Common self-employed deductions

Working for yourself comes with a big perk: you can write off many of the costs of running your business. Here are some of the most common deductions available to self-employed individuals.

Start-up costs

Starting a business isn’t cheap, and the IRS knows it. That’s why they let you deduct some of your start-up expenses.

In your first year, you can usually deduct up to $5,000 of start-up costs (e.g., market research, advertising, or professional fees to set up your business). You can also deduct up to $5,000 of organizational costs (e.g., forming an LLC, filing fees, or drafting partnership agreements).

If your total start-up or organizational costs are more than $50,000, that first-year deduction gets reduced. Anything above the limit usually has to be spread out (amortized) over 15 years.

Business loan interest

If you take out a small business loan to help run your operation (e.g., buy equipment or hire help), you can usually deduct the interest you pay. For most small businesses, this deduction is straightforward and can really add up, especially if you rely on financing in your early years.

Make sure to keep this key information in mind when considering this deduction:

- Only the interest is deductible, not the loan principal.

- The loan has to be for a business purpose and properly documented, not a casual loan from a friend with no paperwork.

- If you use part of the loan for personal spending, you can only deduct the portion used for the business.

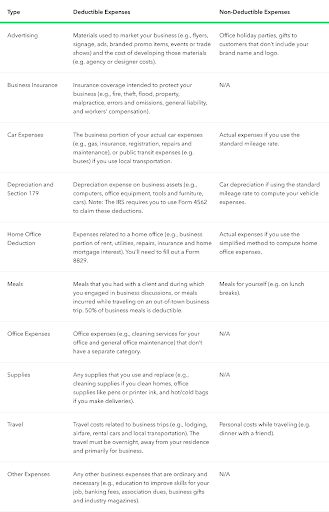

Travel and hotel

If you travel to visit clients or attend trade shows, you may be able to deduct the cost of travel. Business travel expenses include transportation and accommodation costs. The key is that the trip has to be legitimately for business. The IRS calls these “ordinary and necessary” expenses.

Here are a few things to keep in mind:

- The trip has to take you away from your tax home (your main work location) and usually requires an overnight stay.

- Everything must be reasonable, not luxurious. If you stay in a five-star suite when a normal business hotel would do, the IRS might question the excess.

- Keep records, like receipts, hotel bills, or a calendar note about the business purpose of the trip.

Meals

Meals can also be deductible, but only under certain conditions. In most cases, you can deduct 50% of the cost of a meal if it’s connected to your business. That includes meals while you’re traveling for work or when you’re meeting with a client, partner, or prospect.

To qualify, you (or an employee) must be present at the meal, and the purpose has to be business-related. For example, discussing a project over lunch with a client would count. Grabbing dinner with a friend and casually chatting about work wouldn’t.

And just like with business travel expenses, the meal must be “ordinary and necessary.” For example, a modest dinner at a local restaurant is fine, but a lavish multi-course feast with wine pairings (unless clearly tied to your work) may not pass.

Home office

Many freelancers work out of their homes, and the IRS allows self-employed persons to deduct the portion of their mortgage (including property taxes) or their rent that goes toward a home office.

To qualify for the home office deduction, you must have a specific area in your home designated for working, and you must refrain from using it for other purposes.

You can claim it in two ways:

- Simplified method: You multiply the square footage of your office (up to 300 sq. ft.) by $5. That means the most you can deduct is $1,500. No receipts or complicated math required.

- Regular method: Deduct a percentage of actual costs like rent or mortgage interest, utilities, insurance, and repairs, based on how much of your home is used for business. For example, if your office takes up 10% of your home, you can deduct 10% of those costs.

Overall, it’s one of the best ways to cut down your taxable income when you’re self-employed. The simplified method can save you up to $1,500, while the regular method can be worth much more if your housing costs are high.

Utilities

Self-employed individuals who work at home can deduct a portion of utility costs as a home office expense. The percentage of your utility costs that are tax-deductible is proportional to the percentage of your home occupied by your office. For example, For example, if your home office takes up 200 square feet in a 2,000-square-foot home, that’s 10% of your total space. You could generally deduct 10% of your electricity, gas, water, and other household utility bills.

