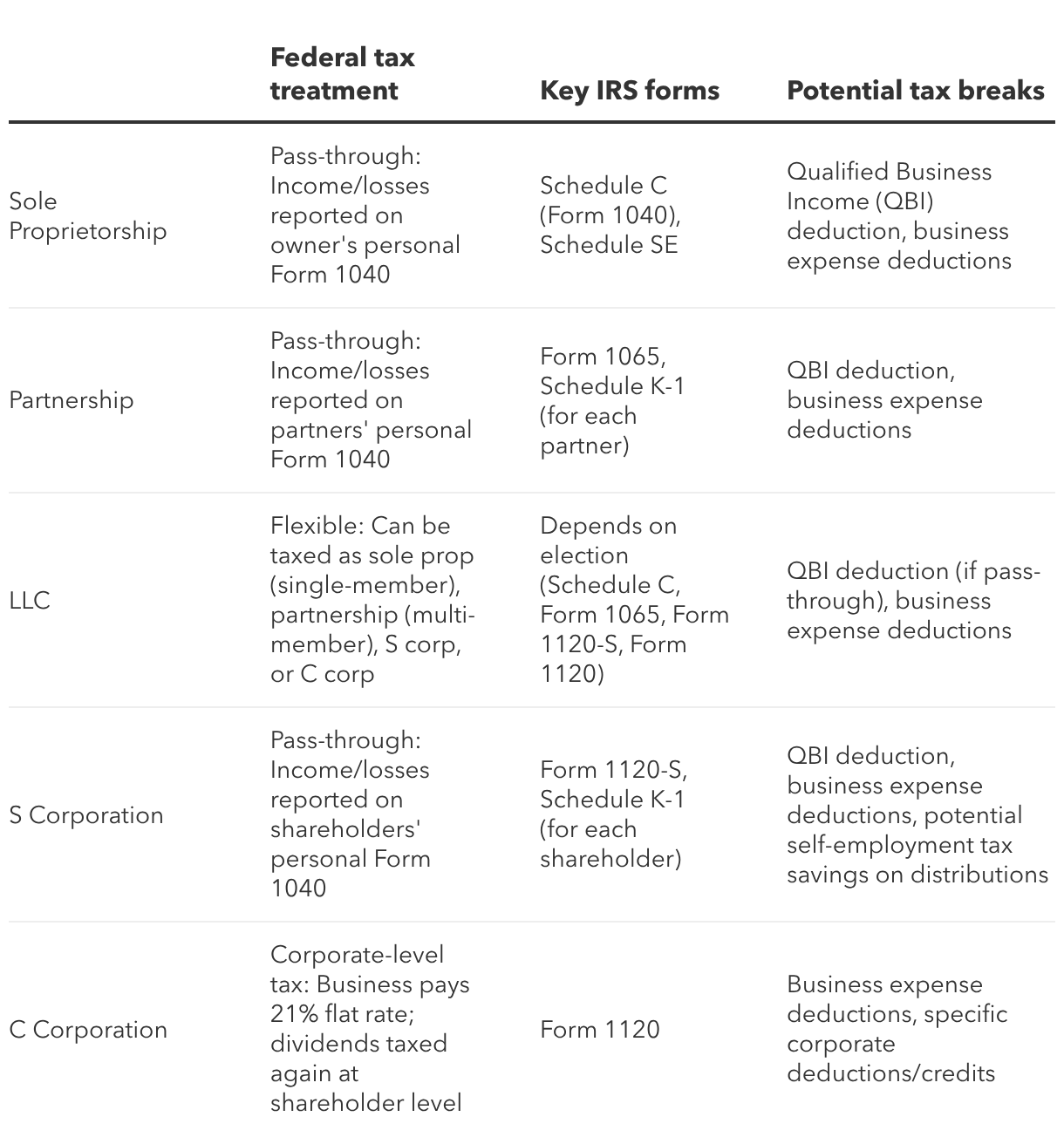

Sole proprietorship

As a sole proprietor, you and your business operate as the same entity for tax purposes. This structure offers the most straightforward setup.

