of electronic payment method. Wire transfers, ACH transfers, and eChecks are all examples of EFTs, but each has different features and benefits. Let’s take a look at how eChecks differ from these payment methods.

Automated Clearing House (ACH) is a network that processes batches of electronic transactions. ACH transfers can be used for recurring payments, such as payroll or bills, or for one-time payments, such as online shopping or peer-to-peer transfers. ACH transfers typically take one to three business days to process, but they also tend to be cheaper and more convenient.

eChecks are a type of ACH transfer that mimics the process of writing a paper check. eChecks require the payer to provide their bank account number and routing number, and the payee must authorize the payment.

They’re safer than paper checks, as they reduce the risk of fraud and bounced checks. eChecks are also faster and cheaper than paper checks, as they eliminate the need for printing and mailing.

eChecks remain the most effective way to avoid the 3%–4% interchange fees associated with premium credit cards.

Wire transfers send money directly from one bank to another, usually within the same day, making them much faster than eChecks. However, wire transfers cost more and are commonly used for time-sensitive or large payments, like buying a home.

On the other hand, eChecks are slower and processed through the ACH system, but they’re cheaper and safer for everyday transactions.

To accept eCheck payments as a business, you need a payment processor that supports this method and a secure online form that collects the customer's bank information.

If you decide to use eChecks as a payment option, follow these steps:

Your first step is to protect yourself and your customers. Don't just pick the cheapest provider; choose a reputable tool like QuickBooks Payments that explicitly supports ACH/eCheck transactions and utilizes robust data encryption.

Look for the following when choosing a provider:

You’ll need your customer to approve this transaction before you can access the funds. Unlike simply swiping a card, the ACH network requires explicit permission.

To approve an eCheck, you'll need:

Before you begin accepting eCheck payments, you’ll need to gather and submit key information to the ACH merchant.

You'll need to provide:

As with any form of payment, merchants and customers are encouraged to protect their payment information. Notify your ACH provider if you need to change this information or suspect any fraudulent activity.

Once you’ve set up your account, received customer authorization, and entered your payment details, you’re ready to process the payment and access your funds. Keep in mind that the process can take a few days to complete.

Since eChecks are a form of EFT that enables you to easily collect recurring payments, process payroll, and initiate online payments, prepare to enjoy a more streamlined payment process.

If you accept an eCheck payment from a customer for the first time, the processing may take slightly longer than usual (sometimes 5-7 days). This is due to additional security checks or account verification performed by the banks.

The days of asking customers to hunt for a checkbook to find a routing number are over. Modern workflows use Instant Account Verification (IAV).

eCheck transactions can be useful for recurring payments and direct deposit, but several other perks may benefit your business.

If your business frequently processes paper checks or has recurring customer transactions, eChecks can save you time. Your customers will benefit from having easier ways to pay, and you’ll reduce the risks of human error during payment processing. eChecks also provide a digital transaction log that feeds data to your accounting system, making reconciliation simple.

eChecks are generally a reliable way of transferring funds. They use the ACH network to process transactions. The ACH system is governed by the Federal Reserve as well as the National Automated Clearing House Association, which upholds strict regulatory guidelines for participating banks and providers.

eChecks pass through far fewer hands than paper checks, which speeds up the transaction process and mitigates fraud risk (more on that in a moment). If your business collects recurring customer payments, eChecks can be a more consistent payment method than credit cards.

Another big benefit eChecks offer merchants and other small businesses is their cost-effectiveness. Processing fees for eChecks are typically more affordable than other payment methods, like credit cards, which can range between 1.5% and 4% of each transaction.

And if you use QuickBooks Bill Pay, standard ACH payments are now free ** — meaning you can pay vendors electronically with no per-transaction fee, keeping more money in your business.

eChecks are generally considered a safe, reliable payment option for both merchants and customers. On the customer’s side, eChecks leverage data encryption to protect sensitive details like bank routing information and account numbers. In addition, eChecks exchange fewer hands than sending or cashing a check.

As for the merchant, data encryption works in your favor, too. To mitigate the risk of receiving a bad check, it’s a good idea to research payment processors and ensure you’re only working with reputable providers.

Carbon footprint reporting is more than a trend; it’s often a requirement for mid-market contracts. Switching from paper checks to eChecks is a measurable way to reduce your business's environmental impact by eliminating the paper, ink, and fuel used in physical mail delivery.

Like any payment option, eChecks have both advantages and disadvantages. Now that you’ve had a chance to look through the positive aspects, let’s review some of the potential drawbacks.

As we covered earlier in this post, it typically takes between a few business days for eChecks to process fully. Other payment types, such as debit and credit card payments, are usually posted within one to three days. For some businesses, payment timelines are more flexible, while others may require greater efficiency in collections.

Most customers are familiar with debit and credit card transactions that use the ACH network, but fewer are familiar with eChecks. Transitioning to eChecks may be challenging depending on your customer base, but it could also help expand your possibilities for doing business.

