You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

Accurate bookkeeping is the key to getting a clear picture of your business's health. A cleanup doesn't just tame the clutter; it empowers you to understand your cash flow, identify areas for growth, and ultimately, take control of your financial future.

Our 12-step guide and downloadable checklist transform the bookkeeping cleanup process from a daunting task into a manageable system for solopreneurs and small business owners alike.

As important as it is to perform a thorough 12-step audit of your bookkeeping, it’s just as important to recognize when to start. Keeping your books tidy ahead of important milestones and identifying small anomalies before they become systemic problems is key to keeping your finances transparent, accurate, and compliant.

Bookkeeping doesn’t look the same as it did five years ago, and neither do the warning signs that should make you consider a proper account cleanup. While many small business owners may try to tidy their books when anomalies surface, it’s just as critical to keep everything accurate and organized ahead of key events.

Here are the top triggers and 2026 that indicate it’s time to start an internal bookkeeping audit:

The first part of bookkeeping basics is assembling all your financial records. This can include:

Don't worry—you don’t have to spend hours sifting through mountains of paper. Digital tools can make this process a breeze. For example, for physical receipts and invoices, consider using a mobile scanning app.

These apps allow you to quickly capture clear digital copies of your documents using your smartphone's camera. The scanned documents can then be easily stored and organized within the app or exported to a cloud storage service for safekeeping.

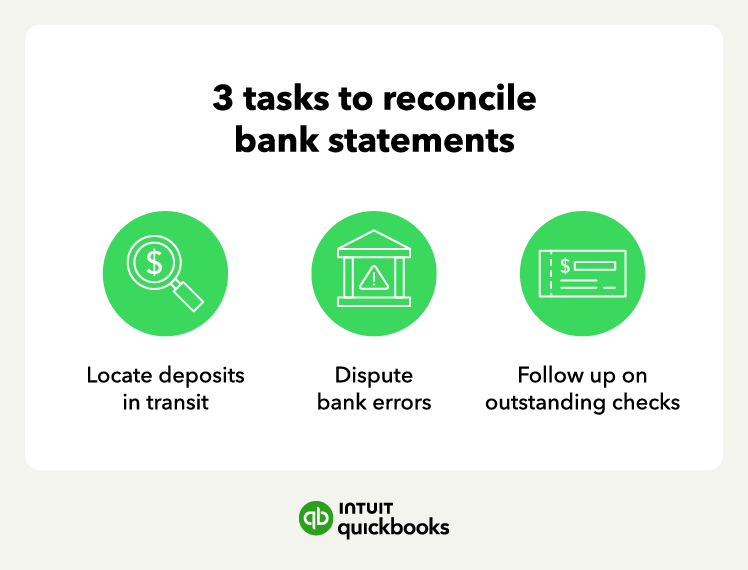

Now that you have all your financial records in one place, it's time to ensure your bank's records match your own bookkeeping. This process, known as bank reconciliation, involves comparing your bank statement balance to the balance in your accounting records and identifying any discrepancies.

Thorough reconciliation reviews three main categories:

Common culprits for these mismatches include:

By carefully addressing these discrepancies, you can ensure your bank records and your accounting software match, providing you with an accurate picture of your financial situation.

This seemingly simple step is crucial for gaining valuable financial insights from your data. By accurately categorizing each transaction, you can track your spending habits, identify areas for potential overhead savings, and monitor the health of your income streams.

Common categories include:

Sort uncollected revenue:

While these are just a few examples, you can customize your categories to best suit your specific needs. The key is consistency and ensuring your categorization system provides a clear picture of your financial activity.

It's time to ensure you haven't missed any outstanding invoices or bills. This step involves reviewing any vendor invoices you haven't yet paid, as well as identifying any invoices you've issued to clients but haven’t collected.

Let's explore how to handle each scenario:

By taking account of these outstanding items, you'll gain a more accurate picture of your current financial obligations and potential sources of future income.

Schedule time for routine bank reconciliations. Regular reconciliation prevents errors from snowballing and ensures your financial records are accurate and reliable.

After you've identified outstanding invoices and bills, it's time to tackle them head-on. Understanding the terms accounts payable and accounts receivable is crucial for effective cash flow management.

Here is the difference between both:

By proactively managing both accounts payable and receivable, you can ensure timely payments to vendors and maximize the amount of cash readily available for your business operations.

The next step involves reviewing and potentially updating your fixed assets, which include:

Over time, these assets lose value due to wear and tear, obsolescence, or other factors. This gradual decrease in value is known as depreciation—a crucial bookkeeping concept that allows you to spread the cost of a fixed asset over its useful life. For 2026, deduction limits rose to $2.56 million under Section 179 of the IRS tax code.