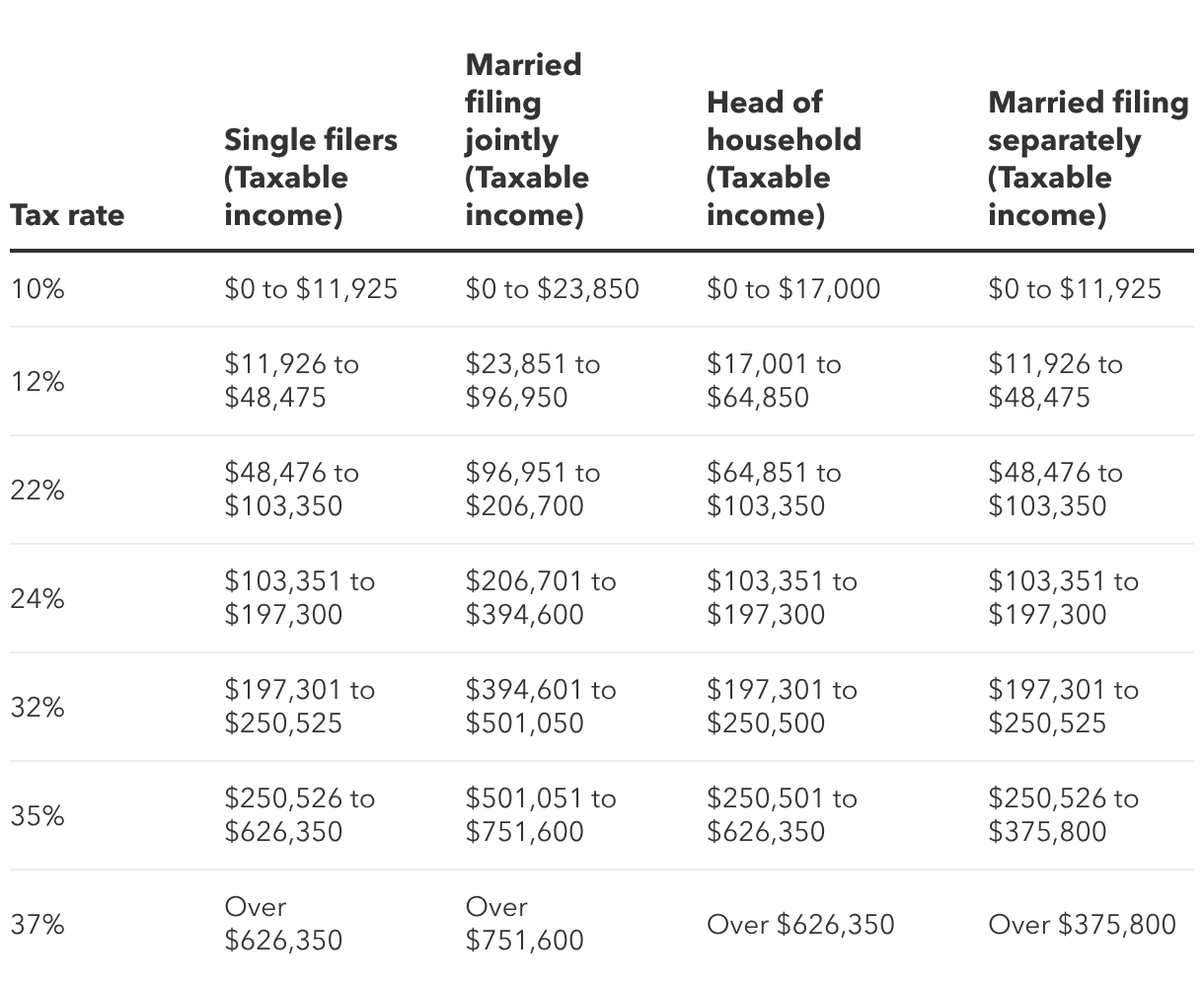

Taxation: Your business income and expenses report directly on Schedule C Profit or Loss from Business (and Schedule SE if you're self-employed) of your personal federal income tax return (Form 1040). Your net profit then becomes subject to your individual income tax rate.

