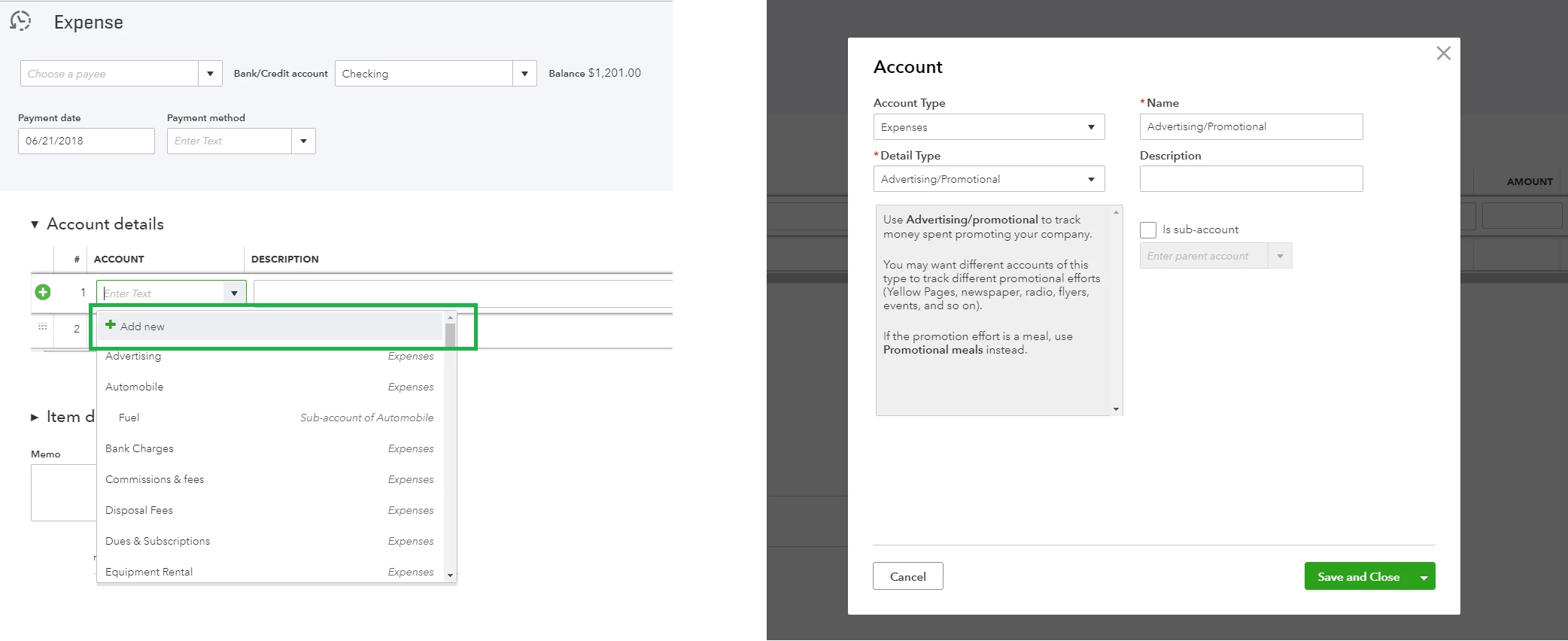

Creating and Managing Accounts

This entry focuses primarily on the Chart of Accounts and associated reporting tools that pull information from those accounts. Most of the time, you create accounts as you work, such as when you first create a new product or service, log an expense or connect a bank account. If you need to modify an existing account or create new ones from scratch, you’d do so from the Chart of Accounts. This is essentially a list of your accounts that determines how transactions are categorized and interpreted (i.e. whether a transaction adds or deducts from an account).

We generally recommend not making too many changes to the Chart of Accounts (referred to as CoA from here on) – it's complicated territory that should be explored once you’re completely confident using QuickBooks. However, we also believe every user should have a basic understanding of what the CoA is, how it organizes your finances and when to go in and make adjustments.

