Understanding Payment Holds

Getting paid is important to everyone, especially small business owners. So when something goes wrong, it is important to understand why, how to manage the issue and how to minimize these in the future. In this article, we will guide you through the what the typical payments process cycle looks like and some specific scenarios where holds occur. If you are currently experiencing payment holds, additional guidance is provided in our next article, “Managing and Avoiding Payment Holds”.

In order to have the best possible experience, we encourage you to read through this entire article to gain a thorough understanding of payment holds. If you are short on time and need some quick guidance, you can also click on the individual links below to jump to the areas that interest you the most.

Contents

- When to Expect Funds in Your Account

- Good to Know - Credit Card Processing Cycle

- What Triggers a Hold?

- What Happens When Funds Are Placed On Hold?

- What Happens When You (the Business Owner) Void a Credit Card Transaction

- What Happens When Your Customer Voids a Credit Card Transaction

When to Expect Funds in Your Account

When you are using an electronic payments system, it is important to have the right expectations of when funds will hit your bank account. The time it takes to process payments can vary based on a number of factors, such as the time of day. For QuickBooks Online Payments users, credit card payments typically deposit in about 2-3 business days and free ACH Bank Transfer payments deposit in about 2-7 business days.

|

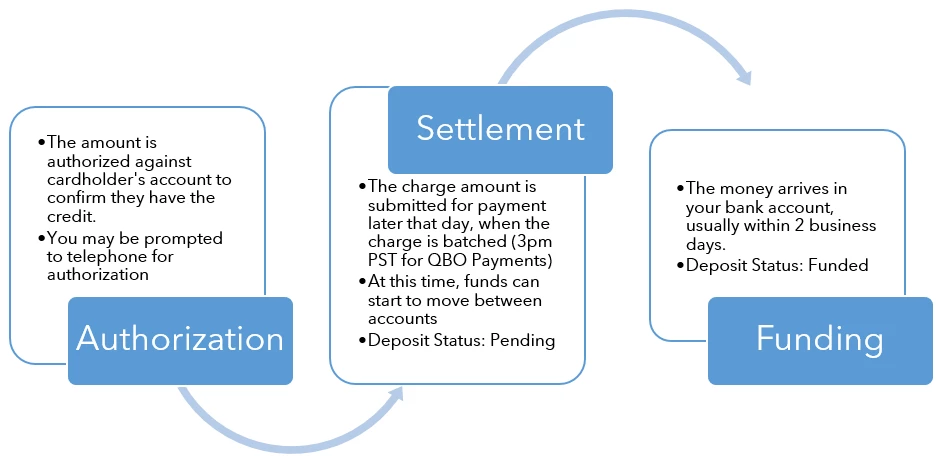

Good to Know - Credit Card Processing Cycle

|

What Triggers a Hold?

When something unexpected occurs in your transaction(s), a hold may be placed on the funds. Here are some common reasons for holds:

- When your payment processing exceeds the established maximum dollar amount expected on your account

- When a transaction is processed after several authorization attempts and failures

- When certain transactions require verification of your business type to ensure it is compliant with the Intuit Acceptable Use Policy

- When our systems identify processing patterns that pose a risk to any of the parties involved: You, your customer or to Intuit.

What Happens When Funds Are Placed On Hold?

Intuit will attempt to contact you via the phone number you have provided on your merchant account. You will then receive an email with detailed instructions on what additional information is needed in order to complete our review. For example, we may ask for a detailed invoice with the cardholder's name and billing address as they are reflected on file with their bank. To resolve the issue as quickly as possible, please submit any requested documents as soon as possible.

When will Intuit release these funds?

We are unable to deposit any money from funds on hold until we complete our review. Once all of the requested information has been provided, the review is typically completed within 2 business days.

What Happens When You (the Business Owner) Void a Credit Card Transaction?

If you void a transaction prior to batching, the authorization for that amount remains, placing a hold on the customer’s credit card for around 7-10 days (or up to 30 days, depending on the policies of the cardholder’s issuing bank).

What Happens When Your Customer Voids a Credit Card Transaction?

A chargeback is a transaction that has been disputed by the cardholder or card issuer. Here are the most common reasons for chargebacks. Listed below each bullet is a list of documents to dispute the chargeback.

- The cardholder claims they did not get the merchandise or service.

- Rebuttal addressing the Cardholder's claims.

- Proof of Delivery.

- Signed proof of pick-up.

- The cardholder claims the merchandise or services were not as initially described or were received in defective condition.

- Rebuttal addressing the Cardholder's claims.

- Proof that merchandise/service matched the description.

- Proof that the Cardholder did not attempt to return the merchandise.

- Proof of ongoing negotiations between the Cardholder and the Merchant.

- Outside opinion from a third party expert in support of the Merchant's rebuttal.

- The cardholder claims the transaction was cancelled and/or the merchandise was returned.

- Rebuttal addressing the Cardholder's claims.

- Proof that the Merchant's return/cancellation policy was properly disclosed to the Cardholder at the time of sale.

- Proof that the Cardholder's cancellation/return was not in accordance with the Merchant's properly disclosed policy.

- The cardholder does not recognize the transaction.

- A copy of the Transaction Record with showing what was purchased.

- The cardholder claims fraud or unauthorized charge.

- A copy of the signed and swiped receipt (if applicable).

- Rebuttal letter, Invoice, proof of delivery.

- Compelling evidence (i.e. photographs, emails, etc.), to support that the Cardholder made the Transaction and has received the merchandise/service.

- Duplicate transactions.

- Failure to respond to an inquiry (American Express only).

|

Please note: Even if you work with Intuit to successfully reverse a chargeback, you still need to pay a chargeback fee. The chargeback fee is not a penalty fee but a processing fee for handling the issue on your behalf.

|

If you have need help with payment holds, please continue reading more in our next article “Managing and Avoiding Payment Holds.