Out-of-state

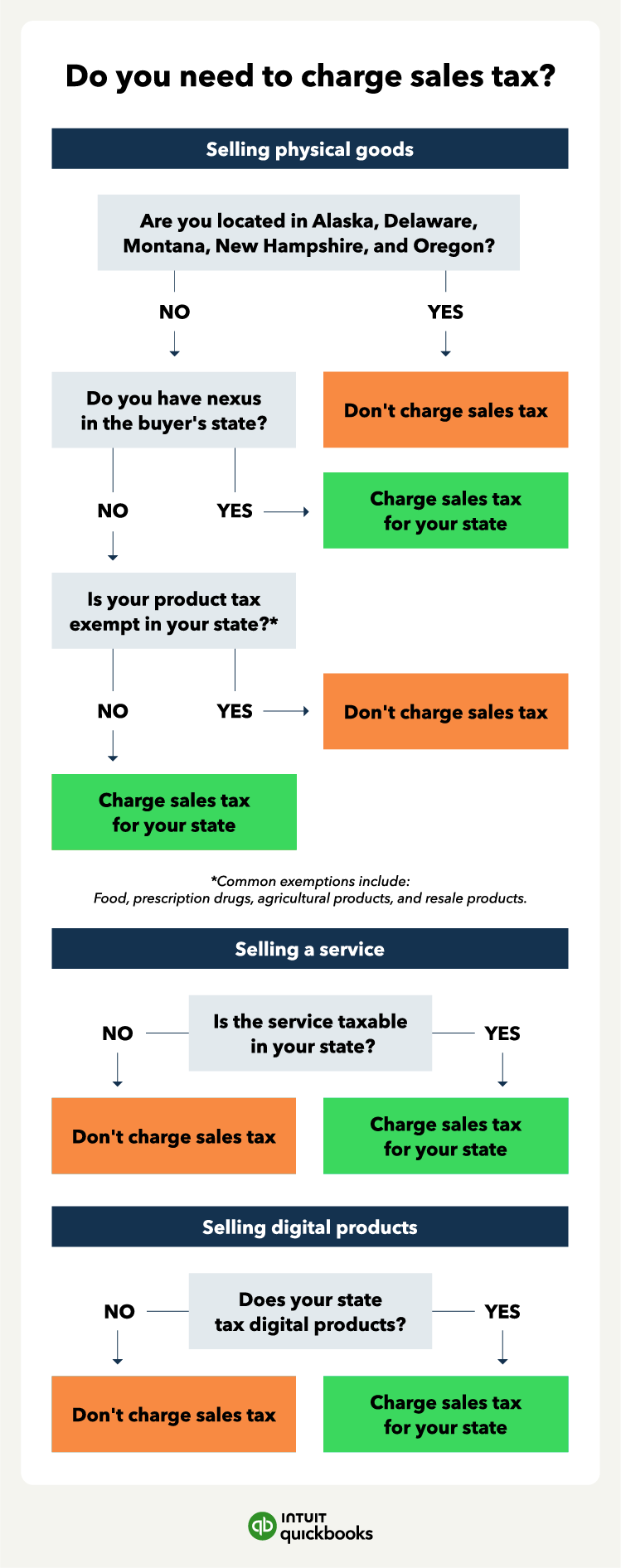

Out-of-state sellers, also called remote sellers, generally won’t need to collect taxes from their customers unless they have a nexus within that state. Literally translated as a “connection,” a nexus means that your business meets one or more of the following criteria:

- Your business has a physical location in that state

- Some of your employees reside in and work in that state

- Your business has property (including intangible property like trademarks, copyrights, and patents) in that state

- Your employees regularly seek or perform business in that state (for example, you have an active salesperson in that state)

So, many online sellers can ship goods out of state without charging or collecting sales tax, provided they don’t have a physical presence in that state.

However, a number of states have enacted nexus laws that require payment of sales tax when sales to that state from an out-of-state buyer exceed a specific dollar threshold or number of transactions.

There’s one more term you might come across as you research your state tax rates. Use tax is a type of excise tax imposed on the sale of specific goods or services or certain uses.

Use tax is often used for out-of-state purchases but is generally not the seller’s responsibility. In most cases, the purchaser should declare and file this tax in their home state.