Here are some quick tips:

- If you haven’t done so already, review accounting and bookkeeping basics and the Accounting Terms You Need to Know

- Keep your CoA simple - - that means keeping the number of accounts to a minimum and giving accounts relevant yet understandable names

- Pay extra attention to Account Types as these are what determine transaction categorization

- If you don’t know what type of account to create, ask the community or follow the tutorial creators’ advice and create an “Ask my Accountant” account to house all transactions you’re unsure about

Understanding the Chart of Accounts | QuickBooks Online Tutorial 2018

Notice how a single transaction impacts a number of accounts. When the narrator makes a bank deposit for a single loan, both the checking and liability account increase for the $15,000 amount. By creating and categorizing accounts, QuickBooks automatically manages and runs the calculations.

Why don't you try creating a few transactions in Test Drive (above) and poke around the COA to see the results - - you may be surprised just how many calculations occur during a single transaction.

How to Set Up Your Chart of Accounts: Understanding the Basics | QuickBooks Online Tutorial 2018

This video is very important, so you may want to watch it a few times. We recommend creating new accounts sparingly. QuickBooks Online already provides you with most standard accounts and creates new ones when you do activities like connecting a bank account. Less is more - - meaning more time and less to manage.

If there’s one key take away from this video, think broadly about your account organization and structure them in ways that make sense to you and your accountant. A second and equally important point is the available types in the CoA:

- Category type – determines if the accounts on the Balance Sheet or Profit and Loss Sheet. This is the more important of the two because the category type determines how transactions hit your books.

- Type detail – doesn’t determine how an account is used, it’s there for detail and tracking purposes. Think of it like a secondary description that will help you quickly distil lines on a report.

- If you need a refresher on reports and how these types impact them, click here.

Our trainer makes key distinctions between accounts that show up on your Balance Sheet vs. the Profit & Loss Report. You’re probably familiar with the Profit and Loss Report, which looks at all of your Income and Expense accounts, but you may not recognize some of the heavier accounting terms tied to the Balance Sheet. Essentially, the Balance Sheet shows your asset (what you own), liability (what you owe) and equity accounts (income and expenses).

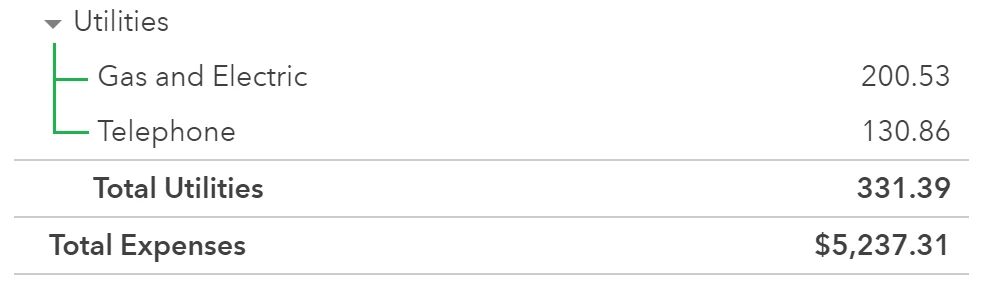

Sub-accounts are a critical organizational feature for the CoA. Instead of having separate expense accounts for various utilities, you can create a “Utilities” parent account and separate “gas and electric” and “telephone” sub-accounts. You can go four levels deep with sub-accounts so you can break this down even further by different cell carriers if you wanted to.

| Important - Going forward, remember to add transactions to the appropriate sub-accounts and not the parent account (in the case above, in either “gas and electric” or “telephone,” not “utilities”) which becomes the aggregate for the child accounts. |

Opening balances, as the video explains, are typically added when you have an existing account outside of QuickBooks that you’re recording for going forward with funds already in it, such as a bank checking account or an asset account.