Just like with bank reconciliation, ensure your credit card statements align with your small business bookkeeping records. The process is similar, involving matching transactions on your credit card statement to corresponding entries in your accounting system.

However, with credit cards, there's an added layer of complexity—the potential for personal and business expenses to get mixed up. Carefully review each transaction to ensure only business-related charges are reflected in your bookkeeping. If you find any personal expenses on the company credit card, remove them from your business records.

Don't just rely on the transaction description on the statement. Match each credit card charge to a corresponding receipt to ensure accuracy.

For businesses with employees, accurate payroll records are essential. This step involves reviewing and potentially categorizing your payroll costs within your bookkeeping system.

This data typically includes:

Accurate payroll records are crucial not just for ensuring your employees are paid correctly but also for tax compliance purposes.

This step is particularly relevant for businesses that manage physical products. Here, you'll review and potentially categorize your inventory records within your bookkeeping system. This might involve:

Maintaining accurate inventory records is essential for several reasons. It allows you to:

By meticulously reviewing and categorizing your inventory data, you can ensure your bookkeeping system reflects the true value of your on-hand inventory, which ultimately impacts your tax calculations.

Achieving a clean bookkeeping system goes hand-in-hand with ensuring your business is tax-compliant. Solopreneurs and independent contractors will use Schedule C (Form 1040) to declare profit and loss. Businesses that contract with you will issue 1099-NEC or 1099-MISC to report nonemployee compensations, which are added to the Schedule C.

Be mindful of sales tax nexus, which may link you and your business to one or more states based on your physical presence or economic activity.

Here are some other key areas to focus on:

Unassigned transactions can create a murky financial picture and hinder tax preparation. Review and categorize all income and expenses into appropriate categories. Avoid generic labels like "other" or "miscellaneous," as these offer little clarity to tax professionals.

Double-check your chart of accounts to ensure items like credit card payments are classified correctly. A credit card payment itself isn't an expense; it reflects settling a previous expense you categorized earlier. Finally, provide clear descriptions for fixed assets beyond simply listing them in the fixed asset accounts. Your tax preparer will need this information for accurate tax calculations.

Negative numbers can arise from errors in recording transactions. For instance, a negative number in your accounts receivable report might indicate a payment received without a corresponding invoice. Address these discrepancies promptly to ensure accurate financial reporting and a smoother tax filing process.

If your balance sheet doesn't balance, investigate potential issues like incorrect account closures, misplaced inventory entries, or the need for file verification and repair. Additionally, the prior year's balance sheet should align with the one reported on your tax return.

This signifies no unadjusted entries were made in prior years, simplifying tax filing. Finally, verify that loan balances on your balance sheet match year-end loan statements, with separate accounts for interest, late fees, and principal.

Imagine cloud service interruptions or data sync errors corrupting your bookkeeping software, a hardware malfunction erasing your files, or even a cyberattack compromising your system. After all your hard work cleaning up your books, the last thing you want is to lose that valuable data.

Regular backups are essential for safeguarding your financial information and ensuring disaster recovery in case of unforeseen events. Cloud backups of your digital bookkeeping systems create copies of your data, allowing you to restore your bookkeeping system to a previous state if disaster strikes. Ensure that both your on-site record and cloud backups are guarded by multifactor authentication (MFA) to prevent unauthorized access and ransomware. MFA uses passwords, SMS codes, authenticator apps, and more to safeguard your data even if one channel is compromised.

Just like a clean house needs regular maintenance to stay tidy, your bookkeeping system requires ongoing attention to maintain its clarity and accuracy. Scheduling regular bookkeeping sessions helps you avoid the chaos you just tackled.

By dedicating designated time slots for bookkeeping tasks, you can consistently categorize transactions, reconcile accounts, and monitor your financial health. This regular upkeep prevents small issues from snowballing into a future clean-up project. Think of it as an investment in your financial well-being, ensuring you have easy access to accurate and up-to-date financial information whenever you need it.

If you find the thought of regular bookkeeping sessions tedious or simply don't have the time to dedicate to it, then consider hiring a professional bookkeeper. A qualified bookkeeper can remove this burden, ensuring your finances are meticulously maintained. They can also offer valuable insights and guidance to help you make informed financial decisions for your business.

Bookkeeping anomalies will always happen. With AI-powered detection and proper human oversight, these one-off errors will be resolved quickly. Needing to perform a thorough bookkeeping audit doesn’t stem from anomalies. It stems from a full system failure.

Small business owners should be proactive in optimizing their tech stacks to ensure that each automated system and workflow operates correctly.