As digital fraud has become more sophisticated, banks in 2026 have stricter know-your-customer (KYC) requirements.

The challenge: Setting up an eCheck merchant account may require more upfront documentation than a simple PayPal account.

The fix: Use a provider that bundles your identity verification with your existing accounting software to skip the redundant paperwork.

If your business is thinking about accepting eChecks, there are a few bumps you might hit along the way. Let’s look at some of the most common challenges and how you can address them.

If a customer doesn’t have enough money in their account, the eCheck can bounce. This means you won’t receive payment, which may also result in additional fees. To avoid this problem, confirm the customer’s bank details before processing the payment. You can even use pre-authorization to ensure they have the necessary funds before you proceed.

Example: If you are a property manager collecting a monthly rent payment, instead of submitting the full amount immediately, your payment system could perform a small pre-authorization check (like a $1 debit) a few days before the official payment date.

If the pre-authorization fails, you then know to contact the tenant before incurring fees for the full returned payment.

Entering the wrong account or routing number can lead to failed payments and cause frustrating delays for both you and your customers. Before submitting an eCheck, have your customers double-check these details. Offering a simple step in your payment form where customers can verify their information helps catch errors before they cause problems.

Example: When onboarding a new client for a recurring consulting retainer, your online payment form should require them to enter their bank account number twice to ensure accuracy. The system can then instantly flag a mismatch, preventing a transaction failure that would otherwise delay your first payment by a week.

Although eChecks are generally more secure than paper checks, there’s still a risk of fraud because scams like account hijacking or using stolen bank details can still happen. To mitigate this risk, ensure the payer or payee is legitimate, be cautious of any unsolicited payments, and always use trusted payment platforms with robust security features.

Example: You receive a large, unsolicited eCheck payment for services you haven't rendered. If you didn't initiate an invoice, contact the payer directly to confirm the transaction's legitimacy before processing any refund.

Like credit card payments, eCheck transactions can be disputed, resulting in chargebacks or returns. Be sure to keep thorough records of your transactions, and let your customers know your refund and dispute policies upfront.

Example: A customer disputes an eCheck payment for custom furniture. To successfully fight the chargeback, you must provide the payment processor with:

These records prove the transaction was legitimate and the service was delivered.

2026 platforms use machine learning to predict the likelihood of return (non-sufficient funds) before you even hit submit, saving you from bounced check fees.

As more businesses move to recurring eCheck models, customers are becoming increasingly sensitive to surprise bank debits. If a customer doesn't recognize a charge or forgets a renewal date, they may initiate a dispute or move funds, leading to a failed payment and strained client relationships.

To mitigate this, prioritize transparency by setting up automated pre-debit notifications and providing easy-to-access cancellation portals.

Example: You run a monthly SaaS subscription or a recurring landscaping service. Your system sends an automated text or email three days before the eCheck is scheduled to process. This gives the customer a window to fund their account or reach out with questions. It also significantly reduces the likelihood of unauthorized chargebacks or insufficient funds (NSF) returns.

Managing eChecks used to be a manual wait-and-see game. Today, the QuickBooks Payments AI agent proactively secures your cash flow by handling the heavy lifting:

Predictive NSF intelligence: Your AI agent constantly monitors historical payment patterns. It alerts you if a recurring eCheck is at risk of failing due to insufficient funds, giving you the foresight to pause the service before a bounce occurs.

Smart payment recovery agent: If a payment does not go through, the AI does not just stop. It intelligently schedules retries on optimal dates, such as common paydays, to maximize recovery chances without you ever having to send a manual follow-up.

Tailored acceleration strategies: Beyond just processing, the AI agent analyzes your customer data to suggest specific ways to get paid faster. It might recommend turning on certain payment methods for specific clients or drafting personalized reminders to ensure your invoices stay at the top of their list.

Automated done-for-you reconciliation: The AI agent identifies incoming eCheck deposits and instantly matches them to the correct open invoices. It learns your categorization habits to keep your books zeroed out in real-time, completely hands-free.

Ultimately, selecting the right payment tools means minimizing costs, maximizing security, and simplifying your workflow. By integrating eCheck capabilities into your business processes, your business can achieve predictable revenue *without* incurring high credit card fees.

QuickBooks Payments brings it all together—automatically matching transactions, consolidating eChecks, cards, and wallets, and keeping your books clean.

And with the new Payments AI Agent, you can get instant insights into your payment activity, resolve issues faster, and ensure every transaction is accounted for. Start accepting eCheck payments easily to improve your business banking processes and reduce manual accounting effort.

*Get paid 4 days faster on average when you send invoice reminders with Payments AI: Based on U.S. Intuit Assist customers using outstanding invoice notifications and AI-drafted invoice reminder features, compared to customers sending standard invoice reminders to the same customers, from March 2025 to March 2026.

** Limits may apply on total number and amount of payments

Call Sales: 1-800-285-4854