Along with gas and electricity, you can deduct the costs of heating, air conditioning and phone service. Be aware, however, that you cannot deduct the actual cost of utilities if you claim the simplified home office deduction. If you want to claim actual utility expenses, you’ll need to use the regular method and keep detailed records.

Professional development

As a freelancer, it’s important that you find ways to stand out from your competitors. To keep ahead of the pack, many freelancers attend classes and educational seminars.

The cost of these expenses can add up, so the IRS allows freelancers to deduct expenses related to professional development on their tax returns, including tuition, books, supplies, workshop or lab fees, and registration fees for conferences, and dues for professional organizations and membership fees.

To qualify for this deduction, the education must directly support the work you already do. That means the class or training needs to either help you sharpen your current skills or be required to keep your license or certification active. What you can’t deduct are classes that prepare you for a completely different career. For example, a graphic designer can’t deduct the cost of going to nursing school.

Advertising and marketing

Self-employed people have to engage in marketing and advertising if they hope to stay competitive. The IRS permits you to deduct the cost of flyers, web advertisements, business cards, and print ads, along with other marketing expenses.

And as with many of these business expenses, these costs must be ordinary and necessary to your business, meaning they’re common in your industry and genuinely help you attract or keep customers. Personal promotions or expenses unrelated to your work don’t count.

Website

With a majority of consumers using the internet to research purchases, creating a mobile-friendly, responsive website is crucial for a freelancer’s success.

Self-employed persons can deduct costs related to their business websites, including domain fees, web design, web building, and maintenance.

You can also deduct expenses of ongoing subscription services (such as e-commerce platforms, e-commerce accounting software, or website builders), and software tools used to manage or update your site. If you pay contractors, designers, or developers to build or maintain your website, those payments qualify as deductible business expenses, too.

Most of the time, you can deduct these costs in the year you pay them, just like any other business expense. But if you do a major build or redesign that’s expected to last several years, the IRS may treat it more like an asset you have to depreciate over time. In that case, you might still be able to deduct it all at once using Section 179 (if you qualify).

Software

From sophisticated video editing programs to more basic options like Microsoft Office and Adobe Acrobat, software can be expensive. Software costs are a common tax deduction for small business owners and freelancers.

For most programs that cost under about $2,500, you can deduct the full price in the year you buy it. If it’s more expensive or meant to last several years, you may need to spread out the deduction over time, or use Section 179 to write it off faster.

Also, if you use a piece of software partly for personal use and partly for business, you can only deduct the business-use portion, so keep good records of how much time or usage goes to each.

Mileage and gas

Do you regularly drive to meet clients or suppliers? If so, you should take advantage of the tax deductions available for vehicle mileage or normal vehicle wear and tear.

You can choose between two types of vehicle-related deductions: the standard mileage option or the actual expense option.

- Standard mileage rate: Standard mileage rate: For 2025, you can deduct 70 cents per mile driven for business. This method is simple because you just can use a mileage log or mileage tracker app and multiply by the IRS rate. For example, if you drive 5,000 miles for business, you could deduct $3,500 (5,000 x $0.70).

- Actual expense method: Instead of using the flat rate, you can deduct a percentage of your actual vehicle costs (like gas, oil, repairs, insurance, lease payments, and depreciation) that match your business-use percentage. For instance, if your car expenses for the year total $8,000 and you use your car 60% of the time for business, you could deduct $4,800 (60% x $8,000).

So, which one should you choose? It depends on how much you drive and how expensive your car is to maintain. The mileage rate is usually easier and works well if you drive a lot of miles but keep your car costs low. The actual expense method might save you more if you have high costs for things like gas, insurance, or repairs.

Either way, make sure you keep solid records (e.g., mileage logs, receipts, and notes about each trip) so you’re covered if the IRS ever asks.

Incorporation

If your freelance business is successful, you may consider starting a corporation in the future. The IRS permits new businesses to deduct expenditures associated with incorporation, including state registration fees and legal costs.

You can usually deduct up to $5,000 of those incorporation expenses right away in your first year of business, as long as your total costs don’t go over $50,000. If you spent more, you’ll need to spread the rest of the deduction out over 15 years. Keep solid records of every invoice and receipt so you can make the most of this deduction.