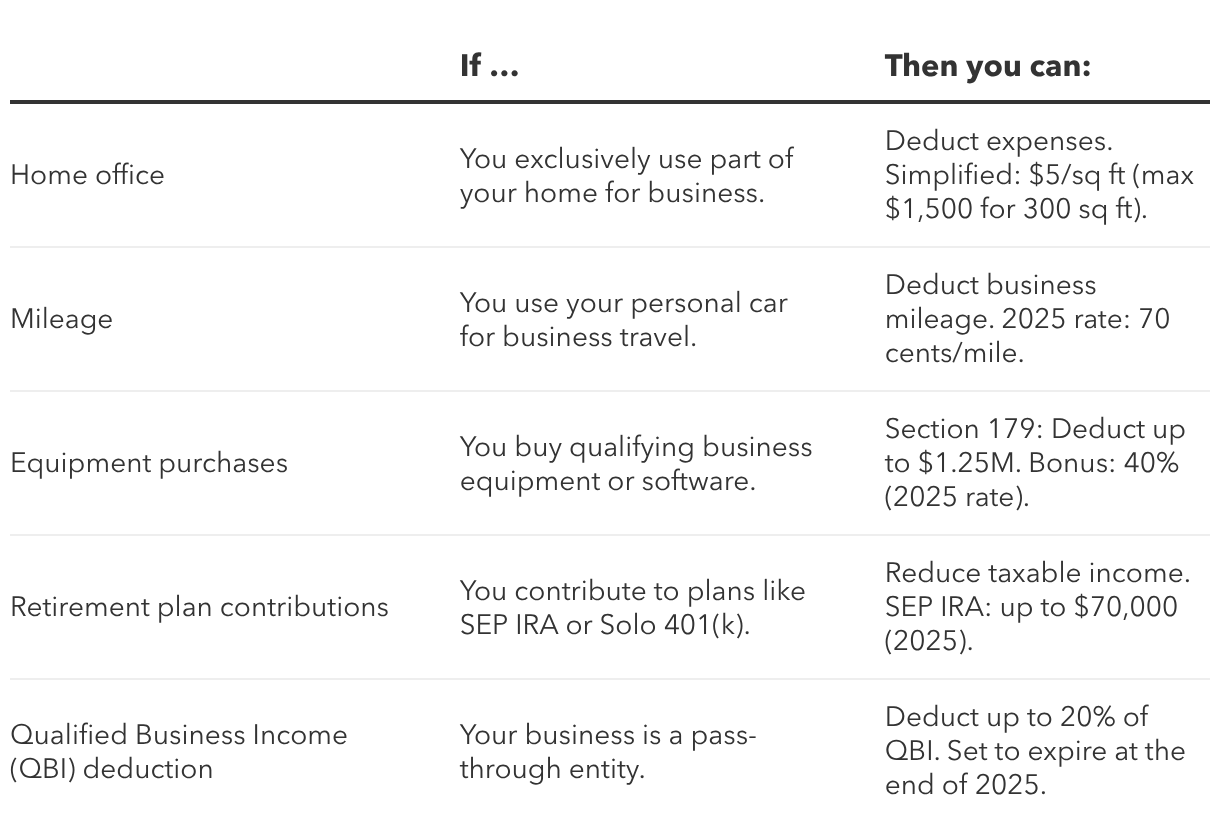

Common deductions: Leverage business expenses (like home office, supplies, business mileage), and the Qualified Business Income (QBI) deduction.

Partnership

A partnership involves two or more owners who share in the profits or losses of a business.