Here are a few of the top things SMB owners can do to ensure their systems save time, not create problems:

Accounting software like QuickBooks Online is designed to let small business owners and solopreneurs customize how their system records new data. Implementing the following rules reduces the need for an emergency system cleanup:

These rules and practices tailor your accounting software to your specific business operations and can help prevent systemic failures.

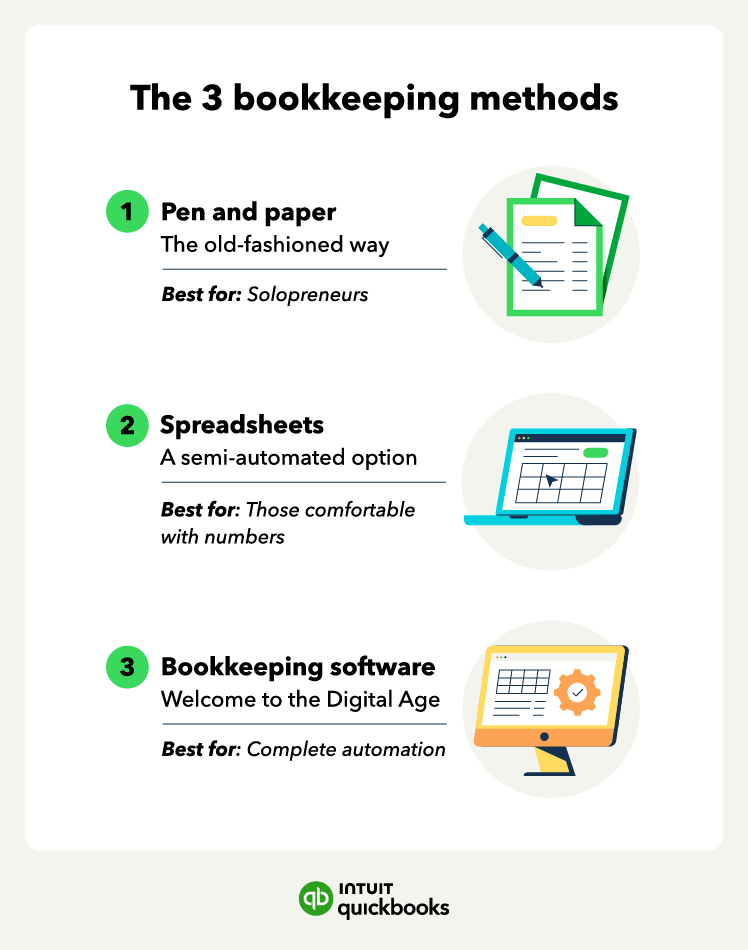

The best bookkeeping method depends on the size of your business and your comfort level with automated technology. Regardless of your preferred method, there are many bookkeeping tips to keep your books clean and efficient in the long run.

Pros: Simple and low-cost.

Cons: Time-consuming, error-prone, and difficult to analyze data.

The DIY, manual approach to bookkeeping is ideal for very small businesses with minimal transactions. A few ways to best utilize this method include:

This method is outdated, risky, and can lead to significant compliance issues if you make an error.

Pros: More affordable than bookkeeping software, allows for customization.

Cons: Requires some technical knowledge, formulas can be complex, and data sharing can be cumbersome.

Spreadsheets offer more flexibility and organization than pen and paper. Here’s how:

For a slightly larger learning curve than pen and paper, you can significantly increase your bookkeeping capabilities with spreadsheets. If you prefer tech but can’t decide between spreadsheets and bookkeeping software, the lower cost of spreadsheets may give them an edge.

Pros: Streamlines data entry, automates tasks, facilitates reporting and analysis, and secures cloud storage.

Cons: Typically requires a monthly subscription fee and can have a learning curve.

Bookkeeping software offers the most robust features and automation, which is ideal for businesses with significant transaction volume or complex financial needs. Here are some tips:

Accounting software can cater to your bookkeeping needs and offers the most robust features and automation available. This is a great option for busy business owners who want to streamline their bookkeeping.

Here are some telltale signs that your bookkeeping system might need a clean-up:

By addressing these warning signs and taking steps to clean up your books, you'll gain control of your finances, make smarter business decisions, and experience a smoother tax season.

By taking these warning signs seriously and initiating a bookkeeping cleanup, you'll know exactly where your business stands financially, have the confidence to make informed decisions, and enjoy a stress-free tax season.

Many bookkeeping services can offer expert assistance to get your finances in order and keep them that way. Consider investing in solopreneur accounting software to level up.

Call Sales: 1-800-285-4854