Health insurance

Most full-time employees receive their health insurance through their employer. However, many self-employed professionals must pay for their own healthcare out of pocket, and those monthly premiums can add up to a hefty chunk of change every month.

Self-employed individuals who meet certain criteria may be entitled to a special tax deduction that allows them to deduct the cost of health insurance premiums. The deduction includes coverage for dental expenses, vision, long-term care and short-term care. You can deduct the cost of coverage for yourself, your spouse and any dependent family members.

If you meet the following requirements, you can deduct the cost of your health insurance plan:

- Your business is generating a profit. If your business claims a loss for the tax year, you can’t claim the health insurance deduction.

- You were not eligible to enroll in an employer’s health plan. This also includes your spouse’s plan. If you were eligible to enroll in a health plan and chose not to, you cannot claim the health insurance deduction.

- You are only attempting to deduct premiums paid for the months when you were not eligible for an employer’s health plan.

Note that health insurance costs are not posted with other expenses on Schedule C, Business Profit and Loss.

Instead, self-employed workers who use Schedule C deduct health insurance costs using Form 7206 and report those costs on Schedule 1 of Form 1040.

Self-employment tax deduction

When you work for yourself, you’re responsible for paying both the employer and employee portions of Social Security and Medicare taxes (FICA taxes). This is called the self-employment tax, and it’s 15.3% of your net earnings (12.4% for Social Security up to the annual wage base limit, and 2.9% for Medicare, with an additional 0.9% Medicare tax for higher earners).

However, the IRS lets you deduct part of this tax to reduce your adjusted gross income. You can claim an above-the-line deduction for 50% of your self-employment tax. For example, if you owe $8,000 in self-employment tax, you can deduct $4,000 when figuring out your taxable income.

Just be aware that this deduction doesn’t reduce the amount of self-employment tax you actually owe. It only lowers the income that’s subject to income tax

Qualified business income deduction

The qualified business income (QBI) deduction, also known as the Section 199A deduction, is one of the biggest tax breaks available to freelancers and small business owners. It allows you to deduct up to 20% of the profit from your business before calculating how much income tax you owe.

This deduction only applies to money you make from running your business. It doesn’t cover wages, capital gains, or investment income.

You may be eligible if you’re a sole proprietor, independent contractor, partner, S corporation owner, or certain LLC owner.

For 2025, the full deduction is available if your taxable income is under $191,950 for single filers or $383,900 for joint filers. You’ll calculate the deduction on IRS Form 8995 or 8995-A, depending on your situation. If you qualify, it will show up as a direct reduction to your taxable income on Form 1040.

Retirement plan contributions

The IRS allows self-employed people and small business owners to deduct contributions they make to certain retirement accounts.

If you work for yourself, you have several options:

- SEP IRA (Simplified Employee Pension): This plan is easy to set up and flexible. For 2025, you can contribute up to 25% of your net earnings from self-employment, up to $70,000.

- Solo 401(k): This plan is great if you want higher limits and the ability to make both employer and employee contributions In 2025, you can contribute up to $23,500 as an employee (plus an extra $7,500 if you’re 50 or older), plus up to 25% of your net earnings as the employer, with a combined cap of $69,000 (or $76,500 with the catch-up).

- SIMPLE IRA: This plan is designed for small businesses with employees, but solo workers can use it too. In 2025, you can put in up to $16,500 (plus $3,500 if you’re 50+).

Tip income deduction

The One Big Beautiful Bill Act created a new tax break for workers who earn tips. If you work in a job where tips are a normal part of the pay (think bartenders, hairstylists, drivers, etc.), you may be able to deduct the amount of qualified tips you report, as long as you properly report your tips on a W-2, 1099, or Form 4137.

You can deduct up to $25,000 a year, but not more than your net business income if you’re self-employed. The deduction starts shrinking once your income tops $150,000 (single) or $300,000 (married filing jointly).

Cash tips, card tips, and pooled/shared tips all count as qualified tips, and you can use it whether you take the standard deduction or itemize.