Taxation: Partnerships are pass-through entities. The partnership files an informational return (Form 1065) showing its income but pays no tax. Each partner receives a Schedule K-1 detailing their share. Partners then report this on their personal Form 1040, paying tax at their individual rate.

Common deductions: Claim business expenses and the QBI deduction.

LLC (single-member and multi-member)

The flexibility of an LLC allows it to choose various tax treatments.

By default, a single-member LLC operates as a sole proprietorship for tax purposes.

Taxation: You report income and expenses on your personal taxes using Form 1040 (with Schedule C) and Schedule SE.

Common deductions: Access the same deductions as a sole proprietorship.

On the other hand, a multi-member LLC functions as a partnership for tax purposes.

Taxation: The LLC files an informational return, and each member reports their share of income on their personal taxes.

The LLC files Form 1065, you receive a Schedule K-1, and then use your individual Form 1040.

Common deductions: Utilize the same deductions as a partnership.

LLC Electing to be taxed as an S-corp or C-corp:

An LLC can choose to be taxed as an S corporation or a C corporation by filing specific forms with the IRS.

Taxation: As an S corporation, income passes through to owners. As a C corporation, the LLC itself pays taxes.

Forms vary based on your election (Form 1120-S or Form 1120).

Common deductions: Deductions align with the chosen S-corp or C-corp structure.

S corporation

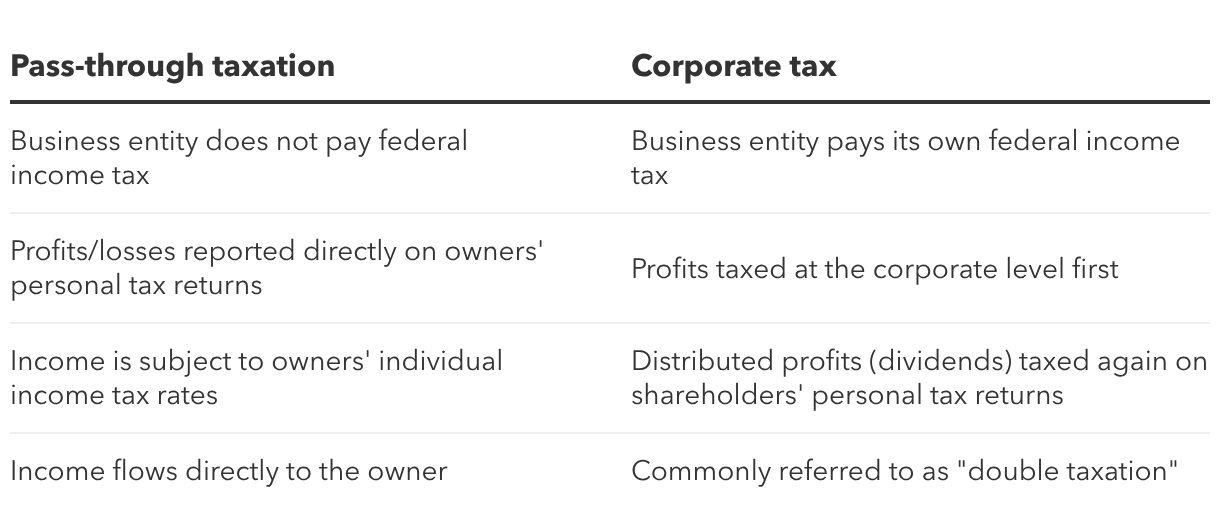

An S corporation offers a special tax election, allowing a corporation to pass its income through to its shareholders for federal tax purposes. This structure helps avoid the "double taxation" of C corporations.

Taxation: An S corporation files Form 1120-S, providing an informational return. Like partnerships, shareholders receive a Schedule K-1 that reports their share of the S corporation's income or losses. Shareholders then report this on their personal Form 1040 and pay tax at their individual income tax rate.

Common deductions: Take business expenses, the QBI deduction, and potentially realize self-employment tax savings on distributions.