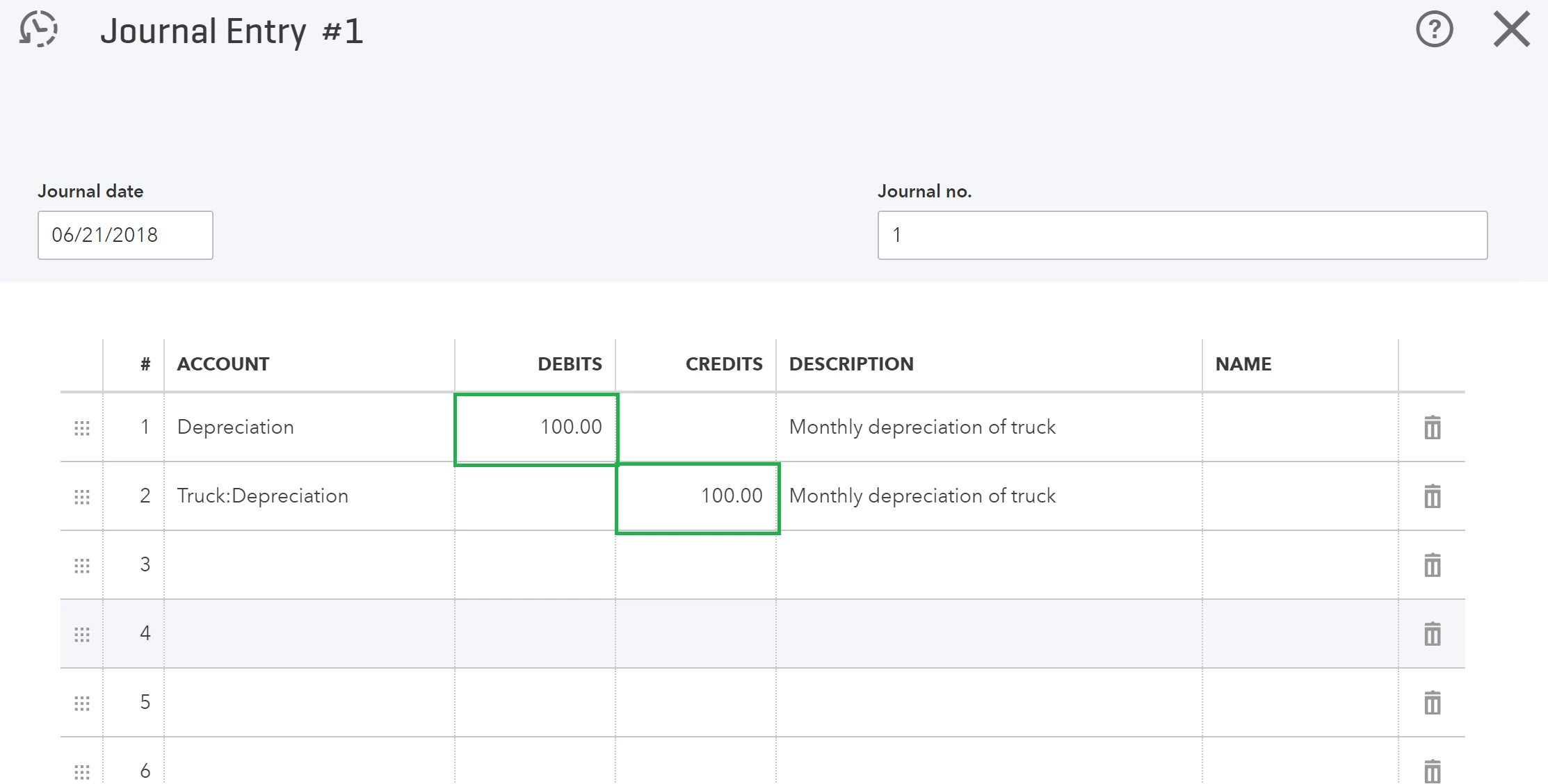

How to Use Journal Entries | QuickBooks Online 2018

When transactions involve customers or vendors, use the standard transaction process. Journal Entries are generally used for making adjustments or obscure entries that aren’t part of your normal workflow. You would typically use Journal Entries for entering things like Depreciation.

Immediately, you’ll notice the terms “debits” and “credits” used, which we went over briefly in the QuickBooks Encyclopedia. The Journal Entry process (often referred to as JE) draws from one account and adds to another in order to keep everything balanced, a process that may not be familiar to non-accountants.

These types of entries are complicated. If you’re at this level of complexity in your accounting, make sure you connect with your accountant for best practices.

Check your Progress

What’s Next?

- How to Use the Undeposited Funds Account to Receive Payments in QuickBooks Online

- Setting up for Success in QuickBooks Online - Adding Products and Services, Customers, and Vendors t...

- How to Adjust your Invoice Payment Terms in QuickBooks Online